Haaaaaappy net worth day, y’all!

Who’s in the stock market right now and grinning from the massive comeback? Now who’s grinning even MORE because you scooped up mad stocks on sale and turbo’d your stock pile even more?? :)

That’s the beauty of the game right there, my friends… Gotta be “in it to win it!” as Randy Jackson would say! (Whoo whoo whoo! < — Dog pound chant a la American Idol, R.I.P.)

As for us, this month’s increase marked the 3rd best in the history of tracking my money and it feels damn good to be back in the running for that $500,000 spot again… something I’ve been chasing since May of last year!

In fact, here’s a look at the top 3 best increases over the years:

- October, 2013: $430,950.10 (+$62,000 – sold some sites)

- October, 2011: $262,425.97 (+$60,000 – mad hustlin’ + $20k inheritance)

- March, 2016: $488,217.20 (+$48,000 – market increase + $10k gift + maxed Ira)

And just to be fair, here’s our top 3 WORST months too :) Just to prove it’s not always glitter and rainbows up in here! We’ve had just as many lows as we’ve had highs over time…

- January, 2016: $437,562.07 (-$51,000 – sold house + market crash)

- June, 2013: $339,921.97 (-$40,000 – moved + renovated + lost income + markets down)

- August, 2015: $468,391.43 (-$23,000 – market crash!)

As you can see, 2016 has been quite a wild one so far! Down $50k one month, up $50k another!

Here’s the TL;DR of how March went down:

- Cashed out all Digit savings and Challenge Everything savings

- Cashed out remaining tax $$ that was set aside and left over from filling taxes

- I finally filed taxes :)

- I used all this money + a bulk of our cash reserves to max out my SEP IRA for 2015 ($25,563 worth)

- We got an unexpected gift of $10,000 from my in-laws!!

So a lot of cash transferring and investing this month which is pretty out of the ordinary. Things should calm down a bit more now that the house/cash shortage/investing dilemmas are all figured out, but you never really know what life has planned for us, eh? Gotta ride the times when they’re well, and brace yourself as best you can when they’re not! It should all work out fine in the end provided we keep our heads down and focused on the bigger picture… And hopefully your month went exceedingly well too :)

Here’s how March broke down in detail:

(PS: To all new people — I share these updates every month to not only hold myself accountable, but also to show a real-life account of someone else’s money. It was one of the coolest/craziest thing I’d ever seen when I first stumbled across this myself 8 years ago, and I found it to be super motivating so I decided to do the same when I started my own blog… Hopefully it helps/inspires you as well! :))

CASH SAVINGS (-$1,415.23): A small amount by looks, but a TON went down in the background to lock in this SEP IRA maxing. About $3,500 came from cashing out my Digit account, $2,000 from emptying our Challenge Everything account, $10,000 from last week’s unexpected gift!, and then another $10,000’ish leftover from my “tax account” that stays separate all year long and dumped out if anything’s left after taxes… And apparently I overestimated by quite a bit! (Better than the opposite though, eh?) A fun – and maddening – month all around, but a very happy ending when all was said and done, whew.

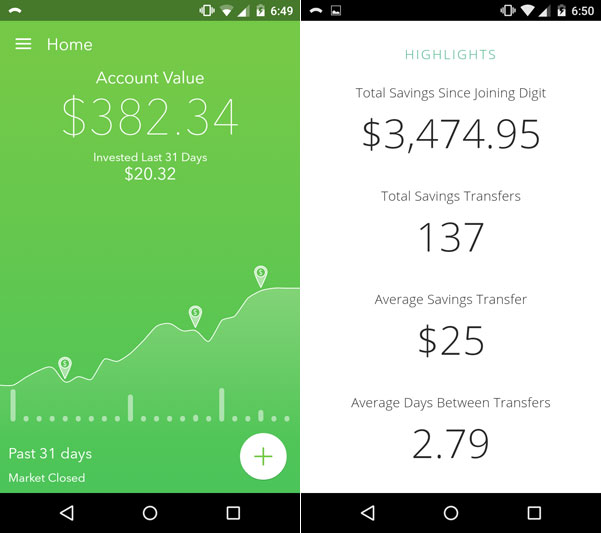

DIGIT SAVINGS (-$3,284.70): Whelp, after over 15 months of saving money with Digit it was finally time to put it to better use! We cashed it out this month and applied it right to our Vanguard investments, particularly VTSAX. A much better spot to hang out for the long term than a savings account, am I right? And we’ll continue to rock Digit to keep saving easily/automatically going forward too so we can do it all over again come this time next year :) If you’re interested in learning more about them, you can check out my review here: Digit: The Easiest Way to Save Money – Ever?

