[Hey guys! So I’ve been trying to get y’all a personal review of Empower (formerly Personal Capital) for ages ‘cuz they’re bad ass, but after finding out one of my friends lives and breathes by them almost daily, I thought you’d get a much better picture of how awesome they are from him so I asked him to write this Empower review. And considering he recently retired early at the ripe age of 33, he’s obviously doing something right ;)

Please welcome today, Justin from RootofGood.com! He’s been using Empower for over a year and a half, and has agreed to share real-life numbers & screenshots from his own account with us. Hope it helps!]

*************************************

I have a confession to make. I love spreadsheets. I run big chunks of my life using spreadsheets. I have an expense tracking spreadsheet, a net worth spreadsheet, and a portfolio analyzer spreadsheet.

They all do exactly what I want, but it takes a lot of time to keep them updated. My spreadsheets aren’t particularly attractive, either. And if there’s one thing the readers of this blog deserve, it is sexy financial management tools.

Enter Empower.

(formerly Personal Capital)

I stumbled into this amazing tool over a year ago and I find myself using it almost every day. You see, I have a bizarre obsession with optimizing all of the financial aspects of my life from spending to asset allocation. That’s how I landed a spot near the top of J Money’s Blogger Net Worth rankings at Rockstar Finance. Financial nerdcraft pays well as long as you have the right tools.

Free Financial Management Software

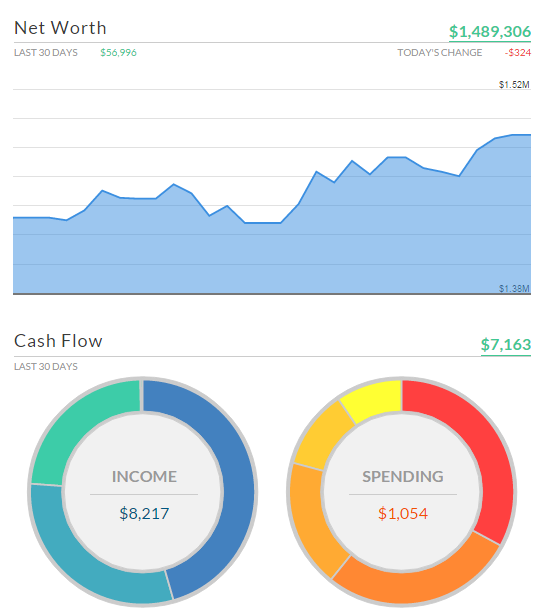

As soon as you log into Empower.com, you get an instant view of your net worth for the last 90 days and your monthly income and expenses on the Dashboard. It’s like having a CFO for your personal finances. Except this CFO doesn’t expect a seven figure salary with stock options – it’s free!

I grabbed a few screenshots from my own Empower account to show exactly what you get. I can see my net worth is tantalizingly close to $1.5 million and has climbed steadily the last month. My income for the last month was around $8,000 and my spending was only $1,054. Don’t worry, some months those figures are reversed.

The Dashboard keys me in to the large scale picture of where I’m at in recent history. Do I have a spending problem? Do I have an income problem? I like this high level summary because it makes it hard to ignore wasteful spending. The bottom line spending figure is right there in front of you every time you log in.

It’s like the annoying Post-It note you leave on the fridge door reminding you to eat healthy. The little orange and red spending circle clues you in to just how awesome (or horrible) your spending has been lately. It’s all automated and doesn’t require any configuration or tweaking. You simply log in and it’s there. Staring at you like a beacon of truth.

Track Your Net Worth

The Net Worth screen shows a graph of net worth for any time period you choose. All of your investment accounts, retirement accounts, savings and checking accounts, real estate and loans are automatically added together.

If you’re saving and investing like you should be, the net worth graph shows a line that rises toward the top right of the screen over time. It reinforces your good behavior.

In contrast, if you spend more than you make or deploy your assets in unproductive investments, you’ll see the net worth flat line or slope downward to the bottom right of the screen. That is totally un-sexy and you need to stay motivated to rectify that mess.

Even though I’m an early retired dude, I stay pretty busy. But I like to keep an eye on what we are spending (so I can stay an early retired dude!).

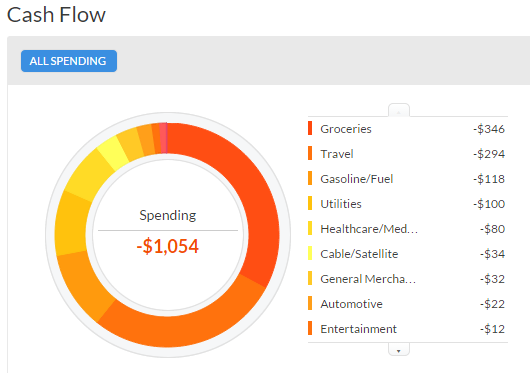

Expense Tracking

The expense tracking screen tells the narrative of my recent expenditures. The top three expenses are groceries, travel, and gas. Although sometimes it feels like it should be groceries, groceries, and groceries! Most days I’ll take a quick look at the expense tracking screen to see how we are doing in different categories and whether our spending is abnormally high in any area.

