We’ve talked about compounding before on this site, most recently with the doubling penny!, but here’s another way to help get it to sink in more. And in a nice and nerdy way at that.

(Don’t you have to see something like 7 times before you “get it”? Or is that just a marketing thing? If so, we’ve got 5 more articles to go! Haha… but I’ll let you off the hook early with good behavior ;))

This popular trick is called the Rule of 72, and I’m going to let my new friend, Mr. “Good Looking, But Not Quite Sexy, Budgeter” share it with you because it was he who emailed it over in the first place. If you like it, you can thank me later for posting it up. If you don’t, direct your comments to him ;)

The Compounding Rule of 72…

Hi, I’m almost sexy (lacking rainy day fund), so I’ll have to pass off as a “good looking, but not quite sexy, budgeter.” I had a idea for a blog that you could add to your queue of 120 ideas I wanted to share with you. It’s really the only investment advice I ever give out, and seems to be right up your alley.

If anyone asks me for advice in investing (it’s happened 2 and half times. One time, I misunderstood the question), I tell them how Albert Einstein called Compound Interest the 8th wonder of the world. Granted, he was a theoretical physicist, not a financial advisor, but I’m sure if he wanted to give us advice on how to bake Bundt cakes or how to throw a slider we’d listen.

The Rule of 72 is my favorite way to explain this concept:

You take 72 divided by a rate or return and it will tell you how long it would take that money to double (or for the purchasing power to cut in half, in the case of using inflation rates).

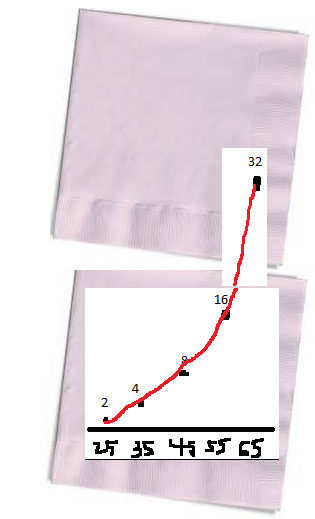

I’ll use 7.2% for my example because the math is easy. That means our investment will double every 10 years. When explaining this to people in real life, I’ll draw out on a cocktail napkin a chart showing the ages of an investor: 25, 35, 45, 55, and 65 across the bottom.

I ask them to pick a number to invest at age 25. $2,000? Okay, let’s plot that here at age 25. At age 35, that will double to $4k… then $8k, and so on until we get to $32k. I’ll connect the dots, which reveals a steady incline with a VERY steep curve at the end.

For effect, I’ll even purposefully make a “mistake” which requires a second napkin to be able to fit the return in the last ten year period, so it’ll look like this:

[Thank you MS Paint!!]

“Pick any 10 year period on this napkin… ” I’ll say. “Which 10 years do you like the return on investment the most?” Everyone (both people) points to the last 10 years leading up to age 65.

The lesson is obvious…start earlier and earn great returns later. Keeping $2,000 today foregoes $16,000 later. Imagine what the curve looks like when you add $2,000 EVERY year? Now figure this with 15% saved instead of just $2,000? The numbers start to get impressive.

[EDITOR’S NOTE: Remember our post on just doing one thing every year, like maxing out your retirement account(s)? I’d like to see how many napkins you need for that!]

I’ve convinced myself of this strategy so much that I’m not even planning on investing very much money in that last 10 years. Instead, I’ll opt to take a step down in my career to do something that gives me much more free time to do the things I want. Which, luckily for me, only require free time as the asset – not money (camping, hiking, etc.).

***********************************************************************************************************

Something to think about on this beautiful Memorial Day! Doing stuff in life that’s important to you vs. slaving away for the almighty buck.

If you liked this article, check out this one too on “pretirement” by my friend Flannel Guy ROI. And if you’re on LinkedIn and want to befriend this new email bff of mine, you can find him over here.

I’ll leave you with one last mind blowing piece on the magic that is compounding… Consider this pimping #3 so we’re already halfway there ;)

Courtesy of AWealthofCommonSense.com:

As Warren Buffett closed in on age 60 in 1989, his net worth was $3.8 billlion according to the Forbe’s List. This year, as Buffett approaches his mid-80s, he’s worth $58.5 billion. That means nearly 94% of Buffett’s current net worth was created after his 60th birthday.

————-

[Top photo by Beau B]

Get blog posts automatically emailed to you!

I love your napkin trick! That’s pretty cool. And I agree, the rule of 72 is pretty handy- at least it helps me understand the power of an investment in real terms, since sometimes “how long will it take my money to double,” has a more powerful and tangible answer than “what is my interest rate?” I also like your comment about how you may not invest as much in the last ten years. This is the reason why my hubby and I have been working our tails off to put away as much money when we’re young as possible. We’d like to “front-load” our retirement savings so that we don’t have to work as hard on the back end!

(that’s what she said??? ;))

I agree with Dee. I’m more of a visual learner myself. I tend to understand a concept better when someone draws it out for me. I’ve started saving for my retirement and intend to become more aggressive with saving towards it once my debt is cleared. Great post!