Here’s a snapshot of my account (on the right), along with Acorns (left) before I cashed out… Kinda neat seeing how it all broke down over time, eh?

CHALLENGE EVERYTHING (-$2,103.45): We said bye-bye to these savings too! Plucked them right from our separate savings account tied to our Challenge Everything mission and moved them right into more VTSAX funds with their friends. I’m debating on whether to keep this account open now that we’ve stopped really challenging stuff, but the rewards from Round I are still paying handsomely so we’ll see if it continues going here or just mingled with our main savings to get more minimalistically aligned.

BROKERAGE (ACORNS) (+$45.68): Still growing a little each month! Looks like our roundups totaled about $20 this month, while the funds increased $20 as well due to a rise in the marketplace… For those new to Acorns you can read my review here – Rounding Up Change + Investing It = Acorns App! – but this was my foray into starting a new brokerage account again and it’s been humming along in the background for about 12 months now. Happy birthday to J+A!

IRA: ROTH(s) (+$5,962.75): A nice uptick here too due to the markets, especially as nothing extra has been deposited in just about a year now… So far, anyways ;) I’m HIGHLY tempted to keep my record of maxing this out along with my SEP for the 5th or 6th time in a row here (such a great habit!!), but with our cash situation being as it is I just can’t justify it one iota – at least if I want to stay married to my wife. I am working on a new partnership though that will result in some extra cash around the corner, so if that pans out between now and April 15th (the last day you can drop money into a Roth for the 2015 year), it’ll be on like Kristin Wong!

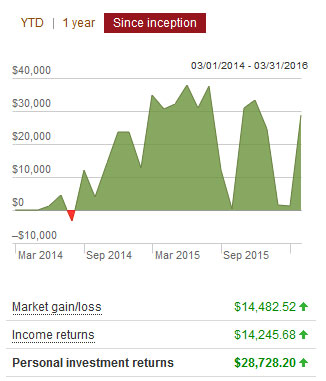

IRA: SEP (+$48,831.75): TRIPLE BOOM COCKTAIL! Haha… $25,000+ dropped in our Vanguard SEP IRA (again, all in VTSAX) along with a nice jump in returns – and dividends! – to boot. Imagine if this happened *every* month? :) Someone asked if I could share the dividend amounts as they hit too, and they just did which came out to an extra $1,896.81 in the accounts. For literally doing nothing (the beauty of investing right?). So needless to say this was a damn good month, and one severely needed with all the uncertainty from the past few months…

Here’s a snapshot right from my Vanguard account that shows how wild it’s been since we first moved over in 2014… The “income returns” part are the dividends since paid out:

AUTO VALUES (+$157.00): Yeah, I don’t know what’s up with that, haha… Just copying/pasting what Kelly Blue Book says! :) Here’s the value of both of our cars, if we were to sell them directly to someone ourselves (which is what we’ll do once time):

- Average Toyota (wife’s): $4,360.00

- Pimping Caddy (mine, of course): $1,000.00

LIABILITIES: None!!! No more house or loans or debs – nada! It’s pretty weird being totally one sided with these updates since I’m not used to it, but it’s something I hope stays as-is for the future years to come :) For those who think we figured out how to live mortgage/rent free, however, that is certainly not the case. While we don’t have mortgages anymore, it’s simply because we sold our house and went back to renting full-time… Perhaps not the best route for many people, but for us it’s heavenly. And something I’d like to continue doing so for however long my growing family will allow me to :)

How my two boys are doing – because why not?:

And that’s Net Worth Update #89! If you’d like to see the complete list of updates over the past 8+ years you can do so by clicking here, and if you’re tired of reading about me and want to see what other – probably much smarter – bloggers are doing, you can see our list of 200+ net worths here: The Ultimate Net Worth Tracker, powered by Rockstar Finance.

