Morning hustlers! You ready for a new week? A new chance to improve your finances? How about your mind at the same time? :)

Came across another money test on the internets, and according to The Motley Fool if you don’t answer these questions right you’re financially illiterate (d’oh).

Here are the 5 questions below, along with my own answers and then followed by theirs. Try to answer them first before cheating and see where you fall. Fingers crossed for you!

#1. What is your net worth?

Starting off with an easy one I see! $490,000. #BOOM I swear if you don’t know this one by now I’ve failed you as a blogger…

#2. Is it more important to pay off high-interest rate debt or save for retirement first?

I’m going to go with “pay off debt.” I can’t say whether it’ more important or less important as retirement since both are pretty damn important!, but I know emotionally speaking it’s much more gratifying killing your debt than it is saving for something 40+ years away. Early retirement scenarios excluded. And in either event, your debt will need to be gone regardless!

I also don’t know of an investment that will give you a higher rate of return than high-interest c/c debt (I’m guessing we’re talking 15% and higher?) and that’s also *guaranteed*. With each credit card payment you’re essentially locking in your return – and a high one at that – so yeah, I’m gonna go with “paying debt down first”, Alex!

#3. When should you start saving for retirement?

Dang it!! I want to say TODAY, but I just spent the past 8 seconds convincing you that your high-interest debt needs to be paid off first! Arghhh…

So I guess, after debt? But that doesn’t sound right… I’d never wait until debt is gone to start saving for retirement. Especially if you get FREE MONEY from employer 401(k) matches! Which you should definitely do regardless of debt because that’s an automatic 50%-100% return right off the bat depending on your company. And also guaranteed!

So my official answer here is: Start saving for retirement today, if you can take advantage of some kick-ass perks, and if not just hustle to get your crazy debt killed first while still throwing at least a few dollars towards retirement until you can put it in full throttle. I think it’ll make you feel better even if it’s not 100% financially “smart,” and honestly any decision you make here gets you closer to freedom.

#4. How much money will you need to have accumulated for retirement?

We’re getting trickier as we go :) But when you’ve finally commit to chasing early retirement (ie. financial freedom), one of the first things you do is run your numbers to see how far you have to go and where you’re starting from. Which requires knowing how much you spend each month (or how much you *think* you’ll spend in the future in retirement – as best you can), as well as your best guestimate of income needed to accomplish it. Whether from stocks, rental properties, pension checks, social security (hah!) or any other forms of passive/semi-passive income.

In other words, the amount you need to retire will be completely different than your neighbor’s. And if anyone ever tells you different they don’t know what they’re talking about.

It all hinges on your *expenses*. The more you need to live off, the more you’ll need for retirement (makes sense, right?). And to figure out how much you’ll need in retirement, a quick calculation you can do is multiply your yearly expenses by 25 – a “rule” most in the E.R. community go off.

For us, this means $1,560,000 in income-producing assets in order for us to retire fully ($5,200/mo x 12 x 25). With the focus on income-producing assets. The house you live in or the $100,000 rare coin you own (you lucky bastard) doesn’t count unless you’re selling it.

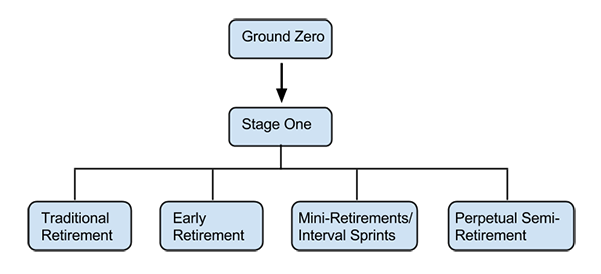

But keep in mind there are *stages* to retirement too. It doesn’t have to be an “all or nothing.” As my friend Paula puts it, there are mini-retirements, semi-retirements, and even retirement sprints! Where you work for a few months, and then play for a few months (yum). Feast your eyes:

I see myself in the perpetual semi-retirement phase as I’ll always be working on something even though I don’t need the money anymore. It’s just those *somethings* are whatever the hell I want them to be ;)

I see myself in the perpetual semi-retirement phase as I’ll always be working on something even though I don’t need the money anymore. It’s just those *somethings* are whatever the hell I want them to be ;)

If you want a fun spreadsheet to play with, plug your numbers into my early retirement calculator and see what it spits out. Knowing your date (and age) when you can retire puts everything in much clearer perspective. And can be incredibly empowering as well.

