Woo hoo, it’s official! I’ve changed contracts at work and my new 401k retirement plan is being set up next month.

I want to share with you guys the plan overview, cool and interesting things I learned reading the benefits brochure, sneaky fees and stuff to watch out for, and my brief chat with the plan administrator. 🤓

At first glance: Reading the boring 401k brochure

Imagine my excitement when I opened the benefits brochure and read the headline: “Profit Sharing” 401(k) Plan!

Profit sharing!? Did I just join some awesome company that will split some profits with me?

Sadly, I found out the answer is No. Although the plan itself is called a “Profit Sharing” Plan, that just means it has sharing capabilities … the company I work with chooses to share zero profits with me. :(

Similarly, the first few brochure pages talk about employer-matched contributions … but again, even though this plan is capable of employer matching, it’s not something that will be acted on at this time. So it looks like no free money for me :( If I want this 401k account to grow, I need to contribute everything myself!

One more sucky thing I realized right away — the plan only kicks in on the 1st of the month, after completing 30 days of service. So even though Aug 10th was my official start date on my new contract, my 401k won’t actually start until October 1st. Seems like forever away!

Bummer, but I’m still excited to have this benefit option. It’s the only pre-tax retirement account I will be contributing to.

Here’s some more info:

Automatic 401k enrollment a.k.a. forced savings!

One cool thing I noticed and love … This plan has automatic enrollment for new hires. What this means is when a new employee is hired, the company automatically enrolls them in a 401k plan. It starts with a contribution rate of 6% of their annual salary!

What I love about this is a) I don’t have to set up an account manually — the onboarding process takes care of it all for me — and b) the average American that pays no attention to their retirement benefits is forced to open a 401k and start investing. Employees have to purposefully “opt out” if they don’t want to participate.

Vanguard says 401k participation rates nearly double (to 93%) when companies use auto-enroll, compared with 47% participation when employees voluntarily choose to save. If the company I worked for 10 years ago had this set up, I’m sure I would have been part of the 93%, and I might have had a bigger retirement savings pile today.

More companies should do auto-enroll retirement benefits!

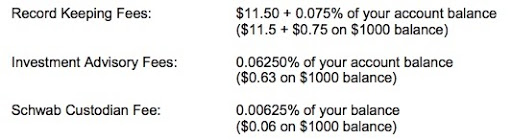

Administration fee disclosure

Here’s the plan sponsor fee breakdown. This is on a quarterly basis, not annual fees:

*This doesn’t include fees for the investment fund itself. These are just admin fees for having an active account.

At first glance these seem minor, but it adds up quickly. If I had a $20,000 balance in this 401k plan, the annual fee would be:

Record Keeping: $11.50 x 4 quarters = ($46) + $15 x 4 quarters = ($60)

Advisory Fees: $12.60 x 4 = ($50.4)

Schwab Custodian Fee: $1.20 x 4 = ($4.80)

Total Admin Fees: $161 (annual)

**Quick note to anyone with old 401k accounts from previous employers. These are the types of tiny fees that seem small but can add up a lot over time (and yours might be higher). You can usually transfer (or roll over) your old 401(k) accounts to Regular IRAs at large brokerage firms with FREE account and admin fees. No matter the balance, it’s worth consolidating any/all of your old 401ks into one retirement account. Why pay when you can have it for free?!

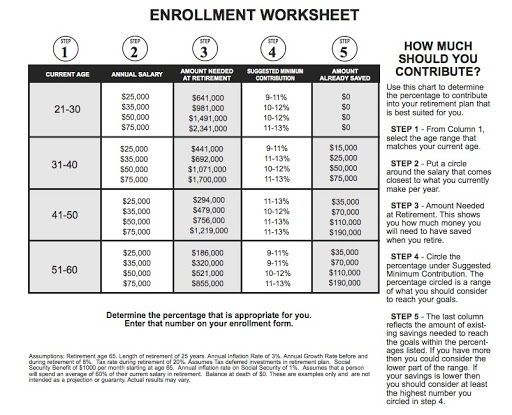

“Suggested contributions” to a 401k plan

The brochure includes all types of fun graphs and basic information on how saving is a good thing to do. It talks about compound interest, inflation, stocks vs. bonds, etc. Then comes a fun section about how much you should contribute to your 401k or retirement plan.

