Happy Fool’s day!!

Except for all of us who pay attention to our money! (HEYO!)

Saw these stats come out from Experian, and while it looks like an epic prank it’s anything but:

- As of the the last quarter of 2018, consumer debt now totals a whopping $13.3 trillion

- With credit card debt coming in at $834 billion

- Mortgage debt totaling $9.4 trillion

- Personal loan debt at $291 billion

- Auto loan balances at $1.27 trillion

- And student loan debt at a new record high of $1.37 trillion

But hey! At least our lifestyles must be great!! (Oh wait, they’re not??? Then what the hell are we doing??!)

Ugh…

But in positive news, at least those of us HERE are on track, right?? :) Even if you’re slowly working through some of life’s past mistakes?! Better to make them all now than later, baby! Life doesn’t have to be so complicated!

As a wise P. Diddy once pontificated:

“Anything that costs you your peace of mind is too expensive…”

(And people say rappers aren’t fiscally aware – HAH)

At any rate, here’s this month’s net worth report along with the rhymes and reasons behind it… Although much less rhyming than reasoning I’m afraid… (I like big budgets and I cannot lie! You other debtors out there can’t deny! Woop!)

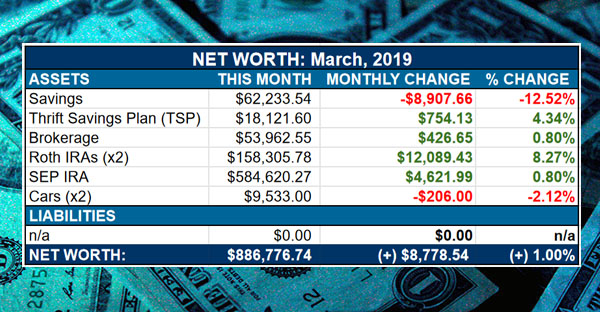

Net Worth Report: March, 2019: $886,776.74

[As part of our Net Worth Series where we share real life snapshots of our money (my money!) to better open up conversations around this stuff… Some months we’re up and others we’re down (way down), but it all gets displayed here as it happens in real life! Here’s report #134!]

CASH SAVINGS: $62,233.54 (-$8,907.66): A hefty drop, but a hefty addition to our Roth IRAs too! As we finally decided to max them both out (me + mrs) and keep our yearly record going… Even though it did make me a little nervous knowing a house purchase may be looming around the corner… But hey – gotta keep my finances on its toes, right?! ;)

THRIFT SAVINGS PLAN (TSP): $18,121.60 (+$754.13): Another nice jump as my wife continues to divert money into it every paycheck! One of the nice perks of having a 9-5: matching retirement contributions!! Something that goes out the window when you’re self-employed!

BROKERAGE: $53,962.55 (+$426.65): Nothing too fancy going on here, but this account *is* why I’m more comfortable dumping out cash reserves to fund our IRAs… knowing we have a nice pot we can liquidate at any point once/if needed. Like for that 20% down payment coming up!

ROTH IRAs: $158,305.78 (+$12,089.43): Now we’re talking!! If the market’s not going to amp it up for us this month, we will! ;) And pretty much the only time where you can even see your contributions making an impact with how wild the swings are these days, jeesh…

SEP IRA: $584,620.27 (+$4,621.99): Similar to the brokerage account, nothing new going on or added here lately… Just the markets doing its thing and taking the accounts along with them!

Here’s how our investments have fared over the past handful of years through Vanguard:

CAR VALUES: $9,533.00 (-$206.00) — And lastly, the cars! Which we conservatively value *down* every month using KBB.com’s tools… Here’s the values of them, both very much paid off:

- 2008 Lexus RX350: $6,974.00

- 2005 Toyota Corolla: $2,559.00

And that’s March!

Total change in net worth this month: (+) $8,778.54

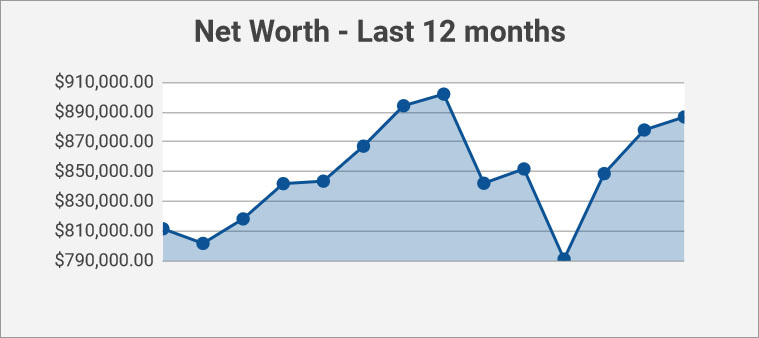

Total changes over the rolling 12 months:

It’s nice to be inching closer to last September’s highs again :) Though we’ll see what the future brings!

