I almost vomited a little in my mouth, but that headline needed to be written.

How many times have you heard that you need $X million in the bank in order to retire safely? Or that you can’t even think about retiring until you’re XX years old?

Now how many times have you then thought about punching yourself in the face because trying to save $X Million is harder than having a civil presidential debate? (Totally random, but did you know that Marco Rubio’s net worth is only $100,000? A chunk of you reading this right now has more than him!)

I came across this TWICE in the past week and it’s quickly becoming one of my biggest irritations. Not because they don’t mean well and aren’t genuinely trying to get people to save more (they are), but because they gloss over the single most important factor in everything.

See if you can spot it…

Example #1) A conversation I had with a long lost friend.

Friend: “Hey Jay, you love money right?”

Me: “Right.”

Friend: “Let me ask you something… HR had me sit down with a financial advisor the other week which was awesome ‘cuz it was free, but within minutes he scared the $hit out of me. He told me in no uncertain terms that I need at least $3.5 Million if I wanted to have any chance at retiring. Is that true?”

Me: “Did he look at your expenses?”

Friend: “No”

Me: “Then how the hell does he know how much you’ll need in retirement?”

(My friend has fully paid off debts, barely spends anything because he’s a homebody, and will have his house completely paid off within 10 years. Sounds like he’s in trouble – watch out!)

Example 2: A PR pitch I just got in my inbox

SUBJECT: The New Retirement Number

EMAIL: Two-million dollars. That’s the minimum amount Generation Y and Millennials will need just to retire comfortably. I thought you might have interest in learning more. Money doesn’t go as far as it used to, and according to financial site [redacted], $2 million isn’t even all that much. Millennial financial experts outline the reasons Why You Will Need $2 Million to Retire and offer ‘how to’ tips and advice. I’m happy to provide the content for your review.

*DELETE*

I took out the blog name because it’s actually a friend of mine and not trying to put him on blast here (something tells me it’s the PR person behind this anyways), but another perfect example of a blanket statement without any reference to the most important piece of the puzzle yet again. Though this time much less scary than the $3.5 figure.

Now I get that this was meant to grab my attention and the actual details could be in the interview or article or whatever else they were hoping I’d do with it (hey – it worked! I’m blogging about it now! :)) but it’s all nonsense at the end of the day and should be dutifully ignored in my humble opinion.

In case you haven’t guessed by now, the most important factor determining your “number” is your SPENDING.

How can anyone tell you you’ll need $2 million or $3.5 Million without having the slightest clue how much your lifestyle costs? Does a person living off $1,000/mo need the same as someone going through $10,000/mo? Do we all have the same hobbies and dreams and future goals in life? Or do we all just suck so bad that we need to hoard as much $$$ as we can ‘cuz we’re all doomed?? (That would be a slightly more reasonable statement based on the way our country’s going, but still no dice…)

Point is – without looking at your *specific* situation it’s all noise and you should DO YOUR BEST TO IGNORE IT. They mean well, but as our mommas like to say- we’re all unique snow flakes.

If you want to figure out what your own number is, do any of the following instead:

- Plug your #’s into a calculator

- Plug your #’s into a spreadsheet

- Multiply your yearly expenses by 25

This will give you a much more accurate – though still rough – look at what you can expect down the line. And THEN you can determine whether you’re happy with it or changes need to be made.

Going back to the $1,000/mo vs $10,000/mo example – you’ll see this becomes the difference between needing $300,000 to retire safely ($1,000 x 12 x 25) vs $3,000,000 ($10,000 x 12 x 25) – based on the generally accepted 4% Trinity Study. Quite a drastic gap if you ask me.

(For further reading on this stuff, check out this awesome article by Rob Berger on how much you need to retire, or the ever feisty Mr. Money Mustache on the same topic.)

At the end of the day it all comes down to your expenses. And without knowing that (hint hint) no one can tell you how much you’ll need to hang up the job when it’s time.

