Happy Monday! Who’s ready for kick-ass week? 🙋🏼♀️🙋🏽🙋♂️

I’ve been reading a survey conducted by our friends over at Personal Capital that reveals some interesting info about how covid has affected people’s retirement plans.

Some of the results are a little scary (like ~30% of people tapped into their IRAs and 401(k)s to fund living expenses last year), but most stats seem apt given that 2020 threw everyone for a loop. I’ll list and discuss the main takeaways below, and if you want to check out the entire dataset, you can do so here.

Also keep in mind that statistics can be interpreted many ways. So take everything with a grain of salt!

Quick Stats About the Survey Participants

This data was collected Nov. 4 to Nov. 10 — right after election day. All respondents were Americans with at least $50k in retirement assets and were “not retired yet.”

Respondents were between 40 to 74 years old, with the biggest concentration (32%) in the 40 to 44 range. They were split equally by gender. Most (86%) were employed (full-time, part-time or self-employed). Seventy-six percent were married.

Enough of that! Here are the interesting finds …

About One-Third of Americans Withdrew Money From an IRA or 401(k)

Part of the CARES Act let people affected by the coronavirus take a distribution of up to $100k from their IRA, 401(k), or similar account without paying the regular penalty.

Looks like about 1/3rd of people withdrew from their retirement accounts, and not just small amounts … more than 30% of them pulled out $75k – $100k. Most funds went to pay regular living expenses. 😳

Regarding the people who “took a loan”… Sometimes taking a *short-term* loan from your retirement account isn’t actually such a bad thing. It’s a tax-free loan, quick process, has no impact on your credit report, and you pay yourself the interest vs. borrowing elsewhere. As long as you pay back the loan within the right time frame, it can be a good fix to a short-term problem.

That being said, I think we can all agree that having an emergency fund is the best way to cover emergencies. This is one of the main survey takeaways I’ll get to at the end.

How Saving Rates Changed During the Pandemic

The median savings in 2020 was 12% of income for all respondents. Data showed about 66% of people contributed to their workplace retirement accounts, 37% to a traditional IRA, and 29% to a Roth IRA.

Honestly, this isn’t as bad as I was picturing. And another interesting thing is that almost 80% of people saved the same or more in 2020 compared with what they saved pre-pandemic.

- 53% said there was no change in savings rate pre-pandemic

- 25% said they saved MORE in 2020 than before

- 21% said they saved less than before

- 1% weren’t sure 🤷🏻♀️

How the Pandemic Is Changing People’s Plans for Retirement

This one is really interesting…

Thirty-four percent of respondents said their retirement plans haven’t changed, and the other 66% of people are mostly planning to work longer and/or save more money.

But, why I find this interesting is because in the section above, nearly 80% of people said they saved the same amount or more than pre-pandemic. This tells me that the pandemic itself didn’t harm their ability to save in 2020, it was more of a wake-up call alerting them to the fact they may not have been saving enough in the first place.

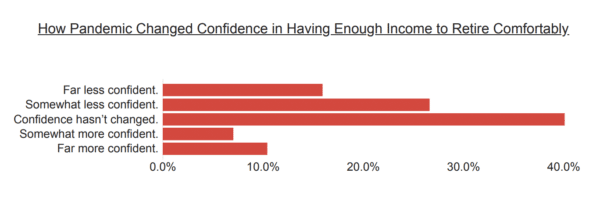

Confidence About Retirement Is Taking a Hit

About 43% of people said they are less confident that they’ll have enough to retire comfortably as a result of the pandemic.

But, although confidence was shaken, still 7 in 10 (71%) respondents said they were confident they’ll have enough income to live comfortably in retirement.

Social Security is a big part of this expected future income. In fact, 1 in 5 people said they expect Social Security will cover >50% of their needed retirement income. 😰

How Americans Are Investing Now — Includes 24% Cash!

Here’s the breakdown of assets in the respondents’ investment portfolios as of November 2020:

I thought I was nuts holding ~10% of my net worth in cash, but these respondents have a huge collective cash allocation at 24%! (They are older than me, so having a less aggressive allocation makes sense I guess). I’m kind of surprised there’s not a larger stock allocation — just 36% here.

How Americans Reacted to the Market Downturn in 2020:

I’m most proud of the 54% of people who said they did nothing about the stock market and simply waited for it to recover …

This is waaaay easier said than done. When markets drop and everything turns red, it takes a really strong mind-set to think long term and not do any panic selling.

Personally, I sold $40k worth of stocks in a panic in March (mostly to boost my cash position and add to my real estate emergency fund) but ended up re-purchasing those same $40k of stocks about 10 days later. Thankfully, the market declined during that 10-day period, but it could have easily gone the other way.