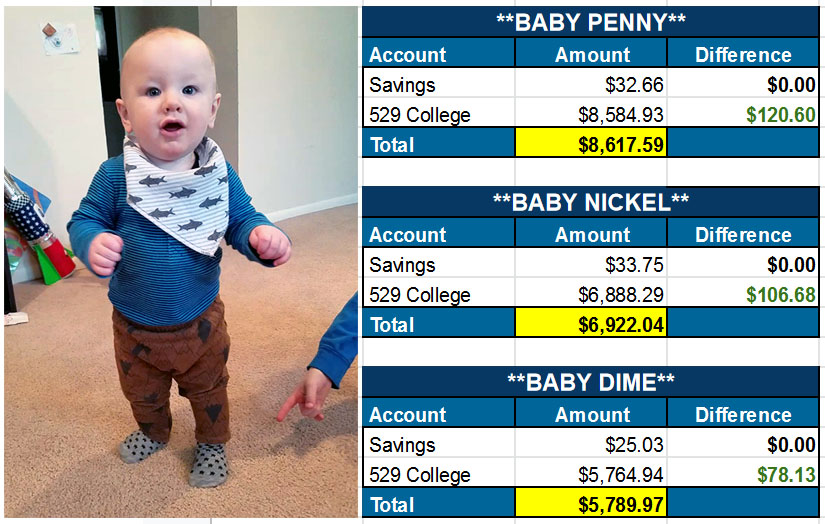

And lastly, a snapshot of my kids’ net worths…

Featuring Baby Dime who’s proudly showing off his standing skills now at only 10 months (!!).

(I swear – he cannot WAIT to be like his brothers! He just wants to play and wrestle all day like a “big boy,” and gets so frustrated when his body doesn’t work the way he wants it to, haha… Not unlike daddy after a few too many beers!)

Alright – so that’s what my money is doing this month… How about yours?? Anything exciting going down??? Anyone cross any major milestones?

Divulge it all below and let’s discuss!! If you can’t talk about money here, where can you??! :)

Peace, love, and spreadsheets,

![]()

PS: If you’re just getting started in your journey, here are a few good resources to help track your money. Doesn’t matter which route you go, just that it ends up sticking!

- The "Budget/Net Worth" spreadsheet - the colorful Excel template I personally use.

- The "Money Snapshot" spreadsheet - a simple Excel template I created for my former $$$ clients

If you're not a spreadsheet guy like me and prefer something more automated (which is fine, whatever gets you to take action!), you can try your hand with a free Empower account instead (formerly Personal Capital)

Empower is a cool tool that connects with your bank & investment accounts to give you an automated way to track your net worth. You'll get a crystal clear picture of how your spending and investments affect your financial goals (early retirement?), and it's super easy to use.

It only takes a couple minutes to set up and you can grab your free account here. They also do a lot of other cool stuff as well which my early retired friend Justin covers in our full review of Empower - check it out here: Why I Use Empower Almost Every Single Day.

Get blog posts automatically emailed to you!

J,

Is your wife making out TSP? If not, why not? Just curious.

She’s putting in enough to get the company matches right now, but not maxing it out every year. Mainly just because we’re enjoying the cash flow right now (allows me to be more lax on my own income streams), but honestly we haven’t really talked or thought it over that much… Which we probably should, haha…

I spent $535.00 on haircuts in 2018. I’m just a normal dude with less than average hair. I’ve seen many videos (including MMM’s) on cutting your own hair but I’m so AFRAID of jacking it up. Any tips or success/disaster stories out there anyone? How bout you J-Dawg?

Haha… I’ve been cutting my own hair for years now!

Although there’s nothing much to shaving the sides and leaving the middle :) I do have to have steady hands while also using a mirror at the same time to make sure it goes okay, haha…

For the first few years I had my wife cut my hair which could be another option for you, but then I felt bad bugging her every two weeks until I decided to try it myself.

Figuring out how to cut your own hair not only saves you money, but also time! And much more convenient! :)

Life hack – have your significant other (with no hairdressing experience) cut your hair to save the cash. I figure there is no one more invested in making sure you look good than a partner. Plus the bald spots grow back quicker than you’d think!

Thanks for the tip Steven. Bald spot..YIKES…haha!

Haha! I forgot about the Mohawk. I read so much I don’t t even look at the pictures of you.

I simply shave my head using the smallest guide so I’m not doing anything fancy, but you definitely need a couple mirrors to see all angles and need to make sure you cut at different angles to catch the hair no matter which way it’s growing (and keep me from having lines in my hair). Having someone else like a wife help out is nice as well since they can see things a bit easier. Over time, it gets easier and easier.

Thanks Scott. I just gotta make that initial plunge and go for it or my wife take a crack at it.

Like Scott below, I’ve shaved my head for more than 20 years, or just let it grow out to donate, then shave again.