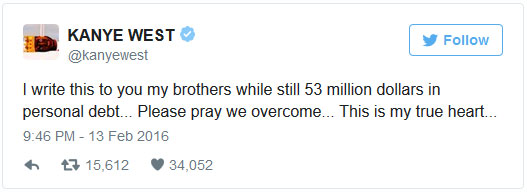

So make that your #1 mission this week if you’ve been putting it off like Kanye and his $53 Million debt woes… Don’t let these forecasts scare you!! Focus on your own specific situation and if it turns out you really DO need $X million to comfortably retire, well, time to decide if you finally need to make a change or not. Just please don’t listen to the hype.

*****

Today’s rant was brought to you by The Federation of Financial Bloggers Against Crimes Towards Money – working hard for you since the invention of the internet.

[Photo credit: Mark Morgan]

Get blog posts automatically emailed to you!

While Kanye is very talented and obviously driven, the fact that he has that much debt makes me filled with glee. I’m trying to be a good person but man, what an idiot.

And the financial adviser probably just makes the assumption that you’ll want to spend what you’re making since that’s the cool thing to do in school now-a-days. :) What a dumb ass!

I guarantee that’s one of the reasons people wait to long to save… hearing large ass numbers like that is scary! You get turned off before you even start :(

The more I think about this, I liken the “one number” to a person’s BMI. From the outside looking in, knowing someone’s net worth is a really quick and dirty way to see how they are doing financially. As a conservative approach, it can work really well. But it’s also a starting point. You should look at NW (or BMI) to say “is there more I need to look into), not the end all be all. It’s a heuristic dammit!

Yup, as others have said he’s either completely dumb or just a gigantic troll

Oh god no, are those number being bandied about again? I remember attending many ‘seminars’ in 2006 (boom time) where the 2 million magic number was mentioned constantly. It’s pretty overwhelming to a young hustler desperate to make bank. Going by your formula we could retire at 600k. Much more manageable.

Also Kanye is a dick.

You almost made me spit out my coffee!! Haha…

An excellent reminder that we should not generalize personal finance. Thanks, J Money!

Might as well just set up a carnival wheel and take her for a spin to see what you lucky retirement number is if you are not going to factor expenses. Everyone got a different situation to often experts are trying to throw out blanket explanation to cover everyone. Sorry my deal is unique.

Yes J$, it’s always about the expense side of the equation when trying to calculate a realistic retirement number. Thanks for sharing the basic calculation with us.

If Marco Rubio’s political aspirations don’t work out, he could always retire on $100k… just not in this country! ;)

Hah!

I had always heard that Rubio’s net worth was actually negative so this is a change in the positive direction!

I hate the idea that there is a general number that everyone needs to hit to be able to retire. All it is is a scare tactic to try and scare the hell out of people and make them doubt they can achieve retirement. Everyone can achieve it and your number doesn’t need to be nearly as daunting as “experts” make it seem.

You’re right that it’s all about the expenses. One thing to keep in mind, though, is that your expenses in your later years may be way different than your expenses now. Mainly in the healthcare arena. Not trying to scare anyone into saving massive numbers, but if you’re not going to have a pretty huge nest egg, then looking into long term care insurance is probably a good idea. The biggest healthcare expense for elderly folks is normally round the clock caregivers or assisted living facilities, which are typically not covered by Medicare. Long term care insurance can help with that. But you have to sign up when you’re younger, so look into it wayyyy in advance (like age 40).

Yes! Great point!!

Yes, I am pretty much aligned with Yetisaurus, very well said. Not everyone has enough saving for their future expenditure. Long term medical care insurance is the key for the salaried people.

Sooner you start it better it would. Very well

I remember going to a financial advisor before I even graduated college and being told that I would need to have roughly $4 Million (preferably in an Edward Jones account) before I would be able to retire comfortably. Now that is a discouraging number for someone who is still working entry level jobs and trying to figure out what to do with their life. Now that I see that its a sales/fear gimmick that financial institutions play and not based on reality in anyway I feel bad for those who live by their advise and haven’t realized the truth yet. I think that they must come up with these numbers based on the worst set of assumptions about the market performance and our spending habits. Let bring back the faith in our generation!

Ugghhh makes me so angry!!

The only good that can come out of it are for those who actually then hustle their asses off and save millions of dollars because of it. Much better to have too much money than too little, but still… That’s a minority out there.

