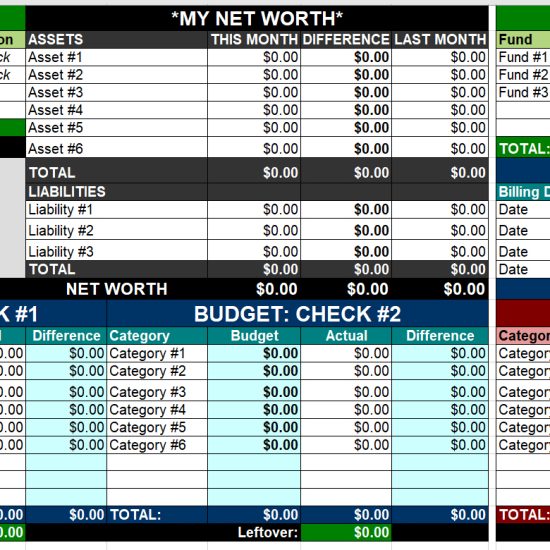

The whole point of budgeting, besides getting an A from yours truly, is to figure out how much “extra” you’re playing with every month. When all your bills are paid, how much do you have left over? Or an even better question to ask yourself – is there *anything*?

As crazy as it sounds, your boy J. never cared about budgets until just a few years ago. Or even money in general for that matter. In fact, if you were to ask me back then I would have told you I was The Man when it came to this stuff. Which was a) hilarious considering I was actually living paycheck to paycheck, and b) scary since I didn’t even know how much I was spending every month! And if a financial catastrophe hit? I would have sheepishly went running straight to the Bank of Mom & Dad ;)

You see, paying your bills on time and having enough to get by is fine if you want an average life. But if you’re looking for something MORE – something that you can hold onto and really build on over time – then “average” isn’t going to cut it. You’ve got to challenge everything and dig in to find where you’re leaking money. Where you can save more here, and chop off some more there. A habit to get into even when your finances are on track!

And the motivation you’ll need to see it all clearly is that number at the very end – the totals that shows you whether you’ve got $XXX left over or you’re going $XXX more in debt. THOSE are the numbers to focus on. Breaking even at $0.00 is still living paycheck to paycheck. What you really need to be working towards is getting that gap into the positives. The more you focus on that, the closer you’ll get to retirement. Or your dream house/boat/house boat/car/million dollar nest egg, etc.

For me, those totals were bright red. Every paycheck I received, no matter how many raises I got or new careers I tried out, I was losing money. It wasn’t enough to notice at first ($50 here, $90 there) but eventually it would have caught up and slapped me silly. How the hell could I be financially free if I never SAVED anything?! It’s just not possible. If you really want to be financially successful, you’ve gotta be bringing in more than you’re letting out. Plain and simple.

And the budget, as boring as you may think it is, will point you in the right direction. What a lot of people don’t get is that it does more than just show you how much your life sucks – it shows you how it could be BETTER. It’s the whole “ya gotta see the bad so you can see the good” kinda thing. The “knowing is half the battle” G.I. Joe type stuff ;) Even if you only follow a budget for a month or two you’ll learn more about your spending habits – way more than you will by reading this blog or any of those killer finance books out there.

And you know why? Because we’re all different. We all have our own way of living, our own way of spending, and our own plans for retirement. We’re all unique snowflakes, as our mother’s like to say, and your numbers will look completely different than the next person’s numbers. But you have to know what numbers you’re dealing with or it won’t really matter in the end.

Whether you choose to budget or not, at least find out how much you’re gaining, or losing, every month. And actually run the numbers – don’t guess like I used to do and think you’re coming ahead every month, only to find out later that you were leaking over $200 a month like an asshat. This is the number that’s key to your success. And until you can determine it, you’ll have a helluva time reaching those sexy dreams of yours.

Now who already knows their number? What is it? :)

————–

PS: If you are looking for a budget to start on, try out the one I use, or any others from the list of great budget templates/spreadsheets I’ve collected over time. Some are kinda purrty…

PPS: Can you tell this was a post I re-published all the way back from 2009? ;) As you can see, money doesn’t change in five years, nor will it in 50, 500 or 5,000 either. Our net worth sure can, though!

Photo cred: Pawel Loj

Get blog posts automatically emailed to you!

I used to track my expenses before, but never consistent about it. I have saved every month, but I think it’s still pretty low. Hopefully starting this month, I will have more savings because aside from my hubs work he just started his side hustle job. Yes, I totally agree that money doesn’t change in five years, but our net worth is. :)

I have nothing left over at the end of the month. But that isn’t because my spending is out of control. I make it a point to save first and then spend what is left over. I save 25% of my income and then what is left can be spent. That savings amount makes it tough to get by for the month too. I really have to be conscious of my spending.

