In case you weren’t aware, this week is the 2nd National my Social Security Week. An event so glorious to money nerds that I can’t believe I almost missed it! ;)

I got an email saying to pass it along to all my colleagues, friends and family, so here you are:

July 19th through 25th marks the celebration of our second National my Social Security Week. Since you have an account, you are aware of what a great financial planning and benefit management tool it is! We hope that you take this opportunity to spread the word to your colleagues, friends and family, about the benefits of signing up for a my Social Security account at www.socialsecurity.gov/myaccount. Let them know that with their account, they can verify their earnings and get estimates of their future benefits to help them make important financial decisions. If they are already receiving benefits, they can get a benefit verification letter, check benefit and payment information, change their address or direct deposit information, and get a replacement Medicare card or SSA-1099 for tax season.

A my Social Security account is convenient, secure, and FREE! It’s never too early or too late to plan for retirement.

They got that last part right! And in all seriousness, it actually is a pretty bad ass site. You can literally log in anytime to see what you (may or may not) get when you retire, along with your entire reported income history. Anyone who gets off on numbers will love this.

Here’s what it says I’ll receive when I retire:

Now I don’t count on any of it just in case, but if God willing I have an extra $2,000+ coming in every month until I die, I will be one pleased budgeter. That’s like having an extra $600,000 invested if you’re going by the “4% Trinity Rule!” Amazing! And according to my early retirement spreadsheet, that would also mean I could retire 8 years earlier at 40 instead of 48 right now :) If, of course, you could actually get this $$ in your 40s (you can’t) and if it’s still there for us come another 30 years (I couldn’t tell you one way or the other).

Anyways, pretty fun stuff to see. Definitely create an account and poke around if you haven’t yet.

While I was in there, I also checked to see if 2014’s numbers were included in the “earned income” section as the last time I checked it wasn’t. Something I’ve been dying to see so I can update our LWF! (Lifetime Wealth Ratio™). And it was!

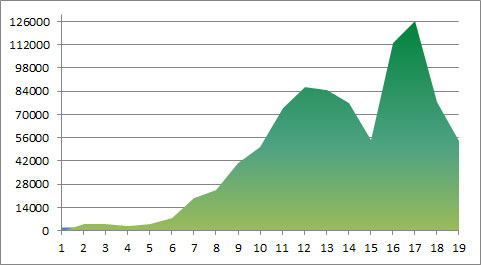

Here’s what is shows for all my earned (taxable) income since birth. With emphasis on taxable.

And here’s what it looks like visually since it’s much more fun to see with graphs (hint, hint, S.S.):

Pretty awesome and scary at the same time, eh? This spans 19 years of money making in high school, college, early career, and most recently, the last 4-5 years of self-employment. Which as you can see has fluctuated wildly! (But don’t worry, 2015 is shaping up to beat out year 17 :))

Back to the LWR…

Once you have your hands on this great info along with your net worth numbers (which any good reader here should have by now, right??) you can then run some pretty fantastic ratios like the one I made up last year: The Lifetime Wealth Ratio™. Which is simply:

Net Worth ÷ Total Income Earned

A not so scientific, but VERY telling, idea idea of how you’ve managed your money over the years. Also once featured in a New York Times piece so you know it’s good ;) The higher the ratio, the better you’ve been saving/investing/building wealth.

Here’s what mine now clocks in at: 54% ($489,886.10/$906,310). Which puts me in “Marry Me” status per our measurement key:

- 0%-10% – Meh

- 10%-25% – Now we’re cooking!

- 25-50% – You’re on fire, baby! Give me your number!

- 50-100% – Marry me.

- 100%-1,000% – How do I get into your will?

If you’re bored/awesome/sexy, I encourage you to run your own numbers now too. Unfortunately I dropped a percentage point from the last time I ran the numbers (November of last year), but it’s always good to see where you stand regardless. Feel free to make up your own measurement keys if mine aren’t satisfactory :)

Here’s to being nerds!

Get blog posts automatically emailed to you!

…but if you make more than the earned income threshold, the numbers won’t be accurate. Ss cuts your income off at a certain number if you make more than that amount. I don’t remember what the threshold is but it is in the low 100ks

So the goal should be to Rothify your nest egg by the time you are 62, and then live off Social Security Tax free…

Actually, if your “earned income” is under certain thresholds, the government gives you money to save in a 401 (k)/IRA… Win-Win-Win

I freakin’ love all the places to hide your money from taxes :) You’d be crazy not to take full advantage!

Where do all homeless accountants live.

In a tax shelter ;-)

WOW! I ran the calculations and my LWR clocks in at 162%!!! I must be a an absolute hottie! Applications to be included in my will are available at http://www.SellMeTheBrooklynBidge.com

Well, when you use a corporate structure and divide your pay between salary & distributions or have a lot of rental income, etc. you have to do a lot more calculating and dig out years of historic tax returns to get the real picture. It’s a pretty cool ratio, however.