Let me do the math on this one. If you need to net $4 million net from an EDJ account, and we’re going to let compounding work its magic (compounding of fees, that is), you need to put in what, $6.8 million? ;)

Oh my gosh, the Kanye thing- how does anyone rack up $53 million in debt? Unbelievable. I wonder how many diseases could be cured for that amount of money in research dollars.

Awesome point that your true number depends on your spending! Every time I score a “win” on lowering our bills it automatically translates into less money needed to retire! It’s like I’m “saving for retirement” in a whole new way. :-)

YES! When you don’t need as much money to live you don’t need as much money to EARN. Though of course in our stages right now we still want to bring in as much as possible to speed up the process :)

I understand some of that is personal money he put into his business…I have a feeling he probably has a decent amount of debt from “stuff” though.

Oh, Kanye.

In other news, I LOVE the ease in your calculations & the 4% rule. It’s the one single thing that keeps me motivated & knowing that I will be just fine. I can’t believe that for so long I seriously thought I needed millions!

Maybe your old self did because she was a Spender McSpenderton? :)

It’s like you are looking right through the computer screen and into my past Spender McSpenderton soul!!! LOLzzzz….

That & I just listened to what every other uneducated person told me. Ha!

I ran into the same thing with a financial advisor telling me I was going to need 3x what we calculated. Our number was calculated knowing our monthly spend for over a year now, and adding in things that may go up and things that may decrease. Beyond other things, he was so far off about, I can say, I still do not have a financial advisor, nor do I plan on getting one.

Yep, it can be as simple as the calc’s you put out there to get an idea of a good target number. Later on you can tweak it up or down as you know more about your spending.

If you’re a typical American with traditional spending habits, sure, a couple million may be close to your target – especially if your plans include an early exit from the rat race.

But screw that. The last thing I want is to work another 10 years just so I can acquire a bunch more junk that I don’t need. Spending is key, and the math is actually quite simple. The less we spend, the less we need for retirement – and, even more awesome, the *earlier we can retire*.

And who is “Kanye”? :)

The FireCalc site ignores social security. The political reality is that SS is not going away. It may get trimmed back at some point, but we aren’t going to let old people starve on the streets in this country. So save like you won’t have SS, and then it becomes a buffer when you are getting a could of extra thousand a month in retirement that you didn’t plan on.

YUP! Exactly…

Why you’ll also not notice it in any of the early retirement FIRE-type calculators/spreadsheets too :) It’ll all be a plus getting extra $$$ if we’re fortunate enough to do do later!

FireCalc does not ignore Social Security. It just defaults to a social security benefit of $0. If you know your amount, enter it on the “Other Income/Spending” screen. To use FireCalc properly, you need to click on each of the menu items and enter in your assumptions for each.

If you do that, FireCalc is one of the best retirement calculators out there.

I work at saving money but I also know that when I cannot work … what I have is what I have to retire on. When my mother retired she could not believe how little she spent and she really felt she had a great life. She did more traveling than when working. She said that the little cost (car/gas, food, clothing) really add a lot to spending. My brother is saying the same thing…he is actually saving money.

As for Kanye….do not feel sorry for his decisions with his money but thank him for teaching young people a great lesson!

I try not to read finance articles from sites like Yahoo and MSN. They’re so depressing!

I’m so happy that I started tracking my expenses a couple years ago. I know they might go up in the future from what I spend now, but at least I’ll be able to track that trend and hopefully reverse it if at all possible!

People really need to realize that the less they spend, the less they’ll need in retirement.

Strong post J$.

It’s been my experience that financial planners and advisers don’t ever want you to feel like you have enough money because then they can’t sell you commission-based investment products. Asking a financial planner if you have sufficient assets is like asking a beanie baby salesmen if you need more beanie babies.

Connor

Oh hot damn I have to go tweet that out now, haha… brilliant!

Yup J its true, it is not what you make but what you spend. Retirement is only a priority when you make it a priority. As of today I think ill be good with less than a million to retire, but that darn inflation better not mess up my plans. Haha. 53 million why the heck would he put that on twitter, sympathy never pays off debt. I guess he can go the 50 cent route, bankruptcy.

