Well that’s a new milestone! $50,000 drop in one month – the biggest on the books since recording these 8 years ago. Egads! What will we ever do???!

Answer: Keep doing what we’re doing and not get phased ;)

It definitely sucks on paper and looks like a complete $hit show if this is the very first time you’re seeing me present one of these (what a lame financial blogger, right?), but we all know some of this stuff is in our control, and some of it is not. And we also know we have plenty of up months that more than make up for these too, so it’s not totally one-sided (remember October of 2013 – up $62,000?)

At the end of the day it is what it is and we focus on what’s in our control. Which this month consisted of:

- Selling our house and becoming completely debt free! A win in the freedom/stress departments, a major hit in the cash reserves/equity section. One I’ll take all day every day though to receive that beautiful nectar of having no mortgages and maintenance! What a beautiful thing!

- Saving throughout the madness with Digit and our Challenge Everything – on rotation – accounts (more on these below)

And did not consist of:

- THE STOCK MARKET CRASHING AND EVERYONE PANICKING ALMOST AS LOUD AS THIS TEXT LOOKS RIGHT NOW #OMG-THE-WORLD-IS-ABOUT-TO-END!!!

It’s a great time to be in the media right now as a financial “expert,” that’s for sure :) Ratings thrive on this nonsense, but smart people like you and me know it’s heads down and forward march with our set game plans… We’re in it for the long haul, and this phase – just like all others – will come and go and the genius ones will scoop up as much as they can while on fire sale. It’s like a thrift store bargain bin out there right now! So beautiful!*

*For those of us who are young and have time on our side, at least… different story if you’re older and already drawing down your funds, but at least you’re not taking out *all* of it at once! It’ll go back up!

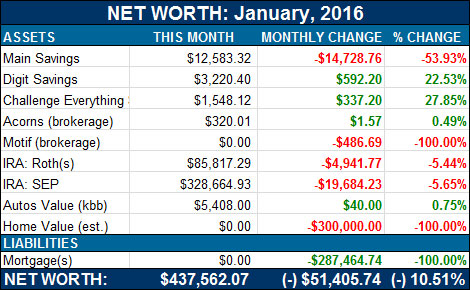

Here’s how January went down:

CASH SAVINGS (-$14,728.76): BAM – that’s the price of freedom, right there. Loss of cash but gain of cash-flow! To the tune of $900’ish a month. What we were practically paying each month to keep that place rented out, ugh… I sure am going to miss that! #NOT.

Jury is still out whether we’re taking the gracious loan offer from The Bank of Mom & Dad, but for now we’re letting things settle a bit and seeing how we feel. Will of course update y’all as soon as we’ve made a decision. Thanks for all the opinions and emails in the meantime! Y’all are surely passionate! :)

DIGIT SAVINGS (+$592.20): In positive-cash news, my favorite robot friend, Digit, continues to sneak away money from me when I’m not looking and our stash now crosses the $3,000 mark. Not too shabby after only a year signed up to them! Here’s my review of them if you have no idea what I’m talking about: Why I love Digit

CHALLENGE EVERYTHING (+$337.20): Someone last month commented that I’m just being lazy with this account now and letting the work of yesteryear continue to power it, and to that I said – “yup, pretty much!” And what a beautiful thing it is, right? I’m not lifting a finger in the slightest, yet every month this account grows by $200-$300. How could you not love that? :) Now granted it’s nowhere near the $500-$800 it was before, but my work-to-income ratio is better spent elsewhere at the moment, so for now we keep this on life support and just be happy with what we’re getting every month… I mean seriously – we’re not doing a thing!

ACORNS (BROKERAGE) (+$1.57): Pretty much a joke here, but hey – we’ll take it :) Beats out all the red below! For those new to the site, I use an app called Acorns which automatically rounds up my checking/credit card transactions every month and drops the difference into a pre-selected investment portfolio they helped set up for me. On good months the account gets about $20+, and on bad ones apparently $1.00 :) Once the market gets to it, at least. You can see my full review of them here if interested: Why I use Acorns

MOTIF (BROKERAGE) (-$486.69): Sayonara, Motif! Was a fun collaboration with you and my fellow financial blogger friends to test the world of dividend investing (read more here), but I had my fill and just not into active stock trading it turns out. So the $500 I just cashed out will happily join its friends over at my beloved Vanguard fund (VTSAX) and we close the door on yet another financial experiment here. If you like that sort of trading, however (stocks), Motif may be more up your alley…