Now Jon, always curious about this… when you (and others) say you “save 25% of [your] income,” are you talking gross income or net? Thx~

Connie, it doesn’t really matter gross or net. It’s the mindset one has to build up to actually save 25% of something. If you can afford gross fine if not do the net amount.

I always admire those who can “pay themselves first.” I always get my bills out of the way first to make sure I have enough and THEN if there’s extra it gets squirreled away into savings… If I had to pay bills last and there isn’t enough, I’d just have to dip back into the savings and play the xfer game! ;)

Though, I do understand and appreciate the mindset for this. It works best if you *know* you bring home enough to cover everything from the start, so by siphoning away the savings first you’ve curbed temptation right away… But that’s the part no one talks about. You need to first be bringing in more $$$ than your expenses or it won’t work!

My wife and I saved 51% of our gross income last year. I include everything in my budget including what my employer pays towards our medical insurance.

My wife went back to school a couple of years after we were married. It was also about the same time that we read Dave Ramsey’s Total Money Makeover and the Millionaire Next Door. We got on a strict budget and decided to pay cash for her school. It was a tight 5 years but when she finished not only didn’t we have to pay thousands for school, our income almost doubled. We decided to live on the smaller of the two income and use the balance to pay off debt and save.

Smart man! And wife!

I’m one of those people that see both sides equally. I know people who spend like it’s doomsday and KNOW they will work to 67 these are mid 40 year old couples.

I know the opposite too people who save, save, save, and try like mad to be debt free.

My issue with the first is “What happens if you get hurt or can’t work?” the other is “Aside from normal family what type of life experiences can you afford living like that?”

Fast forward a bit my neighbors are 57-58 have less than 100k “they say” and are going on trips, travelling, nice cars, nice house “Mortgaged”, but they live they do alot. My teenage kids get jealous sometimes as their kids go to “Italy, Mexico, Cruises” its seems every holiday.

Down the street is Jesse who has 7 figures, drives a 10yr old truck, and is very frugal.

So, what’s the point? There is no right answer. We all will die for some the security of $$$ in the bank and a sound retirement is the reward. For others it’s living each day to the fullest because our time is finite.

The blow it alls will regret it if tragedy strikes and the other group ask yourself on your death bed will you say “Man, I wish I saved more money?” or will you say “I wish I lived more it went by so fast!”

Yup, gotta do what best feels right to YOU no matter what the others are doing. As long you do that I think we’re on the right path whichever side of the money you fall on (and as long as you’re okay with the consequences too! Some of those who “live it up” get mad stressed with money once the high wears off from their recent trip/car purchase… Gotta find that balance)

Despite our six figure income, our number is zero. Paycheck to paycheck. But our student loan payments are as much as some people’s salaries, so there is that. No excuses though – we are embracing the fact that we have to earn more now that we’ve cut back spending and STILL can’t get ahead. Side hustles, here we come!

Oh crap! Good for you for being in the right mindset though. Those loans hopefully turned into some major competitive advantage, upping your human capital at least! You’ll more than make up for the $$ in the end :)

One of the best saving strategies is to pay yourself first. What this means is that you designate a certain amount of your paycheck as your pay and you pay that money to yourself before you pay your bills or anyone else.

Our number left over each month is 0 as well…but it’s because we use a zero-sum budget and put everything extra towards debt, lol. Sometimes it’s tough to look at it that way, because I would love to have tons of discretionary income to invest or blow…..

Yes!… great work… this is what I do as well… $0 left over every check because WHEN there is extra it goes into either my “emergency fund” line item or “general retirement” one… therefore on my spreadsheet it looks as if every dollar is allocated towards something, making it harder to want to spend! Financial discipline is a b!tch but hoping it pays off (literally) in the future! Wahoo, good job!

That works too :) ‘Cuz you’re *already* accounting for the extra money going where it should inside your budget (debt pay off, savings, etc).

I wish I knew about the saving 50% rule way back when. Now we save 50% but it it all goes to debt. Less rewarding, for sure. I need to try to get that message across to my kids so that they can do this type of savings now.

that’s hardcore, good for you! if you can pull that off forever you’ll be hitting your goals in light speed, my friend.

Glad you reposted this! I have not stalked your site far enough back to get to 2009 just yet. ;-)

Totally true, until I budgeted I did not realize that I was spending every single last dime. (and then some) Another benefit I found with budgeting is the pre-planning for future expenses. When my car insurance renewal comes due in November there is no “scramble” for the down payment because I budgeted a little month by month to have it saved up by then.