Can you start an LLC and give yourself (or partner or whoever) a small, reasonable salary (30k)? Then any additional profits wouldn’t have to be taxed on SS which is a HEAP. Obviously you should talk to a tax professional but I know someone who did this and they saved a TON of money on their business!

@Chris

Yes. The profits “pass through the partners (or sole partner). That’s the way most do it.

I use a S-Corp and it works the same way. Take a reasonable salary or wage for the services you perform and the distribute the rest as profits. No SS tax on distributions, thus the beauty of the arrangement.

Curtis….do you have trouble borrowing money or financing the rentals with the S-Corp? In another life I was a RE agent and dealt with a lot of investors. I seem to remember having a heck of a time getting financing when a S-Corp was involved. Is that still the case?

@jestjack

Sorry for any confusion. I operated my commercial cleaning business http://www.A-1Janitorial.com as an S-Corp.

My rentals are all titled in my and my wife’s names. We’ve never felt the need to run them under an LLC or Corp but we do purchase an umbrella liability policy for extra asset protection.

As to financing, we currently have 200k signature loan through one of our banks. They are lienholders and will attach the houses individually as the borrowed balance reaching the limits of the liens.. For example, if I borrow up to 30k, they automatically attach the loan to house #1. If I borrow say 80k, they now attach the next house and so on. Up to 5 houses and 200k. Since they’re paid off and there are no other mortgage lien holders the bank is comfortable and likes this arrangement. It’s not a HELOC that can just be shut down as happened to some, but an investment account. I send an email and the money is transferred within a few hours. I currently carry no balance and can pay off the balance at any time with no penalty. The current rate is 5.5% Give me tremendous power to take advantage of opportunities in a flash. I’ve tested it out but won’t do anything serious with it until my last rental is paid off in about 9 months. Then it’s clear sailing.

I know that was long-winded, but there are options out there when you find a banker that gets to know you and respects your fiscally responsible history.

Hope that helps.

So incredibly interesting!!! Late to the strand here, but thanks for putting it all out there for us. I’m always hearing about S Corps but never really dug into yet. Y’all are making me want to :)

The worst part for me is that I can never remember my damn password and end up getting locked out. IF THEY SAID THAT YOU CAN ONLY TRY THREE TIMES I WOULDN’T HAVE GUESSED AGAIN ON THAT THIRD TIME.

Well, I’ll have to try again tomorrow morning since I’ve reset my PW again. :) Damnit, this is always a fun one to look at.

Haha… I think you would have gotten it on your 4th attempt, if you ask me :)

First time commenting, just under three years ago I had almost nothing to my name. In that short time I have raised my net worth to 50% of my lifetime earnings! Thank you for this great blog.

There you go! Sexiest thing I’ve read all day :) Thanks for reading and chiming in – really appreciate it.

Separate note, if I retire by 40 like I want to, that would definitely change how much I’d get from SS, and I’m OK with that! If I’m getting 1k a month when my house is already paid off, that would absolutely cover my personal expenses!

Yes that is one bad @ss ratio to calculate. I logged in and signed up on that website already a few months ago. My wealth ratio I cant fully recall, so I need to calculate it again. ITs not as high as yours J., so I need to find me a job that matches 100% 401K contributions like your old 9-5. That or save like crazy to catch up. Thanks.

That definitely helped, I’m not going to lie :) And 95% of my colleagues didn’t even take advantage!!

Ha! I think that is one fine measurement key :) We are just cooking but we have been ramping up our efforts! Hopefully, we will catch up and make it to Marry Me status one day!

Very interesting. I’m headed over there now to find out my numbers. :)

It was really cool to see how much I’ve made in my lifetime, sadly I’ve made less in my lifetime than I currently owe in student loans (don’t go to law school kids), but that revelation actually makes me proud of what I’ve accomplished in paying off debt, even though I’ve been seriously broke, I’ve still managed to pay off my credit card debt and have built some good financial habits, just have to keep going to get rid of the rest of my debt. In other news, I’m below the “Meh” category, which is why I got a cat. lol.

Hah! And hopefully you have a law degree now which means you’re 10x smarter than myself :) I never feel like a degree is a waste of money even though it sucks debt-wise for a bit. Can never beat investing in yourself/future.

PAR-TAY! :) Just kidding! I had no idea it would provide that much info so when I get some time (I’m sorry, what is this time thing you are referring to?) I’ll have to check out my own numbers.

I didn’t know that existed. Pretty interesting.

Only 34 credits so not sure what my “future” benefit would be…

Nevertheless I will take 54% LWR!

You’re beating me!

Man ive been being told my whole life by random people that we are not going to get any SS when I reach the age so there is just no point in getting my hopes up. Would be pretty cool though.

Something like social security will be around by the time millennials retire. There just has to be something.