IRA: ROTH(s) (-$4,941.77): Nothing too exciting going on here – come again later :)

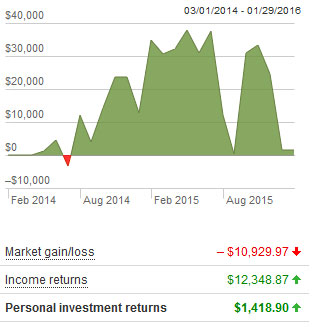

IRA: SEP (-$19,684.23): Nor here! It’s not every day you “lose” $20,000 in one sitting though… Def. gets you to hit pause before you move on your merry way. Here’s our entire progress so far since switching over to Vanguard indexing almost two years ago – kinda neat to see:

AUTOS WORTH (kbb) (+$40.00): Woopee! Our cars went up by $40! Haha… Yeah right, who knows why that happens with Kelly Blue Book… Cars are all depreciating assets no matter which way you look at it, but unfortunately many of us need them to survive (sanely) so they are what they are. And my beat up Caddy lives another month too! Even after the historic winter came and knocked out its batter – yet again. The thing keeps on ticking!

Here’s how both their values break down:

- Plain Jane Toyota (wife’s): $4,408.00

- Frankencaddy (mine): $1,000.00

HOME VALUE (Realtor) ($0.00): YAY!!!!! No more house!!! And how spot on were we, btw, when we had its value listed at $300,000 for almost the past year?? That’s exactly how much it sold for! We were hoping for $320,000 at first, but then realistically went with $310,000 and then dropped it further as the winter month(s) moved on and we weren’t getting a single bite. Turns out $300,000 was the lucky number though and we reeled in our big fish and now the rest is history… And good riddance.

(Awww, I’m so mean to our house! I don’t hate it *that* much… I just hated it the second half of our ownership (4 years) after I realized what a bone-headed mistake it was and wanted to get out ASAP. It lovingly served as a warm home for us and our newborn son at the time, as well as introduced me to you fine friends when I turned to the internet those 8 years ago to figure out how to budget for the thing ;) Who knew I’d go on to be a professional blogger and completely have my life changed? So I will miss you a little bit, old housey-house, but we both know the time had long come. And I wish you nothing but success with the new – seemingly wonderful – tenant you now have inside of you. Good luck guys!)

MORTGAGES ($0.00): I don’t think I’ll ever get tired of seeing that number :) I may just have to include it in all future net worth updates just to keep my excitement going! Haha… For the first time ever since knowing any of you, we are completely – and utterly – debt free! Incredible! And I wish nothing but the same for you too once the time has come!

Bye bye old mortgages…

- 1st Mortgage: $000,000.00 (30 year conventional @ 5.5%)

- 2nd Mortgage: $00,000.00 (HELOC @ variable 2.8%)

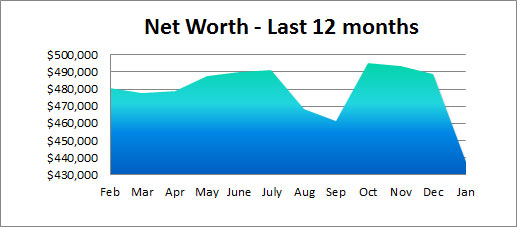

Here’s how the last 12 months have played out:

And here’s the net worths of our two beautiful boys so far too. You know, cuz we’re nerds like that.

And there you have it! The biggest loss on the record books since June of 2013 (-$40k) and we’re still smiling on the other end :) I hope you guys lost a lot less over there! Unless you’re already millionaires, in which case losing a lot more is actually GOOD! Wanna trade?

See you back on Friday,

![]()

——–

PS: Like these? Check out all my net worth updates over the years…

PPS: Don’t like these, but want to see 200+ other financial bloggers’ worths? Here you go.

PS: If you’re just getting started in your journey, here are a few good resources to help track your money. Doesn’t matter which route you go, just that it ends up sticking!

- The "Budget/Net Worth" spreadsheet - the colorful Excel template I personally use.