Here’s a worksheet the brochure provides:

I found this chart interesting for a few reasons:

- First, I noticed that all the contribution rates are between 9-13 percent. Doesn’t matter your age, income, current net worth, it all comes down to a minimum of 9% and a max of 13%. 🤔 Hmmm.

- There are a crap ton of assumptions in the footnotes for inflation rates, growth rates, assumed social security, tax rates, spending percentages, etc. Looks like a fair bit of wiggle room in there.

- It doesn’t explain how the “amount needed to retire” is calculated. This isn’t a bad thing, most people don’t know what the 4% rule is and have no clue how much they need to retire with. So at least this gives them a $ figure to think about and shoot for.

- It looks like nobody at this company earns more than $75k per year? 😳

As pretty as this chart is, these recommended contributions won’t work for me. FIRE folk need to think outside the box and consider their entire net worth and overall investment objectives. Whilst 9-13% may be OK for 401k contributions, I believe most people looking to retire early have a much higher savings rate — split across pre tax and post tax investment vehicles.

For me, I’m still thinking about my contribution allocation for this 401k and will share more soon!

Choosing an investment option

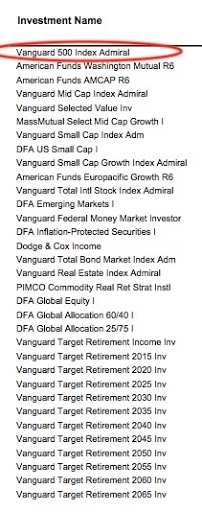

There are about 30 available funds to choose from. Here’s a list of them all. Each investment option came with a long and boring summary page of what the fund is about, past returns, how it’s diversified, etc. I didn’t bother reading into them because I spotted the one I wanted right away … at the top of the list! The Vanguard 500 Index Admiral fund.

Here’s a Google snapshot of this fund: VFIAX

Note the low expense ratio of 0.04%. VFIAX is a good fit for me because of those low expenses, and it uses a passive management — or indexing — approach to track the S&P 500 Index.

*Note, if I didn’t purposefully select a fund myself, I would be auto-enrolled into a target date retirement fund. Since I’m 35 years old, they would assume I would retire at age 65 in the year 2050 … And the fund they would auto-select for me would be VFIFX. It has a little more conservative approach than VFIAX and an expense ratio of 0.15% instead of 0.04%.

Questions for the 401k plan administrator:

The benefits brochure had a few contacts listed inside for a financial advisor and the 401k plan administrator. Just out of curiosity, I called the admin for a quick chat.

Here’s a few things I asked him:

- The brochure I received was from 2018. So my first question was if there was a more current one. He assured me no options had changed and I had the latest info.

- I asked about the employer contribution and profit sharing — just to confirm I had read everything right. Unfortunately, he confirmed there was no matching :(

- Since I didn’t have access to the online portal yet (still don’t actually), I was curious what the process is to change my contribution %, swap investment funds, and how long that stuff takes. Good news here — it’s all relatively quick and easy in the self serve portal. Changes take effect in the immediate next pay period.

- I asked if the plan sponsor (or my employer) had a maximum contribution amount. They don’t, as long as I don’t go over the IRS contribution limit, which is $19,500 for 2020. (Some companies don’t allow you to do a 100% salary deferral — which I am considering for the remainder of 2020 to stay in the lowest income tax bracket.)

- I asked “what happens to my account if I leave the company?” and if there were any fees to move away from them. (There are no fees, and if I leave, the fund stays invested in whatever it’s left in.)

- Lastly, we talked a little about additional *after tax* contributions which the plan allows. Honestly, I’m still a little confused about this and I don’t earn enough income to mess around with that stuff just yet. I’ll stick with my Roth IRA for now!

TLDR & all things considered

- I’m a big boy now, got a new 401k plan! Woot woot!

- But there’s no matching or employer contribution :(

- Decent available investment funds → I’m gonna invest all in VFIAX (tracks sp500)

- Regular retirement advice in benefits brochures isn’t fit for FIRE enthusiasts

- If you have an old 401k account with a previous employer, roll that $$ over and avoid some fees!

- Call your 401k plan admin if you’re ever confused. Grill them with questions — they love it!