From my recent spending, I noticed restaurant spending doesn’t even show up in this list which is good for our waste lines and wallet. However the grocery expenses make up for dining out over the past month. I’m all about trading one type of expense for another type that brings us more value. In this case, it’s buying gourmet food at the grocery store instead of dining out.

By using a data driven approach to direct spending to the areas that bring us the most value, we get to live a more luxurious life without paying full price. It’s almost hard to call that frugality, but that’s exactly what it is.

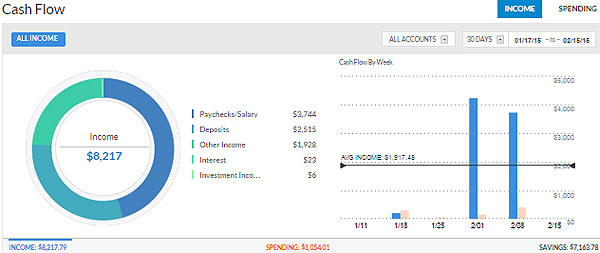

Income Tracking

Take a look at that income display! I have the awesome problem of multiple revenue streams complicating my monthly cash flow. The mix of income over the last month includes my wife’s paycheck, repayment of some personal loans, some revenue from my blog, and various interest and dividend payments from the investment portfolio.

With a quick click I can drill down to see the exact dividends paid on each investment and the exact amount of each loan payment or paycheck. This comes in really handy when I want to figure out how much income of a certain type I have received in the past year so I can forecast that into the next year. Embrace the power of data!

The cash flow tools show the income and expenses for each week on the right hand side of the screen. There’s no better way to get a quick overview of whether you’re making more than you’re spending.

Making Investment Management Cool

I’m a big fan of good Mexican food, hard hitting electronica music, and proper asset allocation. The first two make me cool while the latter makes me wealthy without taking on too much risk.

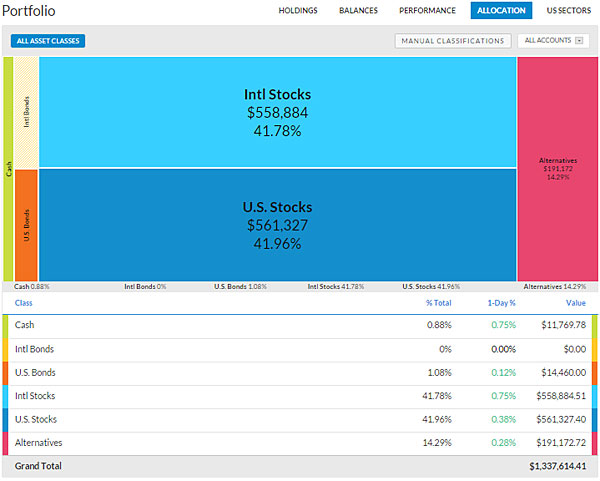

The asset allocation screen is a look under the hood of your portfolio. Your investments require a tune up from time to time, and this is the tool for it. The portfolio module in Empower queries all of your accounts and combines all stock, bond, mutual fund, and ETF holdings into one clean summary.

In my case, I’m holding roughly equal amounts of US and International stocks with smaller allocations to Alternatives, US Bonds, and Cash. Just like it should be.

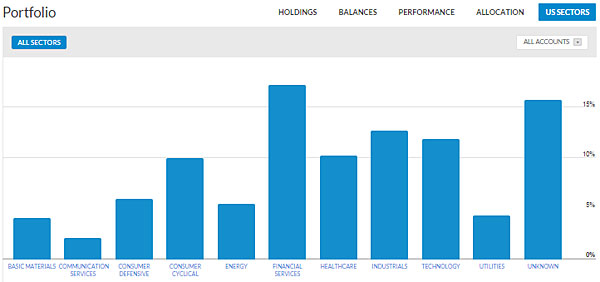

For those investors that want to concentrate their money in particular stock sectors, there’s a tool for that too.

My top three sectors are Financial Services, Industrials, and Technology. I don’t have any sector weightings in my own personal asset allocation, so I don’t really use this tool. But it’s good to see what I already own if I get an urge to buy a sector fund based on an expectation that one sector will outperform another sector.

I already have 10% of my stocks in the Healthcare sector, for example, simply by owning broad market index funds. Unless I have a really strong crystal ball telling me the Healthcare sector is about to outperform, I can rest assured that I’ll see decent investment returns with that 10% allocation to the healthcare sector already in my portfolio.