- The "Money Snapshot" spreadsheet - a simple Excel template I created for my former $$$ clients

If you're not a spreadsheet guy like me and prefer something more automated (which is fine, whatever gets you to take action!), you can try your hand with a free Empower account instead (formerly Personal Capital)

Empower is a cool tool that connects with your bank & investment accounts to give you an automated way to track your net worth. You'll get a crystal clear picture of how your spending and investments affect your financial goals (early retirement?), and it's super easy to use.

It only takes a couple minutes to set up and you can grab your free account here. They also do a lot of other cool stuff as well which my early retired friend Justin covers in our full review of Empower - check it out here: Why I Use Empower Almost Every Single Day.

Get blog posts automatically emailed to you!

CASH SAVINGS (-$14,728.76) – at $900 savings per month you have a payback period of 16 months. Not too shabby.

And that’s just the rent, not anything like the maintenance and upkeep!

I’m betting you’ll have a huge load off your mind now.

Best decision I’ve made in a while :)

A $50k drop? It’s like you aren’t even trying! ;)

It is good that you have the right mindset when you look at these month to month shifts. I can only imagine the panic out there with people who don’t have a true understanding of how the markets work and how when you treat things with the right approach, you get to capitalize on the fact that the market goes up 80% of the time.

I only look at my net worth or stock portfolio every quarter so I normally don’t see the impact of the big drops. It helps me keep my sanity! :)

Well that’s no fun ;)

A $50K drop would have most running for the hills, but when you break it down half was to free you from the house, part of the long term plan and increase cash overall and the other is the market, again another long term plan. Yes tough to see that much cash go out the window in such a short period of time, but you’ve got a plan!

Looking good, looking good! I’m lucky that as just recently started our taxable investment account; so for us, everything is on sale. Yippee. Our retirements accounts are a different story. Thankfully we’re in the “we have time to recover” camp. Keep up the great work with the mortgages ;) I’m jealous.

I got REAL lucky w/ the timing too back when I first started investing heavily – 2008 through 2010 – def. helps grow the $$ faster! (and unfortunately no way to time it to your advantage all the time, so we just go w/ the flow and do our best, right?)

Considering how crappy the stock market performed in January we didn’t do to bad overall. We took a $4,384 hit to our investments but our net worth only dropped by a total of $2,652 in January. That little market uptick on the last day of the month helped but that all went away yesterday, so I’m still preparing mentally for another low month. Good thing I’m young and in the market for the long term or this volatility would really suck.

Keep your chin up and enjoy the sale prices :) I snagged a few stocks in the last few weeks at some pretty spectacular prices and although our investments took a big hit, too I’m looking at the long term. We won’t touch those stocks for at least 15 years so I’ve got a while to ride the waves :)

Was waiting for this update. But, now I want to know how this changes your early retirement spreadsheet (since your expenses went down).

Hah! Me too actually – haven’t run it yet :) Def. be better in the cash flow department, but not as much in the investments growth one to sustain that sexy live of freedom!

Will run and post sometime soon here – good reminder.

So, fun fact, your drop in net worth last month was quite similar to the amount I owe in student loans. Luckily, you’ll get your money back in the future when the markets go up again. (Not so much with the student loans…)

I love that your car value went up — that’s a rare thing to see! :)

I’ll be waiting for that post when you kill them once and for all :) We should have a blogger party!

You stopped a money leak that was also emotionally draining. So it’ll pay off in time! Love your perspective of how your “mistake” prompted your career.

My husband just told me yesterday our retirement accounts are down $50K. This to shall pass. I look at it as everything is on sale! ;) You are wise J – “Keep doing what we’re doing and not get phased.”

I kind of enjoy that your net worth drop is bigger, by far, than my entire net worth!

jeez… yeah, the more you have invested the wider the swing in either direction! and the funny/crazy part is you literally don’t even have to move a finger the entire time and it’ll still grow or drop if its tied to the market.

Tough month but as you mention, you have to step back and really look at things from a broader perspective, which it sounds like you’re doing. In the grand scheme of things, it looks like you’re chugging away just fine.

Congrats on the sale completing. I think this is definitely one step back for two steps forward!

Less money, less problems!! :)

I think I missed your Bank of Mom & Dad loan post. I just published a piece on How to get our parents to pay for everything as an adult with tips from 7 people who did! Might be pertinent.