- This is my only pre tax retirement plan that I will be contributing to. It’ll be starting at $0, let’s track this sucker over time!

PS. Nowhere within the 66 page benefits package did it mention the words financial independence, financial freedom, *early retirement*, savings rate, safe withdrawal rate, or any of the $exy words that FI folk use on a daily basis. Kind of sad :( It’s time these benefits brochures get a big face lift! Don’t you think?

*Photo up top by Urban Data on Flickr. Cheers!

Get blog posts automatically emailed to you!

Great article. Joel, with the ability to make after tax contributions and if you’re able to also make in-service distributions where you are able to rollover your after tax vested balance from your 401K plan to a Roth IRA, then you will be able to make a mega back door Roth IRA contribution. You would be even more of an Icon to the FI world. You could rollover funds to your Roth IRA after you max it out with regular or regular back door contributions of $6000.

I don’t believe this plan allows in-service distributions… Also (correct me if i’m wrong) I don’t think I’m eligible to do mega-backdoor because I have a regular IRA in my name. I think I would need to do a regular backdoor Roth first from my reg IRA, and pay the taxes. It will be many years before I even come close to Icon status in the FI world :)

Joel, thanks for sharing your 401k plan information. I found it interesting that your employer doesn’t provide a match. This at least give you a pre-tax option and another bucket to place your income and reduce your tax burden.

Timias

It’s definitely great to have a pre-tax option – even without matching. My overall portfolio is mostly post-tax accounts and real estate assets. So I can put money in this 401k knowing that I probably won’t need to touch it “early” anyway.

This reminds me of my first 401(k). I was eligible the first day of the month after six full months of employment. Then my company was bought in my fourth month of employment, and my offer letter mistakenly said 401(k) eligibility was to begin immediately; I got loopholed into starting early. So I started putting 20% of my salary in (compared to my colleagues in the 3%-7% range). They were kind of aghast that I was throwing so much money into what seemed in 2008 like a black hole. My wife and I just tripped half a million in invested assets last week. WHO’S LAUGHING NOW!?

Very good questions for the administrator. I wish I’d known to ask that sort of thing back in the day!

YEEEEEES!! Congrats to you and the wife on passing the 1/2M mark! I hope your friends realize that the *next best* time to start investing is right now. :)

Those fees are obscene.

I feel fortunate that my Fortune 100 company charges a flat $5/month in fees.

Any open positions that might suit me? ;)

I started a new job back in June. But I’m not eligible to join the retirement plan for an entire year. Yuck. Still contributing to my Roth until that kicks in.

Whoa – I will stop complaining then! From what I hear, (and I hope it’s true for you) the employers that have the longest waiting periods are the ones that offer the best reward plans afterwards. Glad you’re still crushing the Roth in the meantime!

No employer match is a real bummer, and those fees are quite high compared to the quarterly fees in my past 401k plans. Maybe Frankie is onto something if they offer the ability to do in service distributions (which I believe is rare), but if you could even transfer funds into a Traditional IRA to avoid the taxes it might still work out better for you. I’d want to keep my balances in that account lower if I could. Just out of curiosity, I noticed that you chose to go with an S&P500 fund as opposed to trying to do something like piece meal together something that might mirror VTSAX – Total Stock Market fund, and avoided any type of bond funds. I’m curious what drove your thoughts on that. Some of those funds mirror what I have in my own 401k. I ended up adding a Mid-Cap and a Vanguard Small Cap to try and get the Total Stock Market (plus a Bond Fund). Honestly, I’ve been debating that Mid-Cap since the fees are higher. Thanks for sharing what you asked the advisor!

Cheers J! I guess the reason I chose SP500 is because of simplicity. The more I try to piece meal things or build my own portfolio, the more likely I am to screw it up for myself. I was hoping for something I could just set-and-forget. No rebalancing, no doubting myself later, no additional fees.. You’re probably right about more exposure to mid cap and small cap could be good. But since sp500 covers ~75% of the total stock market, I think the performance is close enough to each other. Another thing I could have chosen is the target retirement fund for 2065. It has about 55% VTSAX and 35% total international market. Fees are higher, but I wouldn’t have to rebalance would have access to more stocks.