May the money Gods be with you this month!!! Keep hustling and learning and saving and paying attention to everything – it always gets better no matter your stage!

XOXO,

![]()

PS: If you’re just getting started in your journey, here are a few good resources to help track your money. Doesn’t matter which route you go, just that it ends up sticking!

- The "Budget/Net Worth" spreadsheet - the colorful Excel template I personally use.

- The "Money Snapshot" spreadsheet - a simple Excel template I created for my former $$$ clients

If you're not a spreadsheet guy like me and prefer something more automated (which is fine, whatever gets you to take action!), you can try your hand with a free Empower account instead (formerly Personal Capital)

Empower is a cool tool that connects with your bank & investment accounts to give you an automated way to track your net worth. You'll get a crystal clear picture of how your spending and investments affect your financial goals (early retirement?), and it's super easy to use.

It only takes a couple minutes to set up and you can grab your free account here. They also do a lot of other cool stuff as well which my early retired friend Justin covers in our full review of Empower - check it out here: Why I Use Empower Almost Every Single Day.

Get blog posts automatically emailed to you!

Stock market going up helps a ton! I don’t worry about it as much as I used to though. After seeing the tip of the iceberg with the #PanamaPapers, it just goes to show you that the worldwide economy is rigged and you’re going to be hard pressed to beat it.

Focus on reducing your spending and all of a sudden these worldly issues don’t impact you as much!

Hell yeah – gotta focus on the stuff you can control!

I was wondering what the plan was for the digit and challenge everything savings funds. Nicely done adding $5K to the investment pile. So how does it feel to have no liabilities? Do you regret not unloading the house sooner?

Feels great and strange all at once – not used to it, ya know?

Nah – no regrets on not offloading house sooner. Just wasn’t the right time and didn’t have a real impetus to do so until our renter gave us notice… Up until this point the plan was to just hold onto it until we can break even one day w/ a sale, but once it got stuck in our minds that we’d be okay PAYING to have it gone the excitement levels rose and then we pulled the trigger :) I don’t think we were ready to go down that path until that point.

It’s interesting that you include your car value in your net worth. May I ask why?

Sure, cuz one day we’ll be selling them for the prices roughly listed above (or whatever they’re worth at the time we’re getting rid of them). I know some people don’t like including them, as well as other things like jewelry or art/collections or even houses, so it’s one of those things you just have to see if makes sense for your situation and tracking purposes. No right or wrong way to really do it :)

Good month!

we don’t have enough in our retirement accounts (yet) to see 5 digit swings. I can imagine the first time seeing -10k scares the hell out of you.

I will have to check out digit, I started using acorns last month – well designed app

Yeah, it does sting the first couple of times but then gets much easier as time goes on… Especially when you have the opposite swings up + $20k, $30k, or even $40k! Important thing to know is that none of it matters until it’s time to take it out so to keep head down and hustling as best you can :)

Holy, crap congrats!

It goes to show you that it is better to invest with a steady hand than get shaken out after every market move.

It’s great to see people’s net worth bouncing back this month. You are getting so close to your goal–congrats!

Congrats J Money! I am actually very surprised to see an automobile’s value increase! That is super rare. Got any idea why? It was a great move on your part to throw money into the stock market, or should I say Mutual Funds through Vanguard, instead of savings accounts.

One quick remark, while renting is very beneficial, and quite frankly the new trend, it may be better to buy a house you can see yourself settling down in, at least to increase your long-term net worth.

PS. I am just as happy as you about this stock market rebound haha. Was super worried the beginning of the year but managed to snag some companies at their low and seeing the huge gains now. Keep up the great work and hope you reach your target soon!

Car value – no idea! I don’t put much stock in it really – I know it’ll be going back down every month going forward :)

Renting – if we knew where we’d be living and for how long I’d def. consider it again, but right now everything’s in transition so just enjoying the freedom and going with the flow… If we settle down somewhere then I’ll start looking again… But mostly at tiny homes :)

Here’s hoping the Number actually crosses the half-a-mil milestone this time! You’ve been close enough to smell it a couple times before.

You’ve had one of your worst and best months ever already in ’16, which is normal as the stash grows. As the nest egg grows, so do the daily and monthly swings. Enjoy the ride.

