Hidey-ho!

Another good month for the markets in Feb! And almost back to where we were in September when it last peaked! Only $24,135.31 to go for us to get back there, haha, how about you?

Here’s a fun snapshot of how it’s gone for us the past few months… Something tells me this is just the beginning of what’s to come ;)

(A delta of almost $100,000! Wild!!)

(A delta of almost $100,000! Wild!!)

In other news, we finally wrapped up our taxes for the year and had two little surprises!

- Surprise #1: we’ll be getting back a refund of almost $5,000 this year! Woo!

- Surprise #2: all that $5,000 will be wiped away as we caught an error in last year’s return and had to re-file and pay back taxes, womp womp…

So pretty much we’re Even Steven, which I guess is worse than being in the hole? ;)

How’d you guys do? Or you still pushing it off because it’s annoying as BALLS to file??

On the plus side, we found out we can max out our SEP IRA this year on up to $14,000 and some change, so I very happily moved some of our surplus cash into it which is why you’ll see a sharp jump in that section of our worth, and a scary red number in the savings one ;)

Other than that, it was a pretty low key month!

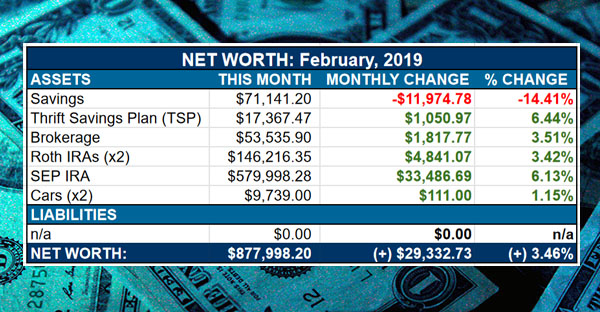

Here’s How February’s Numbers Went Down:

[NOTE: This is part of our Net Worth Series where we show a real-life snapshot of money (my money!) in hopes it helps put more perspective around this stuff… Some months we’re up and others we’re down (way down!), but it all gets displayed here – the goods and the bads – and then we discuss whatever you’d like in the comments section :) Here’s Net Worth Report #133!]

CASH SAVINGS (-$11,974.78): BOOM!!! RUN FOR THE HILLS!!! Haha… A big drop, but as mentioned above due to maxing out our SEP IRA for the year which we do in one clump instead of monthly, since it’s tied to business profits and I never know exactly how much we’ll have to play with ’til the end. Not preferable, but it saves me from making another mistake again.

THRIFT SAVINGS PLAN (TSP) ($1,050.97): Nothing too wild going on here, but it is a little bit lower than usual I think due to my wife’s new job switch and contributions/benefits getting a bit wonky. But so long as her *paychecks* don’t get wonky again (*ahem* gov’t shutdown), we’ll happily bide our time and let the system catch up as it will :)

BROKERAGE ($1,817.77): Another sweet bump here, but nothing out of our own doing as we kinda just plopped the initial $50k in it last year to diversify more from all our retirement accounts. Probably won’t add anything new in it for a while unless we get an unexpected windfall or something.

ROTH IRAs (+$4,841.07): Same deal with these bad boys – nothing new added, although we do have to decide now if we want to max out for the year or not? We typically push ourselves to do it, however my wife hit me with a doozie over the weekend and now I’m not sure what’s up or down or all around, haha.. More info on that as soon as I can wrap my head around it, but needless to say it’ll have a pretty big impact on our finances if we end up going through with it ;)

SEP IRA (+$33,486.69): The best part of the month! Where we threw in an extra $14,317 to the pot and maxed out our contributions for the tax year – woo!! I wish it was done when everything was crashing around us so we could scoop it up on discount, haha, but hey – that’s exactly why I never try to time the market – I fail every time! ;)