I (we) just recently figured this out too. $2+ million sounded like mission impossible especially now that we are officially in our 40’s and are just getting serious about this (after paying off student loans and preK for both of our kids). I didn’t understand where this magic number was coming from, and figured out we should just crunch the numbers ourselves. I was pleasantly surprised that we would need a little more than million based on our lifestyles, and if we paid off our house before retiring. We are aiming for age 55 not 67 for financial freedom too (another term for retirement since I don’t think I would ever fully retire).

I’m glad you wrote this post as folks need to realize that everyone has their own magic number, and that it does not take a financial planner with some crazy formula to figure out what that number is.

I like “financial freedom” too :) Anytime I call it “early retirement” I immediately get bombarded by statements like “what if I like my job?” “I don’t want to sit around and do nothing all day?” etc etc… Freedom is perfect because you have the freedom to do whatever the hell you want at that point! Work or not work or sit on a couch and count to a million by yourself – you’re da boss – hah.

OMG, Rick and I were JUST talking about this. He’s got a co-worker who wants to work for another two years (he’s 62) because he can’t afford to retire. Rick said, “Yes you can. It’s called budgeting and making value-based spending choices.” “But I don’t want to” says the guy, “I want to be able to buy whatever we want”. Well, then, I guess you can’t retire – EVER!

Haha…. at least he’s honest with himself :)

Put me in the 33x or more camp. If I was burned out, I would be OK with 25x and would have walked away yesterday. Most days, I enjoy my job, although I can admit I enjoy days off even more. When I hit 33x, I’ll probably march towards 50x. Eventually, I expect to reach the point where I’m equally or more likely to regret retiring too late versus “too soon”. I hope I’ll be able to recognize that convergence point when I get there. I’m glad to have this site and other great blogs to help sort it all out.

33X or more is fine – it’s still tied to your spending/goals vs randomness!

Karma Kanye, karma… I get those SHOCKING HEADLINES all the time in my inbox and see it on the webz. I think like most media they use scare tactics as click bait. Still, makes for good blog ideas. But you’re totally right about how it comes down to lifestyle. Or at least that’s a huge part of it! Pretty sure “KimYe” could’t live off even 2 or 3 million.

The saddest thing about those inflated numbers is that some people (like “old” me) see them, freak out about them, don’t bother saving, and give up on ever retiring. It never occurred to me that even though we have made some mistakes, we already live a fairly simple life and there’s no reason that we wouldn’t do the same after we retire – duh! Wish I had figured that out a few years ago…live and learn.

EXACTLY!!! It’s meant to help but all it does is scare you the F off and it’s like you might as well never even try, sigh…

That’s so ridiculous and annoying that… gah! I have no idea how much we’ll need in retirement until a few things shake down, but I sure as hell know it’s not $3.5M. Which is good because there’s no reaching that number! A million would still be unattainable given our limitations.

I don’t know why a financial advisor would go around scaring people like that. Is he trying to ensure business? Since the guy’s employer hired him, are they just trying to discourage people from ever retiring? If so, I bet it worked!

I only need $550,000 according to 25 times expenses.

But what about the cost of healthcare/ assisted living / maybe cancer and the rate of inflation and the tax rate? I think with all of those considerations I would need more than a million dollars to retire even though I can live off of $4000 a month with all my bills.

The 25x is just a great starting point to give you a better idea than a random number thrown out there. Some people pad it to account for what may come down the road, while others lessen it for their own personal reasons. The only time we’ll know for certain is when we’re older and retired and living off it :)

EXACTLY. You take SENSE. I Like that! c

It is kinda crazy that Marco Rubio only has a ~$100,000 net worth. I’ve got a follow up post about that where if Marco can make it big, so can any of us as a result.

I agree w/ you on the spending portion of things. There is no one size fits all, but there are some suggest net worth targets by income multiples on should shoot for. My personal recommendation is 20X your average income for the past three years. Let’s rock!