Two percent of people said they withdrew from the stock market completely and haven’t re-invested any money since. 😪

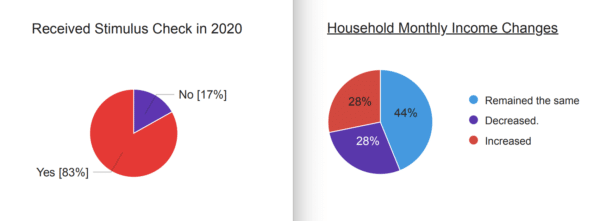

Who Got a Stimulus Check? (and Did They Even Need It?)

This is a little disheartening … 83% of survey respondents received a stimulus check. But only 28% percent of them actually stated that their income decreased…

I think it’s safe to say that a lot of money got sent to people who didn’t really need it (myself included). That’s probably why most people collectively said they saved it, invested it, or gave it to charity.

Keep in mind, this survey was done in November. Income situations may have changed since then (many cities went into more lockdowns for holidays), and another round of stimulus checks went out in late December and January.

What Americans Predict About Economic Recovery

The majority (72%) of respondents are confident the economy will improve in 2021. But 3 out 4 (74%) are still “worried” about stock market volatility.

It’s difficult to interpret this because the questions are quite broad. But I think in general, most people expect 2021 to be much better than 2020 as far as economic improvement. However, they seem very aware that the stock market is detached from the underlying economy and has a mind of its own. (Could also explain why many people are hoarding cash?)

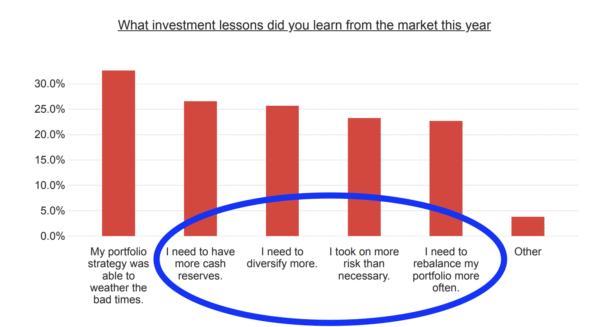

What Investors Learned in 2020

The biggest realization for everyone was that their portfolio strategy was able to weather bad times. Good to know when the next “bad time” comes!

We all need reminders of the other lessons learned, too:

- Check your cash reserves and emergency fund from time to time. Adjust it accordingly when your life situation changes.

- Check your diversification and asset allocation. Diversifying reduces risk by spreading your eggs across multiple baskets.

- Rebalance occasionally as your goals and risk tolerance shifts over time.

- Don’t take on more risk than necessary!

There’s a bunch more facts and general poll data here and here if you’re interested.

******

So, what do you reckon? Do these survey findings align with your experience last year? Have your retirement plans changed? What about you FIRE folks?

Have a great week!

– Joel

PS: Cheers to Personal Capital and to Kiplinger for conducting the survey and giving us permission to use the data and graph images. Personal Capital is a paid affiliate partner of ours, but there are no affiliate links in this post, nor did we get paid to write this.

Get blog posts automatically emailed to you!

Happy Monday Joel –

Thanks for sharing your thoughts here on this survey! I was actually pretty surprised to see the savings rate in 2020 stay relatively the same. I’ve noticed this too, from my conversations with millennials all the way to the age group that was interviewed – the majority stated that they saved the same as they did in 2019, if not more (lots of savings in the eating out and travel categories). I was really happy to see such a high percentage of survey respondents to be so confident in the economy!

Thanks so much for sharing these insights, and have a great week!

Cheers,

Fiona

I feel like there are many people thriving, and many people hurting. The “K shape recovery” is a good way to describe it.

Happy Monday Fiona, have a great week my friend. :)

Great article! I really enjoyed the graphs and access to the data sets.

I took the first stimulus check and split it between by three adult children. They are their partners had different degrees of job instability during this time. Since I could not go anywhere and going out to eat and listen to music is the main thing I do, I have been saving my money.

Nice way to spread the goodness around! I don’t have kids, but our stimulus checks last year helped us put $2500 to a UGMA account for my new baby nephew!

What music you listening to? My playlists are mostly 80’s/90’s stuff! :)

Excellent topic Joel! The pandemic directly impacted my dad’s plans to retire. He was all set to pull the trigger and finally retire last year…then BOOM – global pandemic. He, like most of us, immediately lost 30%-40% of his investments when the economy tanked. So, he put his retirement on hold and waited it out – hoping the stock market and his investment values would return.