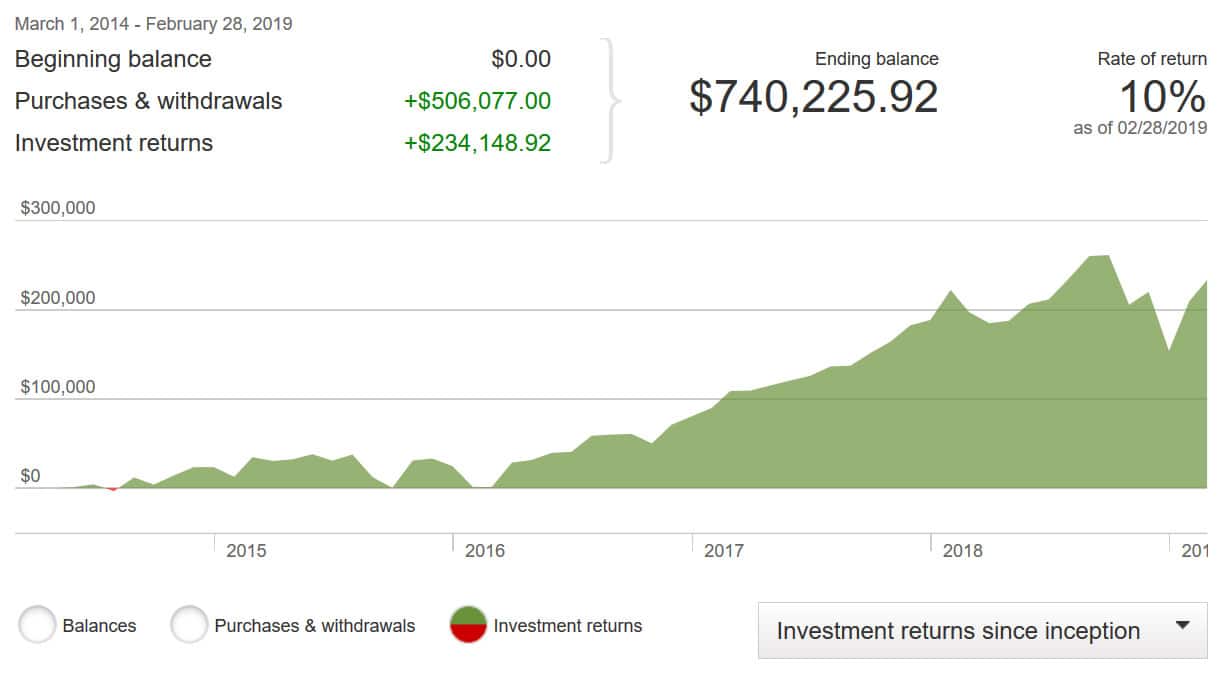

Here’s a snapshot on how our investments (VTSAX) has fared over the years since moving to indexing with Vanguard… Check out that return rate!

CAR VALUES (+$111.00): And lastly, we have the cars… which for the first time in a number of years actually went UP in value! Haha… Who knows why that happens when it does (maybe people are collecting beat up Toyotas now?!), however in the spirit of continuity we’ll let it be as that’s what we’d be relying on if we were to go out and try to sell them today… Which we’re not, but one day!

Per Kelly Blue Book:

- 2008 Lexus RX350: $7,254.00 (paid off)

- 2005 Toyota Corolla: $2,485.00 (paid off)