Thanks, Joel! I hear you on the rebalancing. I believe some plans will allow you to automatically rebalance your investments if you want, but not all. I can also empathize with the simplicity. My own 401k’s are…not simplistic. When I first started working in a different field than I’m in now (I’m a year or two older than you) I thought I’d diversify by just picking between 8-10 different funds in my company 401k’s. And I have 3! But I am working on paring things down more over time. Even with everything I know now, and a CPA license, I can still rationalize my crazy with the best of them!

3 x 401k’s? Can you roll them over into just 1 account? Embrace your crazy – it’s what makes life fun!

That’s good that you have access to Vanguard funds. Some 401ks give you high fee options only. My last employer had a mass mutual plan that was set up like that. It was total garbage. Fees can really destroy your long term returns so having Vanguard options shows your employer actually cares. I did a simple write up in what long term damage is done by high fees at https://www.dollartrak.com/how-do-mutual-fund-fees-impact-performance/.

As far as profit sharing , I think that just means they can cancel their match if the company doesn’t meet business objectives.

This is the first time I’ve had Vanguard options inside a 401k. I’m stocked for sure. It could be much worse!

Great article JOEL! I really like the detail you go into.

I also love how you talk about choosing a fund. I was mislead by a “financial advisor” that my firm hired to give members of my company “advice”.

This “advisor” told me to put my money in a T. Rowe Price Target Date Fund. His logic sounded good to me, but after I looked into it i saw the problems. The rate of return was awful! While the S&P 500 was gaining 10% over the past 5 years this fund was gaining ~4 %. Also, the expense on the T. Rowe Price fund is 0.7 %.

Well, we all learn from our mistakes!! I noticed my company had a fund called VINIX, which is very similar to JOEL’s VFIAX. It is Vanguard’s Institutional Fund at 0.035 % expense. I switched to that in March and have road the recovery UP!!!

Whether people use financial advisors or not, self education is always important. The more we learn and take ownership of our finances the better off we are. I used to find this stuff so confusing (still do haha) but I’m slowly getting better and better. That’s great about VINIX – it’s almost identical!

I’m not sure if you mentioned what type of company you work for, but this looks like a plan that would be offered at a start up or other small company with very few employees. The fees are, as others have noted, pretty ridiculous. I would ask your human resources department to investigate finding another 401(k) provider with lower fees. At least you have fund options that have minimal fees. No match sucks and, again, this sounds like you are with a small company. Honestly, if there is no match and with those high fees, you may do better opening up a traditional IRA on your own. The drawback there is you are only allowed to contribute $6000 to one, so if you are planning to put more than that into your 401(k), that might be the way to go – even with the high fees.

Thanks Shaun! Since I’ve already maxed out my ROTH IRA’s, the traditional IRA isn’t an option for me. I could work out a SEP IRA situation, but then i’m limited to a max of 25% of my income (which is quite small). So this 401k, as bland as it is, probably is the best option. At least I get to lower my taxable income this year – I’m planning to do some capital gains harvesting in my taxable accounts which is nice :)

As for calling the HR team to complain… I’m gonna wait until I’ve been employed for at least 2 weeks before I make a scene :) I definitely will bring it up though – I’ll even work overtime to help them evaluate options that are better for all!

I really wish my company had auto-enrolled me in their plan when I started. I had my head in the sand and was justifiably worried about paying the bills, but smaller percentages are barely noticeable because of the pre-tax benefits. Sometimes you just need to be told what’s best for you!

Looking back, I probably was told what to do. But I either ignored it or thought I was smarter than whatever advice I got. Now I am playing catch-up! Oh well, better late than never!

Nice job and congrats!

Following the S&P 500 for you was golden. All fees still the same? I assume you’ll be finding that out, as I am sure you’ll be monitoring the account like a hawk! My employer took away matching from COVID and not sure if we’ll go back any time soon. Stinks, I loved that 4% match : )

Keep us up to date with how it goes, looking forward to it.

-Lanny

Bummed to hear they took out your match at work. I guess it’s better that they play it safe and reserve funds if it means staying in business and keeping everyone employed. Yep, I’ll be watching out for any little gotchya’s along the way with this 401k. From what I can tell all the fees are disclosed and there’s no additional cost for choosing your own funds inside this 401k. Cheers Lanny!