You would know too! Any plans on sharing your #’s on ye ol’ blog? ;)

I’m 7 months into my first year of keeping track of our actual expenses on Mint. I had a decent estimate in the past based on the monthly CC bills, but I’ll have an all encompassing breakdown 5 months from now, and I plan to post about that. We’ve had a lot of what seem like one-time or hardly-ever expenses, which I think is probably true every year.

Anyway, I plan on revealing our expenses, and the fact that we’ve got at least 25x that, but I’m not sure I want the specific number out there. I may not remain anonymous forever.

OurNextLife does a nice job of posting their numbers in terms of percentages, and offers an excellent explanation why they don’t post actual numbers, which echo my feelings on the subject. That being said, my inner voyeur appreciates how open you & others are.

Yea so I’m that unlucky guy who drops in a ton of cash into the stock market a month before it crashes…twice in a row. I did it in 2008 and I did it again last year.

I always re-leverage and buy up more to get back to even faster…the first time I lost half my value so I kept dumping in money every time the market dropped another 10%. I sold as soon as I got back to even…

Then I invested in real estate and made a fortune.. Love real estate.

So I started diversifying again and plunked some change down into the market…well I haven’t hit even yet..but this time it’s in there for the long haul..hoping that this little crash got my cost average down far enough that I can earn some decent returns in say…20 years. Good thing real estate makes me money Today.

And that’s exactly why I don’t even TRY to time the market! Haha… I’ve sucked more times than I’ve succeeded too over the years – you’re definitely not alone :)

Now I just invest whenever I have the money to invest and don’t even look at the trends or highs/lows/etc… And also why I only stick to Index funds now – my skills at stock-picking are equally as dismal (except for the time I copied Warren Buffett – that was fun!).

Good job mastering real estate – I admire those of y’all who have.

(a month later, I know) Honestly, I wasn’t even trying to time it. I just realized I had some money and I should do something with it. It was in the summer of 2008, sometime in August. I picked a very one aggressive fund and one conservative fund and split my money between the two.

Then September rolled around and the whole financial system collapsed. Great job Eric… Luckily they each did what they were supposed to do, the aggressive fund dropped like a rock and the conservative fund went down but held it’s own. As the market kept dropping, I kept moving funds from the conservative fund into the aggressive fund. Did it several times until….I had no money left in the conservative fund and my aggressive fund was worth half of what I started with.

Fortunately there was a bounce some time later, don’t remember when and my value shot up since I was 100% in on the aggressive fund. I sold everything when I broke even finally… and subsequently missed out on the biggest bull market ever. Great job again Eric..

Fortunately real estate far outperformed the market so I would have missed out on that if I had been all in on the market..

Interesting ride to say the least.

Indeed! Glad there was some positive stuff that came out of it for you :)

Dude, you’ve most definitely got in-laws as opposed to out-laws! Congrats on a great month!

Hah – indeed!

It goes to show staying the course will pay off eventually. 500K is right around the corner. 89th over share of money, TMI buddy. Haha. 10k gift is awesome, wished I had some cool in-laws like that. Now that your mortgage free, whats the next step?

Helping my wife land her first job back into the workforce! Our wallets are going to explode when that happens, haha… been like 6 years on just one income the whole time – can’t even remember what it was like :)

A few thoughts:

1. Congrats! You’re almost at the half million point!!!

2. I got all the cash I could and invested it in the market at this most recent big drop — just like I did in 2008. Both moves have paid off handsomely.

3. After 20 years of investing, the stock market controls my net worth. Every 100 points on the Dow is roughly $10,000 gained or lost.

4. For net worth I include every thing I own and everything I owe (which is only credit cards that I pay off monthly). This includes cars. I depreciate them rapidly and even depreciate my house to the value I’d get from it if I sold and had to pay RE fees, but I still include everything. Because I could sell them after all, right?

That’s exactly why I include all those too. Except for any property/belongings – but I should probably include my coin collection as I could easily liquidate that at any point and get a decent return… Might get too tired of explaining it though adding it on the blog haha….

Interesting about the 100 pts correlation!

Wow, that number is close to the average salary per person for a full year !

That’s very impressive.

Keep on the good work.

Woah – crazy when you put it in that perspective!

Congrats man! I agree with you about using the car value in the net worth. If it all hits the fan and you need to sell, that’s worth something.