I find the Remington HC4250 to be a fabulous tool. No stupid cord, and super easy for touch ups.

$535.00/year x 20 years $10,700.00 BEFORE compounding $$ :-)

You know, I was up to almost $515k at one point last month. As I sit here today sadly I am at $490k again… becoming a half millionaire keeps eluding me, Ill have to stick to the hundredthousandaire moniker for now, I suppose it could be worse.

Anyway, pontificating further, I wonder if that statement applies to jobs you hate, or have grown tired of. I mean I’m at a crossroads here after a decade I’m thinking about leaving the place that brought me to the dance. I’m just so bored, and my upward mobility has dried up… In fact its causing me to have real anxiety, but I think I need to move on. I’ve been WFH for that time frame too but I think I am not doing myself any favors by sitting at home in my fortress of solitude everyday. I’m not necessarily a people person, but after a while I think it affects anyone. I have a really solid offer to go elsewhere and I accepted it, but sometimes I second guess myself, I wonder if I even have the skills to be successful elsewhere I’ve spent so much time in one place. Anyway, I’m not sure getting comfortable is a good thing, and I do believe this new job will be better for me in the long run. I guess its the fear of the unknown…

Wow – good for you man!! I agree it’s time to spice it up a bit! I was just watching Dolphin Tale II with the fam (don’t judge) and there’s a part there about staying in a nice comfy spot vs taking on opportunities that can be scary but we need to do them. So I think you should channel your inner dolphin and 100% go for it :)

And I’m with you on the lonely aspect of working from home…. which is exactly why I’m typing this at a coffee shop right now! It’s nice just to be *around* people, even if you don’t talk to them.

Yeah, I think the time has come too… It doesn’t feel real yet, which is weird. 4 more weeks and I’ll be somewhere else.

8 on top, 7 on sides, 6 on bottom. Takes about a day for my wife to get sick of the edges so she cleans it up for me. Set of Wahl clippers on amazon I bought 5 years ago for like $20. Good thing about hair is it always (usually?) grows back!

Woops – meant to reply to Bryan lol.

Anyway, March was nice for us because we finally hit a new all time high net worth for the first time in 6 months! We bought a new car last September, and the markets been a little wild as well. We do not include value of vehicles in our net worth on Personal Capital, only investments, cash, and home (but we do include the car loan!)

Oh wow – hardcore! Though better to be conservative than the opposite I suppose :) Congrats on the new high!

Thank you for the tips Stevo.

Like Stevo I only count cash, investments (including HSA since it’s penalty-free after 65), and the house. We tipped $635k in mid-March before people started freaking about the yield curve inversion, and we’re only around $10k down from that now. Eleven more years until we kill the mortgage and likely have a solid seven figures invested. I’m trying to enjoy the now and not get lost in how awesome FIRE will be down the road, but sometimes it’s tough…!

Haha yeah it is… But seeing that worth inch up over time definitely makes it a tad easier with each passing month :)

3 months later than projected, but finally crossed half a million.

BOOM!!!!

Way to go, G$!!

Hmmmmm…we too are considering a home purchase soon and are sitting $-wise very close to your net worth numbers which I also track monthly-ish. Wondering, do you also feel the angst I do about watching a big chunk of that NW drop the minute you take on a mortgage? That’s a normal feeling- right?

Haha, it is very normal, yes :)

Though depending on how you track it you shouldn’t see a drop of net worth? You’d just see cash go way down but equity go up which will even things out (minus any fees and what not you’d pay to seal the deal…)

I know some don’t like to put the values of their homes or cars in their reports though, in which case it will drastically tip the #’s when you go to add those mortgages in! Haha…

While your equity will more or less counterbalance your cash pull for the down payment, you’re adding in a large debt in the mortgage which will definitely lower your net worth. If you get a great deal and the house is worth a good amount more than the agreed upon sale price, it’ll at least lessen the impact.

My net worth this month wasn’t as great as it has been the past few months, but at least *almost* all our investments went up since last month! We did end up having some tuition costs we hadn’t anticipated and paying off a medical bill (meaning we’ve already met our deductible this year…yaaaaaay), but my husband is also getting a raise starting this month so it’s only up from here!

Well here’s to the next net worth report, then! :)

Do you ever plan to convert IRA money to ROTH IRA? I considered it for the 2018 tax year but didn’t want to pay the tax. Since my income will be lower when I stop working full time (next year, at age 67) do you think it would ever be a good idea for me? I only have about $150K in the IRA, most of my net worth comes from real estate income property (paid off!) Don’t like the idea of required distributions.

Once you stop working you could start converting small amounts each year that would not trigger a huge tax bill. Maybe 5-10K a year . . .