And that’s February! Total change in net worth: (+) $29,332.73

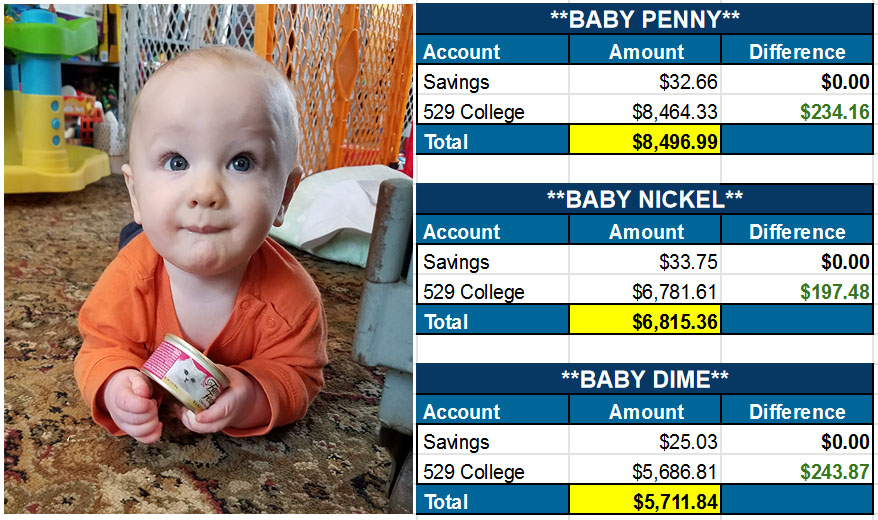

Oh, and last but not least – our cute little babies’ net worths… because lil’ ones need money too! ;)

As you can see, we don’t discriminate between baby toys ;) What baby wants, baby gets! (So long as it keeps him happy for a hot minute while daddy churns out these blog posts!!)

Your turn! What did your money do last month??? Anyone hit their first $10,000?? $100,000??? Anyone pay off all their debts and are running around in their underwear right now screaming their heads off in excitement??

That’s a scene I’d much rather watch than a boring ol’ Dave Ramsey yell ;) Hey Dave!! Why don’t you spice it up every now and then and let people flash some skin! You can call it the “Debt-free, and Clothes-free, scream!” It’s all about baring it all, right???

And I’ll stop there, haha…

Questions/comments/concerns (except for the nudity stuff), share below and we shall discuss!

Your friend in money,

![]()

PS: If you’re just getting started in your journey, here are a few good resources to help track your money. Doesn’t matter which route you go, just that it ends up sticking!

- The "Budget/Net Worth" spreadsheet - the colorful Excel template I personally use.

- The "Money Snapshot" spreadsheet - a simple Excel template I created for my former $$$ clients

If you're not a spreadsheet guy like me and prefer something more automated (which is fine, whatever gets you to take action!), you can try your hand with a free Empower account instead (formerly Personal Capital)

Empower is a cool tool that connects with your bank & investment accounts to give you an automated way to track your net worth. You'll get a crystal clear picture of how your spending and investments affect your financial goals (early retirement?), and it's super easy to use.

It only takes a couple minutes to set up and you can grab your free account here. They also do a lot of other cool stuff as well which my early retired friend Justin covers in our full review of Empower - check it out here: Why I Use Empower Almost Every Single Day.

Get blog posts automatically emailed to you!

I love these updates. They prove that once you save your money takes over the job of making more money. We all know this is true but it certainly helps to visualize it. You are getting so close to that million dollar mark!

Totally!! We hardly lift a finger to save/invest now vs the 24/7 hustling back in the day!! It’s all about getting that momentum going and then feeding the machine :)

My 2010 car I bought brand shiny new for $43,000.00 is now worth $13,000.00 according to KBB. Too bad I can’t go back and punch my younger consumer sucka self in the face and say hey dude, you don’t need that luxury. You want a new reliable car, ok, buy a brand new Civic at the most. It will most likely last 20+ years and cost less that 20k. “You’re welcome younger self…see you in 9 years. “Oh and by the way, a couple dudes out there have some really interesting blogs about money…start reading them.”

Haha… At least it’s probably a fun ride?!

On February 15th, I officially rebounded and my net worth equals what it was at the end of August. It’s been uphill since then so I’m still in “new high” territory.

Fun! I hope there’s many more of them before it gets bonkers again :)

I was more diligent about my cash only system for groceries and disposable income this month. It’s a pretty tiny budget and the cash only system is keeping me on track. This means more cash in the bank account at the end of the month.