Why include cars in net worth, but not TVs, furniture, etc? All could be liquidated for something, and are depreciating assets.

Yeah, I suppose so… We don’t own anything valued at over $100 though outside of our TV and maybe a couch. So we’d probably donate or just sell for a fraction on CL if need be, and in which case not going to amount to much in a net worth calculation anyways.

The only thing I may include in the future is my coin collection which is def. worth something and can be liquidated pretty easily if need be (huge market for old coins online). But not sure I’d want to answer all the questions about it every month in these reports, haha….

Awesome! I’m still pulling together my March numbers, but so far we’re looking at $90k+ net worth gains. That’s a very different story than the past several months for sure!

Beautiful man! That’s huge!

I have heard good things about Digit. I’m leaning towards starting one just to see if I can save some additional money. I mean it can’t hurt right? Little here, little there.

For sure! You can always cash out and just close it down if you find it’s not working well for you… But if you find it helps? Could be a good extra way to save up for things. Let me know if you end up doing it, and what you think after a few weeks!

Guess what? I signed up for a Digit account. And I am so close in convincing my coworker, who does not do a good job saving, to open one up.

SCORE! You should see who can save more over the year, haha… loser buys drinks for the other one :) (or better yet – winner buys drinks since they have the most $$$!)

Awesome. Watching the net worth go up $50k has to feel pretty sweet. Probably just a tiny bit better than watching it drop $50k, I’m sure.

In some ways, I’m thankful my investments aren’t big enough to suffer such big swings. And then, at the same time, I’m a little sad my investments aren’t big enough to suffer such big swings. :(

Wow… That is amazing. Congratulations.

Me too, I did better, but not as good as you.

Looking forward to the next month.

You make the end of the months exiting.

Here is my Net worth.

http://www.alainguillot.com/net-worth-april-2016/

Interesting about all the changes that happened to you in March! Hope your $$$ continues to grow!

I know you mentioned not being able to justify maxing out the Roth IRA with the current cash savings situation but wouldn’t you be able to pull out any contributions you have made tax free if you started the IRA over 5 years ago? I am not sure if you have been funding your Roth IRA that long but if so it seems like you could use it as a pseudo savings account while still getting the benefits of the market gains.

Just a thought.

Yup, this is very true! I wouldn’t dare touch it because it’s a slippery slope and would only tempt me to pull from it again over and over again, but yes – technically I can pull out all the $$ invested over the years which would be a hefty amount.

I like the way you think (but stop tempting me :)).

I’m curious why you don’t contribute to your SEP or Roth IRAs at all throughout the year. I understand why you wouldn’t want to contribute the full say $25k throughout the year but even just doing the Roth IRA that way or say $500/month to your SEP IRA might feel easier than all in one chunk, no? Also, then you’d have longer time in market.

I mainly don’t do it because I never know how well – or not – the year will go in terms of income/life/kids/etc, but you’re totally right – would make things MUCH easier (and financially better!) if we dollar cost averaged throughout the year for sure. Either with the SEP or ROTH or even both! I might start going that route w/ the Roth this year and see how it goes, just want to get over this little transition here and get back on track again… Smart idea though – I wholeheartedly agree :)

Looks like a great month! I have to look into Acorns. I’ve heard such great things about that service.

Congrats on an awesome month!

I really want to jump on the Digit bandwagon but apparently my local credit union is like Fort Knox and has some pretty intense security stuff that isn’t compatible right now. Maybe someday…

They’re pretty good at adding new banks/unions over time – especially as they see a ton of people trying to get access – so hopefully it opens up for ya soon! USAA had some pretty rigorous security as well but thankfully got figured out :)

The market going up is certainly helping our net worth numbers. It’s nice to see the increase for sure.

Just to add, I really wish Personal Capital would work for us Canadians. Feel that we get shafted by these great products all the time. :(

I wish they would all open up for you guys too :( I swear they all say they will be down the line, but have yet to see any of them move over… Not sure why that is? Maybe regulations of some sort?

Same here Me Tawcan sir, doesn’t work in the UK either. And it. Looks. So. Awesome!

Those are some beautiful numbers, and its awesome that you overestimated your taxes. I overwithheld from my day job, but the hustle/rental properties mean that I have to pay some taxes this week (hopefully my accountant gets back to me in the next day or two).