Sam

Wait just a darned minute, Financial Samurai! I thought we were using spending as the variable, not income. You just quintupled my target with your new equation. I think I’ll go ahead and stick with J.$’s math. [no offense]

Retirement number based on expenses is a great start but I would to add a few factors- just to be safe because life changes all the time:

– the bare minimum retirement fund is based on how much you spend

– plus add a contingency pot based on a percentage you are comfortable with for unknown events that may happen or buy expensive insurance for peace of mind

– then add a padding factor for unfortunate but possible events ex: kids come back home and live with you because health issues, parents need a lot of medical support, spouse gets really sick)

– consider adding a bit of padding for lifestyle changes (more time available to travel right)?

I don’t mean to scare anyone, It is more of a reality check, if the number is too high, consider part time hustles that are fun and can generate income to supplement in time of need, It is based on your comfort level and personally I’m ultra conservative, life changes all the time!

I think it would be so much fun to be an airbnb host when I get older so I meet lots of new people! I remembered meeting an older couple who does that and they are both retired. I thought what an awesome idea and they really enjoy it.

–

All good ideas for sure

No worries! Use whatever math you’d like, as you know your finances the best.

My 20X multiple is an easy number to remember, and based off various variables, including retiring by 60, dying 20 years after retirement, and trying to leave some money to others once dead.

Great marketing action. They scare the hell out of people and then can come with the solution…. Good stuff…!

This is where you split the good from the bad. The bad take a general one size fits all number. The good make your personal finance…personal!

These blank statements really get me fired up whenever I hear them. So many of these “financial advisors” fail to mention that how much you need to retire is totally based on your expenses.

I’ve been thinking a lot about this recently and have concluded that it’s not about how much you make….it’s really more so all about how much you need! Good post!

“$X million is required to retire comfortably” makes no more sense than “you must spend X months of salary on an engagement ring”. It’s silly without looking at what you actually want, what that will cost, and how much you need to save to provide that income with a comfortable level of risk for the individual.

I say we’re retired on $1.x million and plenty of people say “holy shit Justin, that’s [a lot / not enough!]”. A million bucks is way more than some people will need, whereas if you have a family of 5 like us you need that much or more unless you are very creative and live non-traditionally (or have other income sources).

Bottom line, it’s a huge fallacy to say a particular number fits everyone.

I think the biggest retirement expense for us will be medical insurance. It’s been running about $600 – $1000 per person for my friends who have retired. We spend about $2000/ month on living expenses so about 1/2 of our retirement budget, $2000/month will go to medical insurance. So remember to add in medical insurance into your retirement spending plan and remember it gets more expensive as you get older. Also make sure you have sufficient funds to meet your deductible. Our deductible with my husband’s insurance is $5,000 per person for in plan providers and $10,000 per person for out of plan providers. This is important to remember because if you go to the hospital, even though the hospital and your doctor are in plan, other in hospital providers may be out of plan and you will get charged for their services.

Yup, good things to consider for sure… who knows how much MORE it’ll all cost later too, ugh…. We pay $1,000/mo right now for our family! Just for the premium!

I like reading different perspective on retirement, especially those with numbers, but I definitely take it all with a grain of salt. I concentrate most on our personal situation – because that’s what matters. We can’t fully retire early, because of our debt situation. But I know that we can semi-retire early if we keep working hard. That conclusion is based on projections that include investments, part-time work, and rental property income. If I blindly accepted the opinions of others on what we needed to retire, I wouldn’t even dream of being able to leave the 9-5 for decades.

Rental properties help a lot. I think they are a way to get inflation indexed income. Also if you become unable to work due to health issues you can hire people to take care/ manage them. It seems many working class people in our neighborhood become ill or their bodies wear out leaving them unable to work when they get in their 50s. I think everyone should work towards being able to retire “early” so that’s it’s a choice/option if you’re still able to work and want to when you’re in your 50’s.

Just started following your blog and love your views.

I have to agree that every situation is different. And this is a good reminder of that.

I plan on passively working until the bitter end. You never know what the future has in store for you until you get there.

Glad you’re enjoying the site :) Thanks for chiming in.

I had my planner tell me that too. I asked: “How could I need 3 million if I’m not earning it over my lifetime?” They said that’s just what they are telling everyone now. Nice! So nothing to do with personal situation just a number meant to scare some into saving.

You hit the nail on the head J $ it’s all about your expenses and lifestyle. Get those under control and your retirement number will drop.