As I mentioned earlier, I love spreadsheets. I actually have an asset allocation spreadsheet where I analyze what I own and what I need to buy and sell to get me back to my desired asset allocation. I copy my aggregated portfolio holdings data from Empower and paste it into my custom spreadsheet. This saves me ten or fifteen minutes of logging into multiple brokerage firms and retirement account administrator sites to copy/paste current holding data into my awesome asset allocation spreadsheet.

Asset Allocation Tool

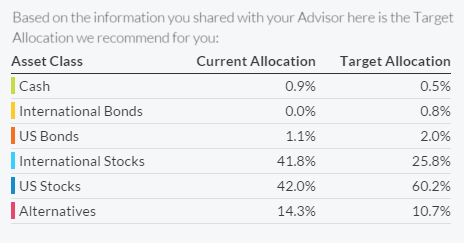

Those investors that don’t bask in their own financial nerddom like me can get an easy asset allocation tool in Empower.

This little beauty tells you how much of each asset class you hold in your portfolio and compares it to a target allocation built on the efficient frontier from modern portfolio theory. In a nutshell, the target allocations are keyed to maximize expected return based on a given level of risk. In general terms, if you can handle more risk, then your target asset allocation will have more stocks and a higher expected return.

This little beauty tells you how much of each asset class you hold in your portfolio and compares it to a target allocation built on the efficient frontier from modern portfolio theory. In a nutshell, the target allocations are keyed to maximize expected return based on a given level of risk. In general terms, if you can handle more risk, then your target asset allocation will have more stocks and a higher expected return.

The chart tells me I’m in roughly the right asset classes except for US and International stocks.

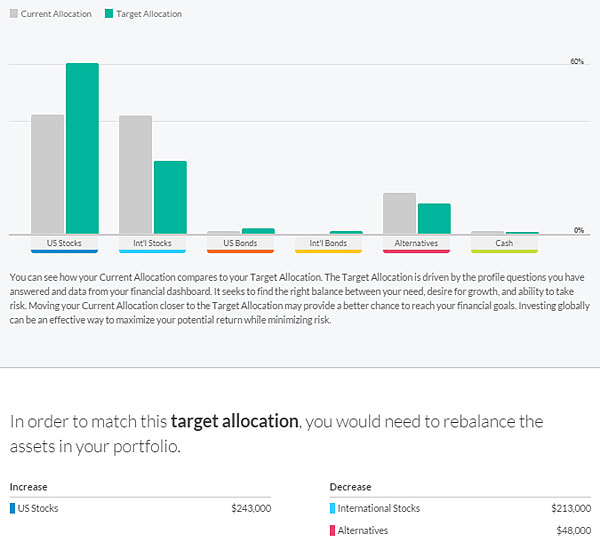

The investment management tools go beyond showing you actual vs target percentages. It also graphs those differences in a pretty bar chart AND tells you exactly how much to buy or sell of each asset class to reach your target asset allocation. Pretty nifty free investment advice customized to your portfolio.

The investment management tools go beyond showing you actual vs target percentages. It also graphs those differences in a pretty bar chart AND tells you exactly how much to buy or sell of each asset class to reach your target asset allocation. Pretty nifty free investment advice customized to your portfolio.

But wait, there’s more! Proper asset allocation will only get you half way to the goal of proper investment management. Focusing on investment fees is also critically important. And there’s a (free) tool for that too.

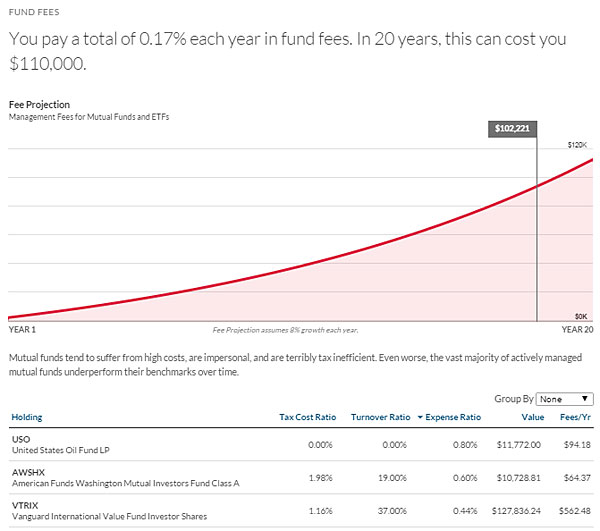

Investment Fee Tool

I can see I’m paying a total of 0.17% in mutual fund fees across my whole portfolio. That’s pretty good, but there’s always room for improvement. The funds with the most expensive management fees are listed first right underneath this graph. Those funds make the best candidates for cost cutting when making your portfolio more cost-effective.