Here’s to hoping that you crack the $500K this week!

Wow! You had an awesome March! Happy Net Worth Day indeed!

Good luck on hitting $500k. My goal is to hit $100k by the end of the year. A month ago I didn’t think I had a chance, but if things keep going the way they are I will definitely hit it!

I hope you hit it, friend :)

I was excited calculating mine on the first of April. I just started last month and was depressed to see we were starting at -$59,860.80. But just one month later we are at -$50,659.39. That’s huge for us with a gain of $9,201.41. I also just started digit about halfway through March and that gave us almost $40 in just 2 weeks. I’m already looking forward to next month because I cancelled a car warranty we had bought less than 60 days ago and were able to return. Car warranty equals the second dumbest financial decision I’ve ever made right behind leasing a car. That means the refund will drop that debt by $2,000 for the first of May. Onwards and upward, even if upward means making to a flat $0!

Damn straight! Gotta start the journey somewhere, right?? As long as you’re trending upward you’re on the right track! :)

Thanks for the digit post. I’m obsessed!

I still don’t understand how you’re freely sharing your net worth. Although I think people can guess mine based on what I wrote, I still feel this is very personal and the kind of level I’m not willing to share.

Good for you though, and awesome progress this month :)

It helps going anonymously :) I don’t know how all those people do it attached with their real names! There are some creepers out there…

I’m retired, a couple of decades and a couple of million ahead of you because what you are doing works! Live frugally and save aggressively and invest wisely and you will win. Your are doing such good work and offering financial hope and wisdom to thousands of people with humor and kindness. Thanks so much for that. I doubt you know the impact you have on so many people’s lives. Thanks for what you do.

Hey, thanks man! So kind of you to say!! And congrats on figuring it all out yourself many moons ago… perhaps if blogging were around then you’d have had your own blog too sharing the wealth :) (Hell, you could start one now in all your glorious free time if you wanted – hah)

That graph showing the last 12 months of NetWorth really shows what a volatile ride it can be! Like there’s some huge NetWorth wrestler waiting around the $500k mark that keeps on drop kicking you whenever you get near.

Crazy swing this month…for the good :)

hah – it certainly feels like that :)

It is nice to see your net worth rebounding. Putting so much in a SEP IRA is pretty sweet. I am not sure if I had asked you before, but have you thought about opening up a solo 401k and potentially soaking up even more $$$ for retirement?

Have you looked at your quarterly dividend income since you moved to Vanguard? I bet it was more stable than that roller coaster of up $50K down $50K :-)

That Vanguard snapshot above highlights the total amount of dividends since moving over :) Looks to be a tad over $14,000! For doing nothing! Haha…

Solo 401k – To be honest I haven’t looked into it much since I can barely max out my SEP each year lately anyways, but yes – def. on the list to consider as soon as my income rises and/or my wife gets back into the workforce! Which hopefully will be soon!

Hi J$,

What I mean is to take a snapshot of portfolio value and dividend income each quarter. Then check how they “behave” relative to each other. The chart you included shows life to date amounts.

Based on my calculations, you made that much in dividends per quarter:

Qtr End Dividend/Quarter

Mar-16 $1,896.81

Dec-15 $2,281.33

Sep-15 $1,980.81

Jun-15 $1,820.62

Mar-15 $1,937.59

Dec-14 $2,075.07

Sep-14 $2,253.45

This is the cumulative amount per Qtr:

Qtr End Dividends Cap Gains

Mar-16 $14,245.68 $14,482.52

Dec-15 $12,348.87 $12,334.34

Sep-15 $10,067.54 $(10,190.64)

Jun-15 $8,086.73 $29,044.53

Mar-15 $6,266.11 $26,914.49

Dec-14 $4,328.52 $18,687.08

Sep-14 $2,253.45 $2,731.45

Ahhh gotcha gotcha.

That’s pretty cool looking at it that way for sure. Thx for spelling it all out for me – I’m a bit slow at times :)

J, man, come on now. Max out that Roth. It can stay in cash, you can pull it if you need it with no penalty (remember you’ve had the accounts for five tax years). Come on…. :)

I’ll even help convince your wife for you, it will be just like your challenge everything fund, technically separate but can be used if needed.