Yeah, I think they’ll be something too even if it looks way different. Won’t stop me from building up my own nest egg regardless though – you can only count on yourself 100%!

I definitely think that Social Security is here to stay with a big but. I think that due to gen X being smaller than the Boomer generation and Gen Z likely to be smaller than Y that the politicians will figure out some sort of reverse disbursement plan. Like rather than getting social security, you will get tax credits. Also, social security will undoubtedly change to a general budget item- Hopefully in the next three years, when it will effectively become a budget item due to the income generation being lower than the expenditures.

Anyways, you’re not allowed in my will just yet :)

I’m going to email you every single day until you say yes :)

Time to drop some SS knowledge…There are some hefty assumptions being used in calculating your SS benefit. The big one being that you will continue to earn what you did last year until you start collecting benefits. The lessor assumption being a guesstimate on what inflation will be.

The way SS benefits are calculated is by taking your 35 highest earning years when adjusted for inflation, and using that average to calculate your benefit. That benefit is a percentage of income based on what they call “bend points.” Facinating, isn’t it?

This is important to know because if you retire at age 40, then all those years leading up to 35 years of work add in zeros to your average. How specifically do you calculate the benefit? It’s really hard. Rule of thumb wise? Take the projected benefit and mark it down by the percentage of 35 years you plan on working…then knock off another 25% for SS “issues.” Some people think that it’s the last years that calculate into the benefit…nope…this isn’t a pension. This system also works to the advantage of someone that works longer than 35 years. For instance, right now, that $350 is counting as one of your top 35 years. Work a 36th year, and that year will come off the books and increase your average.

Oooooh definitely fascinating!!! And HUGE benefit to working those extra years then in that case and watching that $$$ go up! I always wondered why they jumped so much like that… Of course, a couple more years of work in your 60s vs 30s are a completely different story. I don’t fault anyone for wanting to be done earlier and get that time vs $!

You’re going to marry yourself?

Ok, here is where I’m at, I’m always a bit cautious because I can calculat this a few ways, here are the definitions of my calcuations:

Total Cash Only (net worth minus any physical assets e.g. home)

Total Cash + Home Equity (net worth)

Total Cash + Home Value (total assets)

From those 3 categories: and using Taxed Medicare Earnings (the bigger number on SSA.gov) I am:

30% (Cash only) or (Total Cash Saved / Taxed Medicare Earnings): e.g. 25-50% – You’re on fire, baby! Give me your number!

41% (Total Cash + Home Equity) or (Net Worth / Taxed Medicare Earnings): e.g. 25-50% – You’re on fire, baby! Give me your number!

51% (Total Assets) or Home Value + Cash + Checking + Investments): e.g. 50-100% – Marry me.

Seems, I need to stop earning money to push it past 51%!! Just so everyone knows; I calculate the lowest possible number as my guidline: so, my honest number is 30% cash only, I only calculate invested and liquid cash. Frist Goal = accredited investor (must have a net worth of at least one million US dollars, not including the value of their primary residence ….) there is more to the definition, but this is my first target.

Back to your regularly scheduled program.

NWOutlier

That’s a helluva first target :) I’m just trying to hit $1 Mil with all my assets and that’s hard!

Hey, 54% is pretty darn good. I have to sit down and calculate my ratio.

I haven’t been able to log in to the site the last few times I tried. It seems like they want me to log in during working hours? Why can’t I run my numbers at midnight, the only time I have…

I’ll try again and see if I can get the number. I’m looking forward to an extra $2,000/month when I’m 67 too. :)

I can’t imagine the system being closed during certain hours like that? It’s the internet! Your user or password has to be wrong or something.

OK, I got my password reset. Wow, I made a lot more money over 21 years of working. My ratio is about 50%.

This is a very cool ratio! I’m going to calculate it ASAP when I can get my hubby’s SSI figures too. It won’t mean as much to me though since I have received financial windfalls from family over the years which compound and accelerate my net worth growth.

I would say that’s a good problem to have :) And at least you didn’t spend it all and it’s being invested! That counts pretty damn high towards your financial smarts!

Damn, almost marital material.

48.6% of my $1,159,739 in Social Security reported earnings is reflected in my net worth.

I had no idea my lifetime earnings was over a mil!

Pretty cool!

After years of blowing through money like Hammer, and finally getting it together the past 7 years, I’m at 25%. Feeling good, actually, thanks for posting this up.

But I need to add another $100k of NON-Taxable income to my number for accurate lifetime earnings…. ;)

Hey – you’re up from 9% last year when I tried to figure yours out! Haha…

https://budgetsaresexy.com/2014/11/total-lifetime-earnings-wealth-ratio/

You were my first test case when building this ratio :)

I come in just over 50%

I’ve understood and liked the concept for awhile now (since reading Your Money or Your Life), but never heard the LWR term. I like it!

http://wealthydoc.com/blog/what-do-you-have-to-show-for-all-you-earned

Rock on!