Such a great feeling!!!

GREAT POINT about the 6 mo. car insurance renewal, isn’t that always a pain… but now, with your way (and I do this as well), you just sort of go, oh, car insurance, ok, and boop! … you have the $$$! No muss no fuss! Great job!!!

Thank you Connie!

Heh my financial priorities are all over the freaking place. I am like a distracted kid looking at all the shiny objects “OOO ROTH IRA, I NEED IT!”, “OO BROKERAGE ACCOUNT, GIMME!”, “EWWW DEBT!!! SQUASH IT!!!!” and that is where my extra money goes (after auto investing in 401k’s as well of course). So I am all over the place!

As far as a number, yea I got an idea, but it will change with inflation and as life continues. I’m not sweatin’ it.

It could be worse!

“OOOoooh a new Corvette!”, “woahhhh look at that flat screen!!!” “Omg I HAVE to have that $20,000 diamond encrusted phone – gimme gimme gimme!” Haha….

We’re on the same page this week, J! I love what you’ve added here about budgets. For me, having money left over at the end of the month just ends up going to my student loans, so it never “feels” like I have extra money. I think I’m going to try to give myself a bit more margin and increase my contribution to my student loans through my side hustles. This way, I’ll be able to have that extra money (margin) at the end of the month while still paying more on my loans.

I mean, you’re already one step ahead of the game – you don’t have money leftover cuz you’re already sending it where its supposed to go! Debt pay off :) But I’ll never stand in the way of a girl and her hustle! Work it!

Yup, we have money left over at the end of the month, but it all goes to our savings targets! The number changes each month, due to things like property taxes and car insurance renewals, but our savings plans are for the whole year, not month to month.

I’ve just done a post on budgets so we’re on the same page this week! Anything we do have leftover gets moved swiftly across to various savings pots, though in our budget there is a savings aim. Just working on getting that higher percentage now!

Zero right now, but in a few months once debt snowball is completed I will have a $2k surplus that will be reallocated for a number of things. First beefing up our e-fund and then retirement etc. Looking forward to that time!

Holy crap, no kidding!!! Do you know what you can do with $2k extra/mo??

We have a set amount that we pay ourselves with first. If there is anything beyond that leftover each month, that money goes towards student loans.

We take money from our pension check each month and deposit it into out savings and brokerage accounts. Usually, at the end of the money there is still money left over. We do track our spending through Quicken and a spreadsheet. We set money aside for regular non-monthly expenses like insurance and real estate taxes so when those come due we are not in a panic where money is to pay that. Since we have no debt, the left over money either goes into savings or if we know a more expensive month is coming up due to a weekend trip or something similar, then we let the extra money stay in the checking account to pay for that.

I’m in the pay-yourself-first camp, and leftovers in a normal 2-check month can range from a couple hundred to over $1000. This is partly because hubs and I do separate checking, so I only pay the mortgage every other month. Weird to some people, but it works for us! My excess cash gets split between increasing our emergency fund and decreasing our mortgage principal.

Our goal is to save as much as possible. Some months we get bombarded with crap and have a negative cash flow, but most months we get to put at least a couple hundred in the ol’ savings account.

I don’t budget in the same sense you do (but I have tried tracking each penny). But I do run my numbers usually once a week to ensure I’m always carrying over money from each paycheck, even after my retirement contributions and my savings. I do want to do a month of tracking each penny again just to see if my spending habits have changed much since experiencing a little lifestyle inflation.

Oh man, I hate tracking to the penny and won’t do it again unless I’m forced (or joining you on a challenge ;)). I think when you’re starting out though it’s a necessity. We need that wake up call with our money when things have started getting out of hand!

One year, I tracked every penny in and out for a year. I had it set up in excel, it only took a few minutes a day, and by the end of the year, I had a neat graph showing when exactly we started breaking even, and a pie chart breaking down down the expenses. I’m getting back in practice, and I want to do this again next year.

Nice! You should totally blog about it if you haven’t done so already… would make for a nice juicy (and nerdy) article ;) Which people like us love!

I started tracking every penny in and out a few years ago- talk about a game changer! My tracking spreadsheets are like stepping on the scale, I might feel like I’m getting away with the occasional indulgence, but the numbers give me the reality check I need when the indulgences start getting carried away.

This is exactly how I think about it, but I LOVE the scale/indulgence analysis. I don’t zero-budget, but I do “pay myself first” in that the savings for maxed-out Roth IRAs and 401Ks and 529 contributions are automatic deductions from our paychecks. Extra cash used to go towards our emergency fund and car replacement savings. We have zero non-mortgage debt, a 6 month emergency fund that we hardly ever touch and, just recently, enough cash set aside to buy another vehicle when one of our cars gives up the ghost.