#5. Do stocks, bonds, or real estate grow fastest over long periods?

STOCKS!!!! Bonds are slooooow and don’t net you much (I don’t think?), and real estate, well, we all know how real estate is :) In theory it holds its value and only goes up, but as far as being “fast” I’d say depends on market and location conditions. Something I’m quite obviously not an expert in. My guess would be stocks, real estate, and then bonds.

**Answer Key**

A1. Net worth — You either know it or you don’t! Add up all your assets (savings, investments, real estate), subtract your liabilities (debts, loans), and presto – your net worth.

A2. Debt or retirement? — The Fool says high-interest debt first all day, every day. Basically comparing 10% (hopeful) market returns to 25% (vomit-producing) credit card debt. Which apparently some people have?? How is that even legal?? Anyways, they say that with lower interest rate debts it’s fine to manage while at the same time saving for retirement. Which is the case for us, and I imagine any other homeowner under the age of 50 since most carry mortgages for (what seems like) forever.

A3. When to save for retirement? — “As soon as possible!” Laaaaame. But also very true – which is why questions like these suck cuz you’ll never get a straight answer since WE’RE ALL IN DIFFERENT STAGES. The real question to figure out is when it’s “possible” for you. And, realistically, it’s usually a lot sooner than you think. Which is why I say to start TODAY even if it’s a measly $5.00. You won’t miss it, and it’ll get the ball rolling that much faster.

A4. How much money do you need for retirement? — “There’s no one-size-fits-all answer here.” Aww man! I wanted to not listen to them anymore ;) But it is good to see they go off the 25x yearly expenses idea too. I’m telling you, it’s all about those expenses in our lives! Gotta keep challenging them to push ’em lower and lower. The less you need to live off, the less you need to make!

A5. What’s quicker – stocks, bonds, real estate? – Stocks! Ding ding ding! And then according to their charts (which spanned from 1802-2012), bonds are next. Though it didn’t include real estate:

- Stocks @ 8.1% (9.6% between 1926 to 2012)

- Bonds @ 5.1%

- Bills @ 4.2% (Treasury bills?)

- Gold @ 2.1%

- U.S. Dollar @ 1.4%

Full story and answers here: The Financial Literacy Test

How did you do? You make me a proud blogger?? :)

Where I stand, the most important questions here were #1 and #4. You concentrate on those and the rest will follow – no matter which route you take to improve them.

And always remember: The only reason we pay attention to money is to hopefully not need to one day! Until then, you play the game the best way you can.

******

[photo by thierry ehrmann / dollar-fied by J$]

Get blog posts automatically emailed to you!

#2 is the only one I was sort of in the middle on, wondering how MF would answer it. I agree paying off debt should come first, but there are tons of factors that come into play.

For #5, I would be really interested to see the “rate of return” on real estate. I know it’s probably not a quick and easy number to come by, but depending on where you have your properties and if they’re commercial or residential, I’d imagine owning real estate could beat stocks into the ground.

My father in law bought a cluster of apartment buildings a few years ago. Instead of keeping them as one “complex” he split them and sold half of the buildings for nearly as much as he paid for all of them. He then hung on to the other half and collected rent, then eventually sold it for a profit. Now that’s smart business.

Lovin’ this test J$! Happy Monday to you!

That’s a true hustler right there!

@ChrisMiller, historically real estate around the United States has grown around 3%, but as J. Money mentioned it all depends on the area you lived and time of purchase. NYC and Miami over the past 5 years could have doubled the money.

If we didn’t have a mortgage, our needed for retirement would go down a ton! We would need well under $1 million if we dropped both daycare and mortgages from our expenses. Definitely itely a goal of mine to not have a mortgage!

A world without daycare or mortgage?? That would be magical.