So, in the 5 hours since I posted my exciting comment about cash only budget, I found out the company I work for just got bought out. Irony, I am off today so I have no details!

ACK!!! I hope you find out something soon!! And your job is safe!

It’s officially March-mas, that time of year when Southern Claus sneaks into my bank account and deposits a tax refund, a third paycheck, a yearly bonus, and a raise.

I’m one year away from being debt free. I’ve had debt for the last four years, and I don’t know how people live with that stuff their whole life.

I’ve been flirting with half a million since late last year, but March should do it. I’m at $485,000, and unless the market tanks, the fresh cash should push me well over.

March-mas- hilarious!!

AND GREAT JOB ALMOST BEING DEBT-FREE!!! You’re gonna have so much joy AND extra money to play with now :) Do you already have plans for it?

Stick it in my after tax investments. I’m already maxing our my 401k. The engineering industry is in chaos, so I foresee a future of work being on and off the rest of my life. I’ll need to be FI as soon as possible.

Excellent plan…

I was kicking myself three months ago for maxing out last year’s 401k early, leaving no space to buy when the market was on sale. But so it goes. We’re up >7% in net worth since January 1 even factoring in some pricey home upgrades (a new gas line and tankless heater last week, and a new gas furnace installation TOMORROW).

Had a fun experience at our neighbors’ house for dinner on Saturday. The topic of investing came up and I guess I must’ve looked fairly confident, because our friend said “um, are you into that ‘FIRE’ thing?” :D

HAH! Don’t you just love how mainstream it’s getting though??? My brother-in-law recently brought it up to me too and he’s in his 50s and now ready to retire like next year, haha…

I am cheering you on to a cool mil. The 7 figure club is right around the corner. I hope you do something to celebrate that milestone.

I’ll definitely have a beer…. maybe even two! ;)

You’ll be back over $900k in no time ;)

I just passed the €25k mark. All home equity and cash reserves (I don’t count retirement contributions, it doesn’t make sense with the system here).

It’s going to dwindle soon enough because about 8k are to be spent in the new apartement by the end of the year… Oh well. It’s tiny anyway since the amount I’d need for FI is somewhere between €500k and €600k. But hey, just starting the journey :)

(And still not sure what my strategy will be, TBH)

I love that you already have your “number” though! And that it’s 3x smaller than mine! :)

Well, it’s an estimate :) Partly using the formula, BTW (25x the income I hope for, probably part real estate and part stocks, plus the average cost of a house back home).

3x smaller than yours is not that good, given it’s just me and you’re a family of five. I have a partner, but he isn’t with me on this. Yet. He will at some point, hopefully…

Haha… he’ll wise up eventually ;)

Great job with the SEP IRA. I haven’t started taxes yet this year. We’ve been busy moving and fixing up stuff. It’s done now so I’d better get going with taxes. I have no idea if we’ll owe or get something back. It’s not good.

I think a lot of people are in that position this year :(

With the market being so good right now and spring coming, my home value suddenly rose about $50k thanks in part to zillow’s crap pricing algorithm. Anyway, I’m so close to $500K Net Worth. Sitting right now at $492,000…. Its temporary though, just waiting for the next piece of bad news for the market to drop 1000 points… I just want to see it hit 500K though, Ive been so close twice but never over the line

Enjoy it while you can!!! The next major jump is $500k away from that and takes foreverrrrrr to come! ;) Although you can probably count $750k too which I totally forgot and didn’t celebrate an ounce – woops.

Logged in this morning, $505K….Completely due to Zillow’s stupid algorithm that inflates my home value during the warmer months. Ill enjoy it while I can because any bad market news will push me back under, just nice to see 1/2 Mil for the first time ever.

Totally!

I’m working on finalizing the rest of our paperwork to file, it’s been annoying AF waiting for all the forms to come in. I hate filing “late”, it makes me feel like I’m going to be late for an exam -__-

Yay for maxing out that SEP! I was hoping to have a few more minor dips to maximize our buying power. I keep peeking around corners for the big drop to go with a recession but I should stop anticipating and just keep on with our usual investing every couple of weeks even though I really want to hoard cash.