As for net worth, losing sucks. I’ve mentally prepared to lose several hundred thousand this year. And it’s coming to fruition already. Whee!

Glad you sold the house!

Sam

Nice – will check the article out!

But don’t feel bad for anyone losing hundreds of thousands because it means y’all are invested quite nicely! I tip my hat to you, good sir.

Congrats on offloading the house! Now it will just be an upward trajectory :)

Long time lurker, our NW numbers have been close for years. I admit I don’t check my NW as much in downturns, but seeing your consistency inspired me to do my own monthly check, even when I don’t like the numbers. You are like my NW accountabilibuddy.

As for the markets, as long as we are still in the accumulation phase a drop is actually a good thing. It means higher yields for future contributions and dividend/cap gains reinvestments.

Proud to always be a NW accountabilibuddy! Well done staying on top of it!

If you got rid of your house (and mortgage now is $0.00), then you I presume you are renting.

If you mentioned the $0.00 mortgage then you should add back it to $xxx/mo in rent.

People do not sell houses and get rid of mortgage to stay in streets and pay absolute zero for housing!!

I never said we don’t pay anything in housing, but monthly expenses such as rent do not go into Net Worth Updates (or else you’d see cable bills, insurance, Target runs, and all those beer costs adding up in them).

We’ve been renting for almost 3 years while simultaneously owning this house and renting it out another state away. But now no more mortgage costs/losses ($900’ish) so we’re in heaven!!

Hey J,

Damn that’s a brutal drop, my portfolio actually flew up as I added new capital and the TSX recovered late January. Things are dropping again… but for us intelligent investors it just means sales are abundant!

DB

way to go! I salute you, sir.

Congrats on ditching the house and debt! I was very hesitant to run my numbers this month because I’m tantalizing close to a financially goal I’ve been itching to hit and with the market downtown I’m so annoyed that I’m about $2,000 away. If everything were A-Okay, I would’ve passed it and then some…should be there next month!!

Yeah, you’ve already done all the hard parts now so just a matter of *when* vs *if*. Congrats!

Ouch! But like you, I try not to pay attention (or at least not panic) to dips in our retirement accounts. Because we have decades yet.

And don’t forget that people drawing down on their accounts have usually moved to lower risk stocks, so their losses should be less. And they’re still only drawing down a small percentage each year. So they still have time to recover, too.

All in all, people need to chill the hell out and take the long view, just like you!

Good point!! Forgot you get out of a lot of stocks/funds by that time…

You should be a financial blogger or something :)

Whoa! That is some drop, but I’m glad you’re pumped about the house (I would be too. We lost $40K about two and a half years ago, and it was the best thing ever).

And I’m happy that I officially passed you on the net worth tracker (although, I’m guessing it will be for just a few months since I’m hoping to unjob in a few months here).

You owe me beer the next time we meet!!! :)

Time to shut it down and put money in your mattress instead!

Yup, game over. #ShutsDownBlog

I share your pain. My net worth went down as well. It feels less painful she you share it.

Thank you for posting.

http://www.alainguillot.com/net-worth-february-1st-2016-down-7769/

I like your goals section at the end – that’s a great idea!

Dang, you know how to make a guy feel better. I’ve done a detailed tracking of my monthly net worth for the last 44 months, and loved running across your site a year ago to see others are doing this too! I was feeling bummed about my $957.68 dip in January (thank you, investments for the $5,250 drop)! Looking forward to seeing you break the $500,000 and $1,000,000 marks. You’ve got a big head start on me, but race ya there :-)

Haha you’re on, brotha!

Yeah, pretty brutal month if one invests a lot of emotion in the numbers. Luckily I don’t, since I have some time until retirement. The market will recover. Down $69K since the end of December – blech.

It’ll be interesting to see where we all are this time next year!

I LOVE that you still wrote in all those zeroes for the mortgage values to really drive the point. HAHAHA! Awesome!

It’s the little things in life :)

Funny how math works – the bigger the nut the bigger the change in REAL dollars, not just abstract percentages.

I think about it sometimes like – “Hey, do you know how long I’ll have to work and save to get that $30-40K back I lost since December?” They say there is a psychology that we enjoy a dollar of gain much less than a dollar of loss hurts, or something to that effect.

Anyway you have the exact right attitude towards it all!