I’m excited to say my dad was able to retire at the end of last year (12/31/20) and has decided to wait till his 70th birthday in March to claim his social security. It’s been quite a learning experience for me to watch everything he’s been going through as part of his “retiring during a pandemic” stage of life!

Keep up the great work!

Wow – great story and congrats to your Dad. Sounds like he was in the bucket of “do nothing and wait for market to recover”. Hopefully he’s also shuffling to a more conservative allocation now that he’s retired, so if the market crashed again like that he can still rest easy!

Great article. My hunch is that for the majority of Americans who didn’t have job turmoil 2020 turned out to be a fine financial year and one with a surplus of savings.

But I fear there is a missing demographic in this survey of those who lost jobs or worked in industries that were decimated; hotels, restaurants, healthcare in some ways, etc.

Definitely big demographics missing, because the respondents are all 40 and older. Much of the gig economy workers are younger than this. But, I will say Personal Cap’s goal was to investigate “Retirement planning”, and 20s and 30 y/o’s probably don’t have much saved or would skew the data given their timeline is largely unknown (except for FIRE peeps – we have our stuff buttoned up!).

I know 1 person that took advantage of the CARES act and he used the money to pay off his house. I’m sure he wasn’t the only one in uncertain times people want to feel in control and paying off your home gives them that.

That’s cool. Taking advantage of the no fees to shuffle investments around and feel safer.

When I took a second job 5 years ago, I had no idea that it would be considered “essential” and be a stable move.

We didn’t change our retirement plans and actually purchased another rental. Our oldest is our new tenant. As far as our plans, they’re not overly complicated- 401k’s, pensions and several rental properties. We may never retire (unless health goes downhill).

We did use part of the 401k to buy the rental since the ROI is greater than any other kind of investment that we’re comfortable doing. We’re getting a 10% increase in value on those rentals year after year. If we wanted to, we could sell 2 of them and pay off the house, with $ leftover. Real estate for us has been our diamond in the rough.

That’s cool to hear, Lisa. I was wondering for all those people that withdrew from their 401k and didn’t need the money for regular living expenses – what did they use the money for?. Good to know it helped you meet other investment goals!

We had a house back in 2020 when the market crashed and I took our extra payment $1200 and bought a few different investments at different times. I have fzrox bought on 3/18 that’s up 71% today. If only I would have bought more lol but I’m glad I did.

haha I’m right there with ya. Shoulda woulda coulda bought more at the bottom! :)

I wonder if the people who withdrew from their 401k’s are regretting taking the money out. Hindsight is always 20/20 but I can’t imagine not being invested all throughout last year. Heck, I considered taking money out myself but I’m so glad that I didn’t pull the trigger due to my laziness.

Interesting data points to consider.

There were people that answered “I sold my investments, but have since re-invested at least a part of it”. It’s not a huge group, but this tell me there was some regret taking money out.

Retirement accounts are usually a 1 way street though. If you withdraw from a 401k or IRA and don’t return the money within a short time, you’re stuck with a taxable event and it not earning tax free growth ever again. You can’t just put it back.

Hope this pandemic will be over soon. Thanks for sharing with us.

Me too my friend.

I appreciate all this data and how you presented it — thanks for the topic! A friend posted on Facebook a few months ago asking whether he should take advantage of no-penalty distributions and turn his orphaned 457b assets from two jobs ago into a Rolex and a pistol. I somehow managed to avoid rolling my eyes out of my head while explaining that a 457b is worth keeping precisely because there’s never a penalty on distributions (unlike a 403b or 401k). If our retirement assets were held entirely within a 457b instead of 401k and IRA plans, that benefit would shave literal years off of our working career!

I guess consumers are what make our stocks rise, but blowing retirement assets on toys makes my head hurt.

Agreed. Converting appreciating stuff into DEpreciating stuff… It’s the opposite direction. :(

Guns rarely depreciate but yeah the Rolex that isn’t the best move.

This was a really interesting article. Thanks for sharing! We weathered 2020 from a financial perspective just fine. My direct boss was already planning to retire in a few years. I know he starting banking vacation days like crazy just to help create another financial buffer. But after losing his young nephew to a freak drowning accident and everything going on with Covid, he just decided to pull the plug and retire in the Fall. His thoughts were more along the lines of you just don’t know how much time you’re going to have left, and after all these decades he was just ready to be done with it. I still miss getting to talk to him, but I’m glad he was able to pull the plug.

Money aside, the pandemic has reminded us all how precious and short life actually is. Glad your boss pulled the trigger with retirement if that was his goal anyway :)

Glad to hear you weathered 2020 just fine too, J!