Also, no no, J, no one needs to see Dave’s skin! ;)

Yeah I really want to hoard cash too, but then remind myself that I’ve never ONCE been able to time things to my advantage so I’ve pretty much just given up on it and continue on as-is :) So I’m right there with you!

(And glad you caught that Dave Ramsey line! I thought I was pretty clever with that one, haha…)

What an interesting blog! I keep up with my money quarterly but I had an unusual month so I ran the numbers for Feb. I’m an independent IT contractor and hit over 25k for billable time this month. Never even hit 20k previously. I had to spend 7k to prepare to sell my first rental property. Received an offer of asking within 3 days so hopefully I’ll get that money right back. Been the best financial month of my life so far! Easy to stick to saving 50% of income after taxes on months like this.

Nice!!!! Soak it all up, brother!

Always good to see the numbers go up.

Another high-water mark, up $14.2k to $932k net worth. I can almost see that second comma. :)

I am still liking the “Scaredy-cat” portfolio allocation I have. It didn’t go up as much as the “full” equity allocations, but the volatility is much lower. I am up $44k from my September number and have had new highs in 19 of the last 24 months.

REALLY CLOSE over there!!! Congrats man!!! I want an email as soon as you cross it and your world becomes brighter and shinier! ;)

You know it, J! :)

I had a pretty good February, investments are back up from the Q4 lows. Recently had my taxes done and I owe $3,000, dryer died and had to replace it ($775). If that isn’t bad enough my daughter needs her wisdom teeth pulled ($900). Needless to say… I’m hoping March will be a better month!

Ouch! Good thing for those investments to help balance things out more! I’ve definitely had those months… :(

As of the end of Feb, our net worth is up to $60k! Who care that $10k of it is due to a HUGE student loan payment? Up is up!

(I forget when the last time I commented about my student loans was…but we’re officially down to $26k and by the end of March, I should be right at the cusp of $20k! Movin’ and shakin’…!)

yeah you are!! loving seeing that too – getting so close!!

Our net worth is up to 1.35 mil. Our goal is around 2.4. The thing that will have me doing cartwheels in the street (probably in the snow) is that we were able to put extra in our IRAs and will therefore receive a bigger return, that will allow us to pay off our mortgage this month.

HUGE NEWS congrats!!! Debt-free and millionaire status – hard to beat that ;)

Taxes suck. Was so excited to see our $674 refund from our state but then got hit with the fact that we underpaid federal taxes…by $2,215. Whomp, whomp. Needless to say, I’ve changed my withholdings. But our net worth is looking up. Paying for a big spring break trip next month and we’re still killin’ it with a $5,000+ increase! Also, getting really close to paying off a car. If it wasn’t tax season, everything would be awesome.

Totally – much better to get a surprise of money back than money owed! I’m a huge fan of “lending the government” my money to make that happen ;)

Where you going on Spring Break?

Our son is now 5 so the happiest place on Earth of course! DISNEY WORLD!

Awwww…

My kids are always asking to go and it hasn’t even made it to my radar once, haha…

Does that make me a bad parent???! :)

Is the growth coming from deposits this month or growth, or both of them combined?

Love your newsletter!

Both, but more so the markets doing its thang ;)

Just hit $45,000 dollar networth. Will hopefully be at $46,000 when I update tommorow. Only 21, so still got a long way to go, but beginning to hit a point where momentum is keeping me going. Torn between looking to get on the property ladder, or waiting until I’m 25 and being able to buy outright, if I maintain my saving rate… decisions!

Love the blog, keeping me motivated!!

21 wow!!!

All I cared about were girls and beer at that age, haha..

Good for you man – definitely keep going and you will have so many opportunities later in life!

Your figures are very impressive. They are inspirational. Hopefully I can achieve similar results down the road.