I know a lot of people in our community talk about Liz’s idea above of doing it slowly over the years… I haven’t personally thought about it much just because we’re so far away from retirement, but at some point I’ll have to be strategic about it :)

I went out to lunch with a buddy last week. His net worth now is $234,000,000 (yep, that’s million). Money made in one generation. Dad worked in a bakery. No bitcoin. No IPO. All from real estate. And he’s only 55.

Green monster of jealousy about that one I can tell you. On the other hand, our net worth is closing in on 8 digits – figure 5 or 6 more years ought to do it.

Two power players right there hanging out!! :)

I’m less than $3k away from hitting $100k in my 401k. I turn 30 later this year so I’m excited to hit this milestone while still in my 20s ;)

I read today that the median 401k for people 65+ is only $58k and it made me so sad…and proud of myself!

NICELY DONE!!!!

That’s one of the biggest milestones – it gets so much easier from here!

https://budgetsaresexy.com/the-first-100-thousand-is-the-hardest/

I was surprised to see we crossed another, let’s call it a mile marker instead of a mini milestone since we’re in this for the long haul and I’m trying to embrace the long termness, mile marker this month in our net worth. Happy but surprised.

I haven’t decided how often to update our house “value” from the purchase appraisal since it’s just paper value until/unless we sell but I do keep the bare minimum on the spreadsheet to counter the debt attached to it.

We also passed a significant mile marker on invested assets if you count JB’s college funds, which I do right now because I figure those are assets from which we’ll be covering a specific type of spending someday.

I’m otherwise hoarding cash a bit to prepare myself for whenever the recession hits.

Are home prices reasonable enough where you’re looking that your cash and brokerage balances could cover a down payment??

Congrats on the mile marker passing! ;) I like that, haha…

Housing – yes – VERY affordable, at least comparing to DC prices where I am now :) And probably the same comparing to where you are too!

It’s pretty interesting though… Some communities range from $300k-$400k for single family homes like most of the ones we’re looking at, but then literally next door you’ll have a community with $200k-$300k homes – which then tempts the pants off of me!! haha…

I keep trying to channel my inner frugality man, but of course the cheaper homes are smaller and not as nice so the trick is figuring out what *matches* our family better for the *long term* since we’re going to be sitting put for awhile… My renting mentality would just take the cheaper one since it wouldn’t be my home to own or care about, but when we’re talking ownership I really want one that EXCITES me!! Especially if I’m changing sides!! :)

So we’ll see… but yes, to answer your question – the prices are reasonable, haha…

We have hit a new mile marker ourselves as well! We actually hit it about six months ago, but then it went away thanks to the markets, and it appears to be back. Although the markets could take it away again. Anyway. I wanted to say that I have never updated the value on our houses (yes, we own two) in my personal spreadsheet but I do watch what Personal Capital does via Zillow. Because, like you, I feel it is only paper value until we sell, but I do want to balance the mortgages against them.

PC has us worth about $250K more than I do. And I’m okay with that…

It doesn’t suck to see :)

I love these statistics up top! I took them a little further so I could really grok them:

(the broken out numbers don’t add up to 13.3T, btw)

Mortgage debt per household (assuming 127.59 million households and 64% own)

$115,115

Non-mortgage debt per 18+ adult (assuming 327 million as the us population and 77% are adults)

$15,489

Credit card debt per 18+ adult (same assumptions)

$3,312

Student loan debt per 18+ adult (same assumptions, but i think these assumptions might not quite be an accurate representation of this statistic)

$5,441

Now those are much easier numbers to wrap your head around, haha…

(And good catch on the stats not totaling up! Looks like the auto #’s there should have been *trillion*, not *billion* – sorry about that. Just updated :))

New high-water mark: $940K, up $7.2K.

New highs in 18 out of the last 24 months.

Damn you’re so close!!!

By the end of the year you’ll turn into a Millionaire – woot!

If the market cooperates.

Trying not to get too emotionally invested in it being THIS year. But it is inevitable at some point if I keep doing what I’m doing. :)

Hey J,

I remember when your net worth updates were under $500k.. And now that million seems right around the corner! Keep it up brother.

– Chase

Hey, thanks man!

And for reading the blog for so long :)

Hi J,

Greetings from the UK!

A new reader to your blog and your progress updates have influenced me to make the first steps in working out my current net worth. First goal is now also set, to have a household net worth of £60,000 in 14 months time, linked in with turning 30.

Slightly different rules here, and houses are crazy expensive, but the principle is still the same.

What a day it will be when you hit the million.

Cheers.

Welcome to the party, Doug! I want an email as soon as you cross it – please :)

First time posting.

I’m just beginning my journey. Started tracking my net worth which sits at 4K about a year and a half ago using personal capital. It was just this past January when my net worth was positive for the first time. I’m will try to reach 15K by the end of 2019. I’m 25 years old.

Heyyy very cool man! Thanks for stopping by! And congrats on being in the positives now – should only be going up from here! :)