If I max it out no one is telling my wife yet! One bomb at a time, please, haha…

(but you are helping to sway me, yes :))

Great numbers. Our net worth increased nicely as well thanks to the market. We got a 7% net worth increase.

Nice :). I’m looking at some Tesla shares going up at the moment – a bargain bought in mid February (60% up since then).

Hope you know when a good time to cash out is! That was always my downfall, I had horrible timing when trying to play that game…

This is what I’ve been thinking, J.; the fun part is over and now is time to learn when to ‘fold ’em’. Watch this space.

Investing in VTSAX for the long term is awesome. You get happy when the markets go down because the shares are on sale. And you get happy when the market goes up because you’re making money. Happy time all around!

I got an unexpected bonus at work which I used to max out my Roth…for 2016! So that’s a 2 year streak of maxing that out since 2015 was the first time I was able to do it. I hope to keep it going next year (and hopefully they increase the flippin max contribution this time!)

Great job and appreciate the peak behind the curtain.

Beautiful!! And agree – it’s been pretty low for a while?

You’re so close to that $500,000 goal! Perhaps this will be the month? It’s very good that you display both the ups and the downs of your progress – and the overall win that we can all anticipate if we stick with it and keep emotions out of it. Here’s hoping that April brings you to your half-million goal!

hi there, I’m curious about the decision to have a SEP vs. an individual 401k…I haven’t been around all your posts so don’t know if it’s covered. I have my Roth with Vanguard and (finally!) have enough money to contribute to a retirement account from my side business after contributing only to a Roth and employer plan. I called Vanguard, and they walked me though all the options and strongly suggested the Individual 401k vs. the SEP IRA for sole proprietors. Any thoughts?

I haven’t poked around it as much as I should yet, but from everyone I hear that has one LOVES it. Mainly cuz you can put in more $$$ than you can w/ a SEP. I can barely max out my SEP these days so I haven’t jumped into learning more/switching over, but once that changes I’ll def. be poking around :) Go with the one that best fits your situation! Smart to ask Vanguard about it for sure – that’s what I do as well when needing help with stuff.

Way to go on such an awesome month J! I still think the best part is the big fat ol’ ZERO in the liabilities column. That must be so rewarding to have it all gone. Great job! Half a millionaire has a nice ring to it. :)

Darn buddy, your getting awfully close to that half million dollar mark! Pretty sweet.

Keep it up.

“…at least if I want to stay married to my wife. I am working on a new partnership though that will result in some extra cash around the corner, so if that pans out between now and April 15th…”

Man, did I initially misunderstand that sentence ;-)

Hah! Partnership as in with another person I take it?? :) No plans on swapping her out in the near future, haha…

Wow close to 10% increase is amazing. Great job. My net worth was up by 9% as well in March jacking up my networth by $13,000. Hopefully this trend continues although I feel there are less and less bargains in the market lately. :)

Cheers!

BSR

Whenever I think about having no bargains I just look back in time and see how EVERYTHING used to be on sale :) It will be the same for us years/decades from now! (So long as no apocalypses pop up…)

Nice!! Up $48K in one month is awesome! Even if this is mostly just due to the market, you gotta love it!

Looking sharp! Gotta love free cash flow with no debt :)

You should move your entire stock portfolio to cash, this last rally is a typical dead cat bounce in a bear market. The strongest rallies to the upside always occur in bear markets. You are celebrating something that will disappear soon. The crash coming withing the next year will be much worse than the 2008 crash, that was just a warm up!

Nope – I’m done trying to time the market. Even if you know when to get out you never know when to get back in again to recoup the losses. I’m in it for the long haul so even if a bigger crash IS looming in the future, it’ll just mean more opportunity to scoop up everything on sale while waiting for it to go back up again! As long as you believe the markets solid for the long term I don’t ever suggest cashing out and back in again… If you believe it’s all going to crap and the markets are failing, then by all means – do what you have to do :)

Great update, My brother and I are looking to follow your accountability method and post our finances on our website in the near future.

Thank you for the inspiration!!

Very cool! When you do, let me know and we’ll add you to our epic Net Worth Tracker – where we showcase all the blogs featuring it :)

http://rockstarfinance.com/blogger-net-worths/