So now we theoretically have extra cash every month to the tune of $1500-$2000. Typically, I will use it to cover “emergencies” like a hot water heater replacement needed yesterday ($850) or annual expenses like life insurance or car insurance, plane tickets for vacation or other items. Anything left over after the big tickets purchases gets put into an investment or rainy day account.

Spot on J! This is why I love budgeting so much. Not only can it point you in the right direction, but it also gives you freedom. Freedom to live how you want and see in real numbers how your choices are getting you to where you want to be in life. We don’t know our exact number since it fluctuates with our business from month to month, but once we hit all of our buckets – retirement accounts, kids college, usual saving, etc. the rest is extra that we get to put towards usually the same things we’re already actively working on.

Thanks to a badass suggestion by Jacob from I heart budgets at camp mustache in May, I pay my monthly expenses out of my savings, pay myself a small amount for fun money, and then my actual paychecks get direct deposited into my savings account.

Awesome you got to hang with Jacob and MMM! Smart guys for sure.

I budget every expense to the penny. I do mine as an annual budget (I have a stable, salaried job so that is do-able for me). I then break that budget down and plan it out by month.

For instance, I know I have $3,000 to spend on clothes each year. While that may come to $250/month, the reality is that I tend to spend more like $1,000 in May and again in October and then the rest a little each month. With this system, I can account for that variation. Back when I owned a car it was particularly useful since I never knew when repairs were needed, but I could be sure it would happen some time during the year.

So at the end of the month I reconcile what I spent in each line item and if I spent more than expected, I have to budget less for the following months. Or if I spend less, I may add the extra money to savings, or I may realize that I will still spend that money, but in a different month.

You’re a numbers pro!! Love to hear that!

When I budget with my clients, the first thing we budget for is savings. We automatically build the gap right from the start, therefore every other financial decision has to fit around that, there are no excuses. I unfortunately was not taught to budget this way, but it is part of my practice now.

That’s a great way of looking at things. I personally don’t have this issue but I know a lot of people that should form their budgets this way.

YES! LOVE IT! Very very very smart.

Such a great, but simple idea – to know where one’s money is going. I like watching the Suze Orman show and it always bewilders me when people come onto the show and have no idea they have a deficit every month. I can’t wrap my head around not knowing exactly how much is coming in and going out each month and how you can’t know you’re in the hole a little more each month. But then again, I’ve always tracked my expenses closely. I guess if you don’t do that you might be in for a rude awakening, but at least then you can get yourself on a better path!

Yeah, I have a fair amount of money left over. I’ve got money set aside for future vacations, insurance, car repairs, car replacement, clothing replacement, taxes and fees, health care costs, furniture and electronics replacements, etc.

I’ve actually started to invest some of these longer-term sinking funds. If the markets crash before I need them, I can always dip into my emergency fund.

My extra money was going towards beer, coffee, clothes, junk food, mountain bike stuff, etc. Small stuff, but it added up. To motivate me to save more(aside from my 401k and regular savings account), I opened a taxable brokerage account. This is where I end up putting any cash I have left over every month. I do three money transfers- one at the beginning of the month, one around the 15th(mid-month), and then another at the end of the month. The first transfer of the month “pays yourself first”. I send in some money to the taxable account, and budget the rest for the whole month in two halves. For the second transfer(mid-month), I transfer any remaining cash that was not spent on the first half of the month. At the end of the month, I do another transfer for any amount not spent during the second half of the month. The hardest part of this method is knowing how much to pay “yourself first” at the beginning of the month. Then all there is to do is budget for the two halves of the month. Make sure you leave a little cushion on both budgets of each month.

Having three transfers prevents me from over-transferring money in case an unexpected expense comes up. It has worked for me- you should try it. This system I developed on my own, but I’m sure other people are doing something similar(if not, the same) as well.

HAH! You get the joy of sending money into your accounts 3x a week too – for that reason alone I like it :) And also exactly why I don’t automate my savings/investments too:

https://budgetsaresexy.com/2014/07/un-automating-finances-good-too/

I mean, technically, I have nothing at the end of the month, but that’s by design. I like having a target for every dollar that’s coming in… and if I don’t, it goes straight to debt or into a retirement account so I’m not tempted to spend it.

30% of net. Plain and simple. It works for us. I track every single bill & receipt to make sure we deliver on our savings goals, despite an appetite for travel and other fun pursuits.

Same reason I listen to Dave Ramsey every morning, sometimes I forget I need to save money and not spend it, I need a reminder. 2009 to 2014 still holds true!