I remember myself when I was thinking about retirement. I told myself that I had to do it that day. What I did was I computed the total amount of money I would save each day. I honestly was amazed with the result, which encouraged up until now to keep on and boost my savings for retirement. It was two years ago, I was 25 years old then. Now, I have already maximized ways to help increase my retirement fund such as maximizing my contributions to 401(k). It feels good when I know I have something for my retirement years.

Very smart :)

Do you say free money? I think this is a step some people over look in #3. At a minimum you should be contributing to your 401k to get the company match, it makes no sense to leave this on the table.

Exactly. Even if you think 401ks are “bad” as a ton of pundits are always blabbering about… I get that they don’t always give you the best options in terms of funds to invest in, and you can’t retire off just doing the minimum your whole life, but by and large they’re one of the best deals out there when you get matches!

“Play the game the best you can.” That’s really what it’s all about. So many people get discouraged by comparing with others who are in completely different circumstances, but doing your best is the bottom line.

You know it, sir.

#4 is a good reminder that finance is also about working backwards. I have a lot of friends that are so focused on their debt and the present day that they lose sight of the road ahead, too.

You know, the funny thing is I never calculated my net worth until last December. I think it was a denial mechanism! I didn’t want to admit that the student loans cancelled out the retirement and savings!

That’s a harsh reality, I know :( But at least now you can watch it grow each month since you’re on track to build that wealth! :)

I love how your writing is literally how you’d be saying it — though process and all hahaha. Sounds like you answered similarly to how I would, minus my net worth being “student-loan-debt-negative”!

I don’t know how to write/think differently :) That’s why I’d suck as a journalist!

Fun quiz! I did pretty well, although I have to admit that I don’t know how much I’ll need for retirement. I’m 27, so trying to figure that out now just seems like a futile effort. I save as much as I can towards retirement, so hopefully I’ll be in good shape. As I have a better idea of where my career/salary will take me, I’ll likely try to put some harder numbers to retirement needs.

Yeah, I feel like you have to be “in the mood” one day to figure it all out. Either that or a super nerd/planner :) No shame in saving as much as you can all the while!

I wish we had these kind of quizzes in college!

I don’t count the equity from our home either as part of our money needed for our early retirement years because we don’t plan on selling it. You’re one of the few people I’ve read that also mentions it this way. I actually don’t even count our home equity as part of our net worth and is one of the reasons I stopped by extra on it at the beginning of this year. I instead funnel all extra money into the stock market to reach FI quicker.

Yeah, I like to keep it in my Net Worth just cuz it is an asset (even though it’s not income-producing) and it helps balance out the mortgage debt, but I think it’s good to stick with whatever makes the most sense for you and matches the *why* of tracking it in the first place. Just stings taking it out of the ER calculations a little! haha..

We spend $33k/yr and have $1.3 million or so in investments (maybe $1.2 after today lol but not lol). So that means we have 39 times our expenses. I’d say we are doing very well, even if our investments drop significantly.

And agreed on the high interest rate debt – get that crap paid off before you try to max out all retirement accounts. I’d take a guaranteed 18%+ return by paying off debt if I had it. With the caveat that you might want to take advantage of any company match your employer offers in your 401k, and possibly stick enough into a 401k or IRA to qualify for the Retirement Savers Contribution Credit if your income is low enough to qualify.

I still love SO MUCH that you put all your numbers out there like that. So nice to see a real life example of someone in your sexy ass position ;) We’ve still got a ways to go w/ our expenses double that every year! ugh..

I guess birds of a feather stick together. My answers were exactly the same as yours!

I usually think those general personal finance posts on news publications are crap, but this one is actually pretty good. I think the 5 questions are extremely important and their answers aren’t that bad at all. Now to get the general population to pay attention to those things is a different story :)

I sometimes worry the only people that read these kinds of basic posts on news sites are people who already know the answers! But – C’est La Vie – We can all keep shouting from the rooftops “Start saving money! Pay off Debt! Invest in stocks!” and if nothing else, we’ll keep ourselves on track! :) Also, I thought the correct answer for “When to start saving for retirement” was “YESTERDAY, DUMMY.”