Haha, yeah… hard to save something you don’t even make OVER YOUR ENTIRE LIFE. Speaking of which, did you know you could check out what that number is by going to the social security site?

https://ssa.gov/myaccount/

It’s great that you countered to your friend, “did he look at your expenses?”. Financial planning 101!!! How redic that he was getting advice based on zero data.

I mean, of course a financial advisor would use scare tactics to try and get someone to invest more (and probably take more risks than are necessary). The other factor of course is most financial advisors are probably not going to assume their clients are frugal, because most people aren’t. But for a finance advisor to throw out a number like that without even asking about spending habits is ridiculous and shady as hell.

One thing I don’t get about people referencing the Trinity Study/4% rule is that some use the resulting figure as an early retirement number. The study gives the 4% withdrawal rate as a target for having your money last longer than you will based upon a normal retirement age, not an early one, no?

My understanding of it is that it helps conserve your pot so wouldn’t matter when you start pulling from it (if you’re only taking out 4% but it’s averaging 8%, you’re good and/or breaking even w/ inflation/etc). But I’m far from being an expert here so hopefully others chime in!

Running the numbers my wife and i need less than 600k which is what some spend in a year. Others I know would need many times that. It’s all in what you spend.

Great post! I love that your message is empowering – control your spending, and control your financial destiny.

I do my best to ignore all Kardashian/Kanye headlines and stories, because – quite honestly – they make me sick. But I’m having a really hard time not reading about Kanye’s debt…

I think I may have found my magic number!

There he is! Hope you’re doing well over there, good sir. Miss you popping up here and there :)

I almost pissed in my pants, laughing, while you were vomiting in you mouth. It’s so lame to put a blanketed large retirement number on someone without actually understanding their debt/income and monthly expenses. On the other hand, I don’t think it’s as easy as taking monthly expenses times 12, then times XXX years.

20 years ago retirees never foretasted for monthly cell phone and internet bills, or new phones and computers every few years. My point is I agree with your method more than a blanket number, but the true number lies somewhere in between.

30 years from now we will all have unforeseen expenses that we didn’t forecast for. Hopefully it’s for something cool like monthly service fee for an 18-year-old libido or renting an new, younger organ.

Hah! Could be right on that, for sure… I guess at that point though you weigh the pros and cons and whether you need to start hustling on the side or can go w/out the libido ;) Always a trade off of wants vs needs, eh?

I think it kind of depends and quite a few different variables:

How far will today’s pre-tax dollars get you in 40 years?

How much will you spend post-retirement?

Will you accrue any debt post-retirement?

How much social security will you be receiving?

How much in pension payments will you receive? (if you’re that lucky…)

How much will you be receiving (or needing to receive) from your 401k and other investments?

I agree with Investment Hunting above. I recently sat down with a financial adviser and we plugged in all of my expenses, income, debt, etc. In the end, the goal is to live below our means, discontinue our “war with the Jones’s”, and invest/save as much as we can so as to live a comfortable life after retirement.

I don’t think there’s a specific number. We could create specific goals for ourselves, but it’s hard to plug in a number and say “oh yah, I’ll be totally cool with 2.1 million in the bank when I’m ready for retirement, and that’s all I’m going to save for.” Good luck….

For sure… Def. more to it but the spending multiplier is a better head start than a number pulled out of thin air :) And personally I’m not even *considering* social security or anything else so all that would be a major plus if it comes through when it’s time! As well as other more positive changes as inheritances, lottery winnings (hah) etc… Granted better to play it safe than sorry with future changes, but at least there’s some positive ones that can occur too.

Agreed that your spending is the most important variable to consider. But most people don’t bother keeping a monthly budget, so they have little idea what their spending actually is, or what areas they could trim. If throwing out $X million or some other figure nudges people into saving more for retirement, then maybe it’s for the good.

How unfortunately true that is :(

I completely agree! I definitely want a nice retirement complete with lots of travel, so I will need a bit more, but each person’s retirement account is going to be drastically different. In addition to spending though, expected health care costs also are a concern. (I’m perfectly healthy, but you never know what might happen during those last 10-20 years.)