Why not pass on the $14k loan from the parents, but know you could borrow from them the exact amount you need if an emergency did arise? That way no obligation to them, you’ll be more motivated to save since you’ll see the low amount in your account, but have the safety net if you reallllllly need it.

Yeah, that’s an idea we’re considering for sure. At the end of the day though it all comes down to comfort levels – especially for my wife – so we’ll have to see what a little more time brings us. I’m personally okay with either route at this point. Pros and cons.

$50,000? Pssh! I was reading on the Early Retirement forums about a guy that lost a million in a day (DAY!!!) during the 2007-2009 crash. I wish I had enough to lose a million in a day (my record is probably closer to $50k or so). :)

I haven’t looked at our January numbers but I bet we are down $75-100k or so given the ~5% drop in the market.

Much like you, we are continuing down the path that we’ve been on for a while. We aren’t selling more than 3-4% of our portfolio during the year to fund living expenses so not too worried about this downturn even if it’s a multi-year downturn.

P.S. – congrats on the hugely successful launch of the MONEY podcast. I haven’t had a chance to listen yet but I’ll be over shortly to add another listener to the count. :)

Thanks man! It’s been incredible and overwhelming all at the same time.. Just shows how awesome and encouraging our community is here! Hope you like it! The one we just dropped yesterday featured Mr. Mad Fientist :)

And crazyyyyyy about losing $1 Million in a day! I can’t even fathom that, jeez…

Why not aim for a $100k drop next time? Kidding of course. Yeah the market has been pretty crappy lately but it means for us long term investors we can buy stuff on discount. Getting rid of mortgage will be huge for you guys in the long run. Congrats!

OMG!!! why is it that I just found this blog??? I’m new to this site but I’m soooooooo happy I found it. You got all the tools and tips and support I need to once and for all take control of my financial situation. You are amazing!!!

Hooray! You just earned yourself my new favorite person of the day, haha… I’m so glad you’re liking it! What a crazy post to come into too with this one :) Hope it all helps!

We got hit hard this month, too. Logging in to check those accounts was not a bright spot in my day! But made me thankful that I’m years away from retirement.

Hey J Money, congrats on selling the house! I’m sure that will be great from a cash flow perspective now. I’m curious if you’ll continue to max the SEP IRA this year. It looks like 95% of your net worth is in tax-deferred accounts and I was curious if you were trying to build up your cash / taxable portfolio for medium term goals/purchases.

As of right now we are planning to max out our SEP IRA – which will basically demolish our cash savings, but the tax benefits – and overall growth! – just can’t be avoided in my personal opinion :) So we’ll be taking the riskier route there, but should pan out – and then some – in the future.

As for taxable stuff, yeah I def. need to start thinking about that more and setting some aside, I just haven’t for whatever reason and guess waiting for our income to jump up here when it’ll be a lot more do-able. Right now we’re all living on my single (not-so-steady) income here as a finance blogger, but as soon as my wife gets her first job in her new career (she’s been working on her PHD for yearssss) it should all be a different story :) ‘Till then, we continue to hustle!

So, you sold your house… are you going to be renters for life now? Interested to know how this will work, I know my wife would not be happy about that kind of scenario (we’re renting currently, but she certainly plans to own a place at some point)

I’ve long since quit calling anything permanent these days as I realize more and more how our lives – and goals – are ever changing, but as of now I do not plan on owning anything in the very near future :) That could change when my wife gets a job or wants to settle down more, but for now it’s the rent life for us and we couldn’t be happier!

Sacrificing debt and asset together to gain future cash inflow is a great thing. Good job selling your house and welcome to the renter’s club. You know how it is. Renting gives you so much freedom that I walk 5 minutes to get to work everyday. If I find another job, no problems. I will find another rental nearby.

My portfolio had been in tough time for a while and here I am buying more and more undervalued stocks. When tide turns, we will recover all of the paper loss. Thanks for sharing!

Cheers!

BeSmartRich

You know it!

We got hit too, but not as hard. I’m with you, stocks will be back. After that big crash a little more than a week ago, we threw $11k into our 2016 Roth IRA’s and it’s already doing better. :-)

Our net worth is at $482,540 – http://www.budgetinginthefunstuff.com/february-2016-net-worth-482540/

Let’s just keep trucking!