Hah – yeah. Most people just ignore $$$ stuff until they actually care enough (or something FORCES them to care enough!) to pay attention. It took me 25 years to do so and thank goodness it finally did!

(And yes – a much better answer with “yesterday” haha…)

I don’t think paying off debt or saving for retirement have to be mutually exclusive. If you have high interest debt (like credit card debt) then, yes, paying that off should be your primary focus. However, if you have lower interest rate debt then do both.

Interesting money test. I didn’t think those questions were all that hard, but before I was a PF blogger I might have had a bit more trouble with some of them.

Woohoo, I have answers to all 5 questions, and reasonably accurate answers at that! That’s much more than my former self could have side, 2 years ago.

note “side”, said*… stupid brain

That’s awesome! We’re becoming better adults! Haha…

J$ How would you put a value on a pension? Let’s keep it simple and say a person in their mid 50’s was getting $50k a year. What would you value that at?

Oh man, like you mean in a net worth?

I guess I’d just leave it out as it seems more like an income stream than an asset (though of course it is). But in terms of the Early Retirement/Financially Free calculations, this would play a major role! That one line item will drastically affect your #’s for sure – and most definitely needs to be included (provided it’s a 100% fact).

I have similar problems with valuing my blog and other online projects. You can certainly put a # on it, but until it’s time to sell you just really don’t know what the market will provide. So for now I leave those out too, and when/if the day comes to offload the profits will then be calculated into the wealth #.

Interesting question though for sure – I bet you’re not alone in wondering :) I’d google a little and see how others do it! Maybe it’s a multiplier of the $ or something?

There could be another question: What’s the single most important behaviour/measure that helps you determine your success in saving for retirement? Answer: Your personal savings rate…the higher the better. :) Yup, that indicator alone explains over 70% of investors’ success. WOW!

yup, savings rates are important! I would have guessed expenses, but I guess they go hand-in-hand eh? and you can have expenses without any income which would put you in pretty dire straights, haha… so yeah – guess it is savings rate :)

On Q2, I wonder….how do you factor in the tax benefits of contributing to a traditional 401k into the comparison with paying off high interest debt?

If you’re in the 25%/28% bracket and contribute to a traditional 401k, yes you get that 10% or whatever long term gain….but you also get some tax benefit by contributing pre-tax dollars. Of course, when you withdraw that money down the line, you may be/will be taxed on it, but maybe at a lower rate.

I think the math on “retirement vs. high interest debt” might be a bit more complex than what we/Motley Fool suggest. Ideally, you’d do enough to do both (max out traditional 401k while paying extra on high interest debt), but I’m not sure it’s quite as much a slam dunk to go after the debt as they even suggest.

Oh, and that’s without even factoring in company matches, by the way…..

yeah, I was gonna say – the company match changes the game completely. That’s a 100% return and will kill any c/c rate (hopefully – hah!). Not to mention all that match is then growing on top and making even more investment babies while you sleep :)

But yeah, matches aside it does get a bit wonky tax-wise for sure. Which makes me love the “do what makes you happiest” route even more, since both are smart moves!

Yeah this test is very east to me, and had all answers somewhat solid compared to results. Good job finding another test J. you just keep expanding the site readers knowledge.

Saw this test. I guess it’s a good generic article from Motely, but I have a feeling if you’re reading Motley, or especially this blog, you have a pretty good feel on most of these. Regarding Q2, it’s not necessarily an all-or-nothing answer. Obviously, 25% cc debt will kill you, but you also need to pay yourself first. Lesson learned from “The Richest Man in Babylon” – he paid off his debtors with each payment he received, but he also put aside some money to work for him, as well! Don’t forget to pay yourself!

-DP

Great answers!

This was a nice little brain exercise. Pretty basic stuff for us financial nerds but I wonder how the general public would do? I think question #5 is very important, especially for young people. If you’re saving for retirement and you’re not almost entirely in stocks early in life, you’re missing out on a whole lot of growth. People are scared of stocks, but they shouldn’t be because they almost always perform better than bonds and real estate in the long term.

Agreed. And this week was a perfect reminder of that too! I hope people bought, bought, bought during those crashes!