There could be worse reminders out there! :)

My first budget showed me how much debt I was really in. I never calculated all of the minimum payments until I budgeted for the first time. It was scary. I have come a long way since then. Now, my number is in the black and I love that spot.

This post gave me a real kick in the @$$! I like to think I’ve got it all under control finances-wise, but there’s one thing I’m avoiding – challenging every expense. I need to stop avoiding this and actually start tracking because, like you said, you’ve got to see the bad in order to see the good.

Mine too is $0– because I send the money somewhere– like a retirement fund or emergency savings account.

Before I do that, it really varies depending on what’s going on that month.

When I was living in my mortgage-free home, sometimes it could be up to $2,000 a month or more left after paying the bills.

Yeah cuz you were a financial rockstar!!! Had a nice ring to it too, “mortgage free Mike” :)

I’m with Mortgage Free Mike! Well, actually, usually we have a tiny bit leftover because I budget like I’m going to spend everything we have and then spend like we have nothing. The point being, we usually end up pretty near $0 but budget in the savings.

I struggle to have ANY money at the end of the month, as most of it is allocated to investments/savings or spending early in the month (I pay myself first…).

Anything that is left, I use to pay down deductible debt (which I normally don’t focus on paying off).

Re. payrises, any payrises I get now, I bank them straight away to a separate account, away from any spending. Cost of living always seems to tracking your salary…

Great way to express a commonly used PF post idea. I heard a great quote the other day, and it goes like this – If it is not tracked or measured you cannot grow it -Unknown Author. I have been tracking mine forever in my head until about 3 years ago. Since then I have grown my net worth. I’ll tell you my number if you tell me yours. HA.

Great quote indeed :)

Knowing really is half the battle. Yo, Joe!

I love the simplicity of this concept. The delta, or the gap, is your only real progress (or problem, I suppose, depending on which side of “0” the gap is).

I’ll add a plug on your behalf for mint.com, which you have on your recommendation page. Tracking expenses can be as hard as counting calories, but mint makes it a lot easier. Plus, a longer term view can help you see where money is slipping slowly over time. It exposed a crazy amount of expense going to groceries for me, which we’ve been focusing on for about 4 weeks now.

I go off and on with the budget, but I have a pretty good idea of where the money all goes, and yes, I do have a little extra each month. Right now it’s building an emergency savings fund. Once it’s where I want it, I’ll be paying down a bunch of debt.

Like you, I had no clue just a couple of years ago. Getting on a budget was NOT FUN, and I still find it absolute drudgery to sit with my husband and go through the numbers. (Your blog title has a shock value. “Budget” and “Sexy” do not go together! You’re changing paradigms with that concept.) But a budget works! It really, really does. As for knowing how much we’ll have left over at the end of the month, we never do because my husband is self-employed and the numbers vary a great deal. But I can tell you that every left-over dollar goes against our debt. And it’s coming down.

You know what helps w/ the budget convos? Being naked. Just sayin’ ;)

It’s like that old book you found (“Thrift” it might have been called) from back in the 19th century. People change, but good money advice remains the same, 5 years down the road or 105 years. :)

Yeah! Exactly! That book (“Thrift”) was from 1875 and still just as accurate today. You made me want to dig it back up and check it out again – love that book! :)

https://budgetsaresexy.com/2014/03/thrift-lessons-samuel-smiles-1875/

Good thing my expense is not that much, I make enough where I can still invest a lot too. I can probably improve on my budget skills a bit, my excel spreadsheet skills isn’t that great. That’s another reason why I decided to track my net worth, to keep myself accountable.

Well, right now not much. Like many commenters above, I’m routing much of my income (30% of gross) to retirement or savings accounts at the beginning of the month. But I still really wish I had something left over at the end, because I want to get sinking funds going for clothing, car stuff, entertainment, etc. But something *always* seems to come up to prevent my coming in on budget, and I dip into next month’s slush or food budget, which then makes the next month tight and…. I need to get a handle on this. At least my net worth is climbing steadily, even if my end of the month money is consistently absent.

Yeah! 30% is no joke!! It would be much worse with that piece out of the puzzle ;) So def. good job on saving/investing and living off the rest – that’s not always easy to do.

We’ll be about $400 over this month, but this is our month to get dug out from under a mess we got into. 5 months with hubby unemployed really threw a wrench into our lives, but the bleeding is over, we’ve got the stitches in place, and it’ll be a couple of months until we can start paying down the debts in a meaningful way again.

At least we know where we are and where we are going.

Yes! That’s the important part there. You have to be able to track progress or setbacks to really grasp the impact and better line up the game plan.