And just like that you’ve beat me! Congrats, mi lady!

I understand how that feels, my real estate investments took a hit too, losing a lot in the last 18 months because of the oil glut ( including cashflow). The good thing is that I’m not selling so mostly a paperless, like yours:)

DUDE CONGRATS!!!

My partner took a loss on his house sale but we could not be HAPPIER to have it off the books!

Worth it!!!

Give your partner a beer for me and we’ll rejoice together!

p.s. check out the Rent vs. Buy thread of Reddit from yesterday.

https://www.reddit.com/r/financialindependence/comments/43v9r3/rent_vs_buy_mega_thread/

RENTING is back in fashion big time!

nice! going over now…

This is my first time visiting your site, and I love what I’ve read thus far.

I’m in total agreement about stock market volatility. I could care less about my personal portfolio balances dropping. It’s one of the many privileges afforded to us index investors; we never have to panic. As long as those dividends keep getting paid and a zombie apocalypse doesn’t break out, the future looks bright.

And congratulations on getting rid of the house. I bought a rental duplex when I was younger (on top of my actual house). I really enjoyed the business aspect of managing it (tax deductions, rent checks, etc), but I sold both properties for a slight loss to move across the country for work.

Since moving, I’ve been strictly renting, and it’s actually saved me an incredible amount of money due to the real estate prices in my new area. Buying vs. renting is never black and white, and I think your story illuminates that well.

I’m looking forward to reading more of your work.

Connor

Thanks for stopping by, man! Glad you’re enjoying the blog so far. Going over now to check out yours – can never resist anything with early retirement in it ;) And seems like you have a good angle going w/ the actuary part too. Good job getting it out the door!

“Here’s how January went down” –> Appropriate for us all this month ;)

Still awesome that you have monthly updates since 2008 #NetWorthWarrior!

MrZ

Congratz on the – in our opinion – bold move to sell the house.

Friends of us rent as well. They have less worries now as the landlord takes care of the house for them.

Our loss in January was less, and we have reached the mental state that we do not panic.

Beef up those 529s, unless you plan on your kids taking out loans for the difference, which admittedly has a lot of merit. I dumped money into one back in 2008 when everything was shit and my oldest (almost 8) now has ~40K on a 28K total investment, even after all this turmoil.

P.S. I feel you on the mortgage, I reached hard to get my place, now I’m hating life paying off a 570K Mortgage….It’s just, you know, a regular house costs a minimum of 500K in the DC metro part of Maryland. Unless you want to live in a crap area that is…

I have to tell you though, every month this mortgage hits, I keep thinking, rural South Dakota is looking better every day. I’d be FI within 3 years if I just had the balls to move.

Hah, indeed my man, indeed…

If only we could move out all our friends and family there too! But what’s the point of $$$ if we seclude ourselves?

We’ll be back at 529s once our 2nd income comes back later. For now it’s all paused until we’re out of this phase.

The $50K decrease would have many jogging to the mountains, but if you break it along 50 % had been to free a person from the property, part of the extended prepare in addition to increase funds all round plus the various other could be the industry, again yet another extended prepare. Yes difficult to discover a whole lot of funds head out this screen in such a small timeframe, but you’ve bought a plan!

Congrats on the (sans) mortgage!

Also, that “camel” IRA graph. Silly market.

Oh my gosh, that’s a tough one, Jay. Your attitude is stellar. I hope it is rewarded by many months on the positive side. Bonne chance!

You have the right mindset, you accounts will eventually bounce back no problem. The current slowdown on wallstreet actually provides investors with great buying opportunities.

The key, as you know, is to have a plan defined IN ADVANCE to keep your mind steady when there a tough months like January. Sounds like you are “staying the course” and will be fine!

Keep up the good work!

John

I get it that the drop is shocking, but the point is, you’re looking to win the war, not the battle, right? And you are doing an inspiring job of that!

Congrats on selling the house!

I’ve been a long time lurker…been reading your stuff for years! You were the first financial blog I consistently would read. Thanks for all the inspiration and NW updates!

Keep Hustlin!

Jay

Oh wow, that’s awesome! And now you have a $$ blog too – going over now to check out :)

Welcome to the solely renter’s club! Glad to hear you’re finally free of the looming mortgage!

Thank you sir! Renters unite! :)