Morning!

My boy James Clear just came out with a clever new newsletter, and I thought I’d be a bit cheeky today and copy it for a fun little blog post ;)

Here’s the idea behind his latest endeavor:

“Every Thursday, I send out my “3-2-1” newsletter with 3 ideas from me, 2 quotes from others, and 1 question for you. The goal of each 3-2-1 email is to share the most wisdom per word of any newsletter on the web.”

Now I can’t say my post here will contain the most wisdom per word on the web, haha, but let’s try it out and see what happens ;)

3 Ideas From Me

I. $1,000 checking account buffer. Melanie Lockert (DearDebt.com / Lola Retreat) recently asked how much people recommend keeping in their checking accounts, and my answer to that was a flat $1,000. Enough to shield you from stupid little mistakes that inevitably pop up, but not so much where it’s impossible to start or keep topped off! It also doubles as an excellent mini emergency fund and helps you sleep a little better at night. (Just make sure you’re not someone who spends everything they see! Otherwise chop off one of the zeros and go for $100 to protect yourself from yourself 👀)

II. $20 monthly donations to places you care about. I’ve talked about this one before, but I just added the 6th organization to my list of donations and I can’t tell you how EMPOWERING (and EASY!) it’s been since implementing this idea! I tend to be good at donating and raising money when it’s a *project* I’m working on (see: Love Drop and The Community Fund), but it’s always been a personal struggle doing it consistently in my offline world until recently when I realized *automation* is just as powerful here as it is in the other areas of finance. And now just a short while later we’re up to $160/mo and getting closer to my ultimate goal of 100 organizations to give to! Woo!

III. Calculate your Lifetime Wealth Ratio (LWR). Ever wondered how much you have left out of all the income you’ve earned over your lifetime?? Get a quick reality check by dividing your net worth by the total income earned that the Social Security Administration has for you (or your own records if you’re a super nerd!), and that will give you the ratio you’ve kept. Anything from 0%-10% is suboptimal, and anything 50%+ is sublime. It’s not an exact science by any means, but it sure does put things in perspective faster! Then use it to fuel your motivation.

*******

2 Quotes From Others

I. From Sophia Amoruso, author of #GIRLBOSS and one of the richest self-made women in the world:

“Treat your savings account like just another bill. It has to be paid every month or there are consequences.”

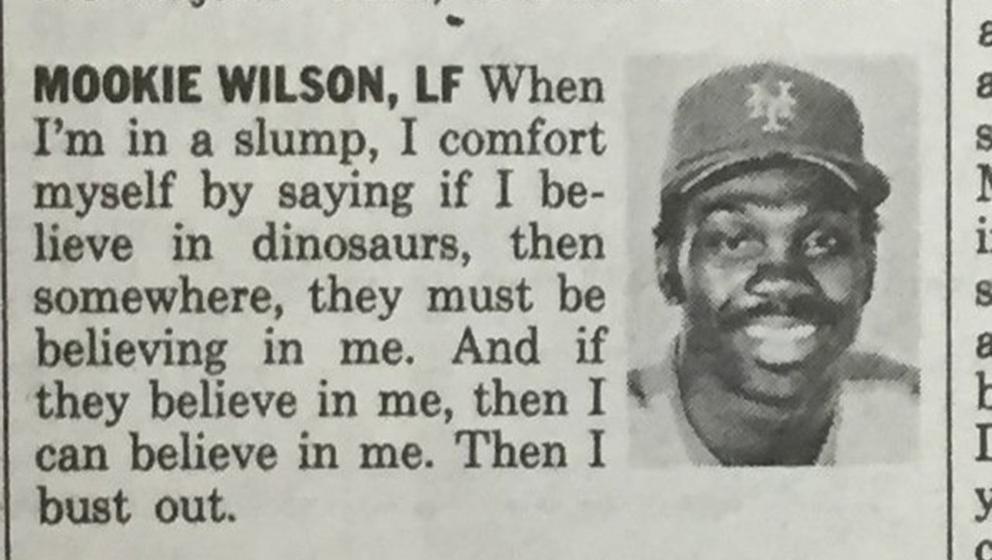

II. From Mookie Wilson, former Major League Baseball outfielder and coach remembered as the Met who hit the ground ball that rolled through Bill Buckner’s legs in the bottom of the 10th inning of game six of the 1986 World Series:

*******

1 Question For You

This weekend we’ll be wrapping up an old month and moving into a new one.

What’s the ONE thing you can do this next month, that by doing so makes your finances exponentially better? Or less stressful?

There’s a great book that deep dives into this if you need some help zeroing in – “The ONE Thing” – but try your best to really think about it as 20% of the things you do usually make for 80% of your success.

Good luck, everyone! Make those dinosaurs proud!! ;)

******

To learn more or sign up to James’ new newsletter as I just did, click here.

Get blog posts automatically emailed to you!

Hi! I’m trialling a new idea… One month a year (and I’m trialling it next month, September) I’m saving my entire after-tax monthly salary and putting it into a “building works fund”. I live in a block of six apartments and so don’t get to personally plan exactly when redecorating or repairs get done and don’t ever want any stressful surprises. Since I’m a massive YNAB budget maker I think I’ll be fine to live more or less normally next month.

That’s a pretty impressive statement!! Don’t know many who can stash a whole month’s income and still live okay!! Where’s your $$$ blog??? :)

No blog! I just YNAB, stay in touch with you and your newsletters, and before I buy something I ask myself, “Do you really need it?!” and then, “Have you budgeted for it?!” (and,occasionally, “is this going to make you fat?”)

haha…. You need to go start one – you’re a riot ;)

This reminded me of the clip in the movie “City Slickers” by Jack Palance. One Thing…just one thing.

Classic movie!