If current expenses include young kids and a mortgage and when we retire we hope to had older kids and no mortgage, what do you use for numbers? Will our mortgage money be medical expenses and our kid spending, vacation spending?

I think you just have to do your best to gauge and continually tweak it all the way up to the magical day :) That’s the beauty of tracking all this stuff early too – you’ll always have a real-life snapshot of the situation as it stands today, and then it’s up to you if you want to fast track it or change courses to meet whatever current/future goals you’re looking to achieve. No one else is going to care about our $$ as much as we are!

So, so true. It’s not just about your spending, one needs to consider other things too. For instance I’m Canadian so I will never have to worry about things like major medical emergencies, an unfortunate expense most Americans will have to prepare for. It is such a personal number there is no one-size-fits-all model.

Retirement numbers are not, as you point out, one size fits all. This “magic number” idiocy puts people into an unnecessary state of panic and anxiety- when if they did the simple math (thanks for your calculator!), they would find that more may be in their control than they realize.

Some of this panic is actually fueled by the investment PR machine. Fear is the most powerful advertising motivator so a good scare may get you to contribute more to your 401K. Not a bad thing as long as your debts are paid off and you’re investing wisely. But I’m not down with the fear thing.

Yeah, I wouldn’t mind it as much if it did get people to actually save more but we all know it has the opposite effect :(

“Focus on your own specific situation and if it turns out you really DO need $X million to comfortably retire, well, time to decide if you finally need to make a change or not.”

One change you CAN make (and we hate to consider THIS one), is that the change you have to make might just be to change your plans so that you spend less.

We HATE hearing THAT one–but it’s often your only choice.

Yup! Big gains usually require big changes!

I think for most people, INCOME also should be a very significant factor in calculating their “number”.

A retired couple who spends $40K a year would need $1 million using the 4% rule.

The same retired couple with $24K in social security benefits and a $12K a year pension would only need enough retirement savings to cover the $4K a year shortfall. For them, $100K would do nicely.

Yup, lots of pieces to consider for sure.

A big part of expenses project during retirement as well should take the geographic locale and cost of living and bring it into play as well. It’s always fun to have these conversations with friends, by asking what’s your walk away from everything number? i.e what is needed to retire, and he came back with a ridiculously lower number than i thought he would say.

However, his game plan include moving out of the U.S to a country with a much lower cost of living and take over a property his family owned and live the simple life. So would definitely agree j, that the numbers that are thrown out are just that numbers until as many realistic factors as able are considered

My favorite is when financial experts tell people “all you have to do” is move somewhere cheap and then all your problems will be solved. As if it’s easy (or worth it!) to leave all your friends and family just to save money. I’m always tempted to ask why they haven’t moved in that case then? ;)

I have come to the realisation that every big financial goal number should have a logic behind it. As Simon Sinek says – “Start with why” and it works on almost everything. If someone tells you, you need $2 million to retire, ask that person why? To me, visualising how you would want your retirement years to be spent also helps. If you see it as being a quiet period of spending quality time with family, sure you don’t need much. If however, your plan is to visit almost every place on earth for which you didn’t have the time or the money and are willing to sacrifice present for that promise of a dream future, then again you should calculate the retirement corpus that you need. All in all, “to each his/her own” is a fitting statement even for something as fundamental as a retirement number.

Yup yup… Reminds me of Toyota founder’s famous “5 Whys” when you’re trying to figure something out – https://www.tillerhq.com/blog/2017/6/4/what-the-five-whys-teach-us-about-our-spending

This sounds a lot like a conversation I had with my former financial planner who was trying to get me to up my insurance coverage. I’m not a believer in whole life, but I do have a 20-year term policy as a safety net for my wife and kids should I meet an unexpected and early demise. When I told my adviser how much coverage I wanted, he told me that wasn’t enough. He said he recommends to all his clients that they have at least a $1 million policy. He said this before ever looking at my outstanding debts or current expenses. Once I showed him everything, he stopped with the high-pressure sale, but still said he thought my coverage was a little tight. I told him I wanted to be worth more alive than dead. I didn’t want anyone getting any crazy ideas!

I’m gonna have to steal that sometime – “I told him I wanted to be worth more alive than dead.” :)