I think we all need to make these napkins ourselves, and then tack them to our walls and over our fridgerater! Haha…

The Rule of 72 was one of the first things that got me interested in saving money. I first made charts depicting it when I was 16, looking almost 50 years into the future. It was amazing what those graphs looked like, especially if I put in 10% or 12%. (I usually use 8% for my estimates today).

Do you still have those charts?? That would be pretty cool to look at now or frame to show your kids/grandkids one day :)

If the Warren Buffet fact doesn’t get you motivated at any age, nothing will.

It really is pretty insane, isn’t it?

This principle is life changing. Every high school student should be given that lesson and get tested on it before being allowed to graduate.

Even better – every EMPLOYER should give that lesson to triple remind you of what to do with those paychecks!

It all sounds so simple like that. Who knew that all I needed was a napkin? ; ) I have actively started to put more away for retirement thanks to getting motivated from your blog. Happy investing everyone!

I’m glad to hear that! I hope you ARE investing away and killin’ it! Keep going, friend!

This is good advice but I have one question: where exactly can you get high returns of investments? ;)

That’s a topic for another day ;) But I will say that it’s “high returns in the LONG run” vs short run, which is what most people fixate on (like the trending stock or get rich quick scheme). A good place to start is by contributing up to your employer match in 401k! That’s a 100% return every year off the bat!

This is exactly what most people don’t understand about spending money as well. The $50 I spend today is just $50, but it’s $800 to myself in 40 years (if I invest). That’s a big deal! That’s why saving money is important!

Yup!!! And I think if you can get into the mindset that it’s okay to spend *some* of your money now, regardless of the future benefits, then you’re more likely to stick to a good savings plan in the long run too. Most people I see go all hardcore and then burn out and reverse to hardcore spending! So finding that mix of spending now and saving later is key. Though much easier to say than to do :)

This is why I made investing a priority early on. I don’t have much income, hopefully that will change over time, but I do know that I’ve got my investments working for me to keep my cushioned in my future and that gives me great peace of mind.

Yes! Perfect!! Exactly what you (and others in the same boat) should be doing. Hell, it’s what we should ALL be doing regardless of income!

Compound interest really is a wonderful thing, and this story/example makes it seem so obvious. (Now I’m kicking myself for not investing at age 5!) Maybe it’s time I take this a little more seriously so I can let my money work for me.

Great trick to really see how compound spending works! I’m definitely a visual person and seeing it really makes sense of it rather than trying to figure out the math in my head.

That napkin trick was rather funny! I like this concept. It inspires people to take initiative early on in their lives, compared to investing when you’re old and tired and uncertain whether or not you will still live to see your investment grow. It is a risk to take, I know it might be scary, but what is life without taking chances, right?

The napkin part of the whole thing really seals the deal. Can’t look at them the same anymore :)

This is a great idea. It convinces people to make a move and make it ASAP! I like it!

Compound interest is the 8th wonder of the world!!!

I really wish we had started investing earlier, but we didn’t start until our late 20’s. This is a great reminder why it’s so important =)

Ha I love it. Mr. Not Quite Sexy reminds me of my dad who is always sharing life lessons on napkins like that haha!

Your dad would be in good company here :) Tell him to stop by and say hi!

I first learned of the rule of 72 in the book “Wealth Without Risk” by Givens – I didn’t like the book that much because he sounded like a sleazy guy selling you sketchy stuff, but that’s besides the point The rule of 72 put into perspective my investment potential and I use it all the time now to tell people what to expect. I like your napkin trick, I’ll will borrow it if you don’t mind =)

Go for it! We need to tell every person who’s willing to listen! :)

I’ve read that one before, and it really is amazing to know that Warren Buffett was able to make most of his money after his 60th birthday. Investing is really a great way to multiply a person’s money.

What an excellent way to show people the value of compound interest. The easier it is to understand, the more likely people will do it. Love this!

I have a love hate relationship with compounding. I like it when it provides money every month, mostly every quarter. But I hate it when I want my money to double every 3 years, and it doesn’t. I guess my expectations are very high for my hard working invested dollars. Good Post.

It could be worse – you could be in debt and the interest is compounding the OTHER way! ;)

I love doubling my money! I feel lame for having tied a lot of my funds up in my house, but bought at a good time and the ROI has been pretty good thus far. Hoping to capture the equity, lower my payment, and get to maxing out my retirement account very soon (in a few years) :)

I’d call that sexy, not lame :) Compound interest works in the opposite way too so you’re still financially killin’ it each time that mortgage payment goes out! You’ll move to hardcore investing when we’re all still scrambling to pay off our damn houses, haha… pros and cons either way :)

“Something to think about on this beautiful Memorial Day! Doing stuff in life that’s important to you vs. slaving away for the almighty buck.”

This is my takeaway, when in Rome.

A little late to the party, but you can use the Rule of 72 in other ways as well. If you assume that inflation runs at 3% per year, 72 divided by 3 equal 24, meaning cost of living will double about every 24 years. So while you may think you can live off a certain income level now, remember it will take DOUBLE that to live the same level of lushness a quarter of a century from now.

Depressing math, I know, but very helpful when doing projections of what one is going to need at retirement.

Yes, why did you bring that up again? ;)