I keep $2k in my checking at all times. That level buffers me from most unexpected scenarios. Sometimes a G just isn’t enough for this baller. My wife and I both hate budgeting and prefer the pa yourself first method instead, so having this buffer works out well. If it dips low I just refill it over the course of a month or two.

Haha… you are ballers.

Ha! I’m a super nerd! My SSA earnings are a tab on my spreadsheet :)

One thing I can do next month. This year I created a value tracking tab on my spreadsheet and anything I spend money on that isn’t a living essential goes onto this tab and I assign it a value (shouldn’t have, obligatory, planned, relational, bucket list). At the end of each month, I calculate the total and find the percentage of the planned, relational, bucket list items. I aim for 90% value spending. I’ve been slacking on this the past couple months and there has been quite a bit more sporadic, thoughtless spending so I plan to refocus and make sure I’m considering the value of any extra spending I do before handing over the cash.

That is so brilliant!!!!! I LOVE IT!!!!

(And too funny you already have SSA earnings tracked, haha… you’re a pro)

Figured my lifetime ratio – came out to 31% – which is actually better than I expected – so Yay! I could probably sway it up or down a bit, but that’s probably pretty close. I also keep a buffer in my accounts – check, and check. I should make some structured donations – they seem to be scattered and I donate when people ask/post/mention a cause. My teens would like me to consider them when deciding who to donate to (LOL). But I should automate something; I’ll have to put some thought into it.

Please do as it’s been such a game changer at least for me… And of course you can always cancel/change them, but the nice thing is that it takes *extra effort* which means usually you don’t and keep giving away… The same results w/ recurring bills! Only feels much better, haha…

$1,000 buffer in the checking account? That’s way too low. I have at least a month of expense in there at all time and usually 2 months. Why keep it so low?

Why in checking vs savings?? All my real padding is in there :)

Oooh, a good post as always! I liked the Dinosaur quote! okay, this month I have got to pay off our credit cards. I never carry a balance…usually. But when we first moved into the new house, I opened a credit card with 0% interest to finance the furnishings and some repairs. I could have withdrawn from savings but I wanted the flexibility. Especially since the husband still had a condo to repair and sell. We paid off most of it but I’ve been meaning to do the last chunk. And…to pay off my husband’s stupid credit card which has carried interest. I would have paid it off ages ago but that requires his participation, so…here we are! Once that’s done I need to do a pay ourselves plan. I am not happy about how we have saved nothing over the last year. (Aside from 401ks). I was used to socking away at least an additional 800-1000/month in short term savings. Granted, I have a mortgage payment now, but we need to adjust our lifestyle to enable more than $0.i guess the good news is all the expensive stuff has been more or less cash flowed…but more has to be flowing back.

I’ve got faith in you!!!

Make it happen and then come back and tell us how it feels again to be c/c debt-free!!!! :)

Houses change things up like that for sure, haha… I already miss renting :(

I keep my checkings pretty low because I transfer savings as soon as we get paid and I pay bills asap too. If I keep 1k in there plus expenses I’ll feel like I have extra money and will spend more. I am going to figure out #3 though!

Good you know yourself like that! Plenty of other ways to get the mission done!

Love that quote by Sophia! #HowtoGetWealthy

Good tips, J$!. For someone who used to live paycheck to paycheck, keeping a $1k buffer in my checking, which I now do, feels incredibly peaceful.

My plan for this & next month, since I have some big expenses (car insurance, braces, etc) is to get some rewards points on a new cc. While I’ve saved the dough, I’m charging these things for the points then paying ’em off.

See you at FinCon!

I like the plan!! And even more so seeing you in person soon!! Gonna be fun!! :)

Brilliant post!

My percentage came close to 22%. I believe there is work to do. I have been tracking all my expenses onto a spreadsheet just like my net worth and this is helping me forecast my networth over next couple of months (includes padding for surprise bills). Nowadays i’m alternating every month between “Savings mode” and “Buy whatever you like mode”. This way i’m postponing things to buy to the next month and i might end up not buying them at all. That’s savings for me :)

I like it, haha… also keeps you sane throughout the process too as you’ve got to have some fun along the way!

3 ideas: open up an 12 mos cd for 3.5%; apply for credit card with a $100 bonus;donate to St Jude’s this month. Next month Alzheimers and following month Shriners.

2 Quotes: “We become what we habitually contemplate” George Russsell

“You are today where your thoughts brought you. You will be tomorrow where your thoughts take you.” James Allen

Question: If you received a salary to follow whatever you wanted to do. what would you do?

This was interesting and something I may continue to do each week or month. It helps me think about things and more importantly;plan an action.

GOOD!!!

Was very fun to read myself too – excellent quotes!

As a teacher, the one thing I’ll do this month is start getting paid again. That should boost my finances.

Thanks for being a role model to all our children!!! We need you!!

J Money,

Even though you copied this, doing it in a way that’s related to Budgets Are Sexy topics would be really cool. I wanted to offer my encouragement to continue this idea.

Also, for what it’s worth, I”m a first time commenter, but long-time reader. I’ve been checking in on you periodically since 2008 I think. My first memory of you was something about an issue getting with your wedding pics.

Love your blog!

Holy $hit!! That was def. 2008 time – wow! So glad you’ve been enjoying the blog man, thanks for letting me know! And now I see you’ve got a blog too! Going now to check out :)

Yeah, it’s been forever ago. I was going through a rough financial time, and was actively seeking out finance blogs and resources and found you somehow. I don’t remember exactly how, but I remember you were newish. Don’t get too excited about my blog. Despite the name, it has nothing to do with money.

yeah, it’s even better!! Letters to your daughter – so beautiful, jeez!!! Such a good idea, I absolutely love it.