The graph also proves how important mutual fund fees are over the long term. Even with modest fees of 0.17% per year, I’ll still lose $110,000 over the next 20 years. Maybe you’re much wealthier than me, but that’s a freaking ton of money.

Empower is Simple, Safe, and Free

I was pleasantly surprised at how easy it was to sign up for Empower and link all of my accounts. We have over 20 accounts spread across eight or nine brokerage firms, retirement plans, credit unions, and banks.

It took about 20 minutes to link all of those accounts and add a few credit cards and other assets and liabilities like my house and some loans. I was expecting serious compatibility issues due to the number of accounts I linked however all the accounts synced up seamlessly.

Empower logs into all my accounts so I don’t have to visit each site one at a time. They even link your home equity to the valuations provided by Zillow. Or you can choose a value yourself if you don’t trust Zillow.

[Editor’s Note: I am someone who doesn’t trust Zillow – those prices go all over the place! I prefer having a realtor pull comps and give me a much better estimate, though it’s harder to track over time unless you want to annoy the piss out of them ;)]

I haven’t used Mint for a long time, but the Empower tools do roughly the same thing on the expense tracking side but outperform on the investment side.

It’s like Mint on steroids, but with better portfolio management tools.

I still maintain a small fleet of spreadsheets but this is a great tool to see everything in one place and enjoy the beautiful graphics showing financial changes over time. My spreadsheets only get updated about once a quarter so I can’t rely on them for real time insights into my spending, income, net worth and investments.

To remain somewhat impartial, there are a few downsides to Empower. You’ll still have to look through your spending transactions to verify that they are categorized correctly, but the system gets it mostly right except for places like Walmart where you might buy clothing, groceries, and automotive supplies. There also isn’t a great way to enter cash transactions beyond categorizing ATM withdrawals.

[Editor’s Note: If you have a lot of money, they’ll also have one of their financial advisers call you every now and then. If you like that sorta stuff, then ignore this comment, but if you don’t (like me) make sure to tell them on the phone that you’re all good and prefer managing your money your own way behind a computer. You can try ignoring their calls if you want, but it doesn’t work – believe me ;) Suck it up once and just let them know you’re good unless you aren’t and prefer their help (which I’m sure is helpful!)]

In spite of those minor quibbles, Empower is still an incredibly useful tool to add to your personal finance arsenal. It’s all web based so you can check out your data wherever you are. Their iPhone and android apps are sleek and beautiful too, and they’ll also shoot you a weekly email letting you know how your money is doing.

Imagine having all of your expenses, income and investing data all in one place. You can quickly pull up how much you spent on entertainment last month (or last year!) or figure out your top dividend paying investment. They even have options to tag transactions to help you sort out your deductible expenses at tax time.

Overall, it’s a great app that can revamp how you run your financial life and doesn’t require a big time investment up front to get you going. And did I mention it was free?

You can learn more about them here: Empower

——-

Author Bio: At age 33 Justin retired from a career in civil engineering to spend more time with his family and pursue his other interests and hobbies. Justin founded RootofGood.com where he shares advice on reaching financial independence and enjoying the early retired life. Although Justin loves to travel, you’re just as likely to find him reclined in his hammock reading a good book or killing bad guys in whatever video or computer game he’s obsessed with at the moment.

PS: Do you think we should feature Justin in a future Early Retirement Series article? :)

PPS: As with most companies we review here, we get compensated when people sign up and try them out. But also just like all the reviews we do here, we only share those we love and trust.

Get blog posts automatically emailed to you!

Fellow Personal Capital fan here. We started using it a few months ago and are enjoying it. Anything that’s free and integrates all of our various accounts is a winner for us.

P.S. J. Money, I think you should definitely feature Justin in your early retirement series!

I think you should do a similar breakdown of your account so we can see all your numbers! Hah! :)

Hah! You wish! Someday…

I’ve been doing some serious research on Personal Capital, and it sounds GREAT! Thanks for the thorough review, Justin. One more reason for me to hop on board the Personal Capital train of awesomeness!

This real-life example is awesome. I love seeing all those zeros at the end of the numbers! I’ll be there one day, not too far away. I LOVE PERSONAL CAPITAL! I have been using it for a long time now and I check it all the time to keep track of my net worth, but mostly to keep track of my credit card purchases and to look for fraud. It’s great because all your transactions are in one place so it’s easy to review to see if there are any purchases that aren’t supposed to be there.

Great idea w/ monitoring of the activity like that. Much easier to do than having to log into a dozen accounts every time!

That’s what I do when I have a bad feeling some accounts have been compromised or after I get a fraud alert from the credit card company. My first stop is PC and not individual card issuers since I get a running list of transactions from all accounts.

Serious US-envy happening here! Personal Capital – if you are reading this – please come to New Zealand.

The investment fee tool to me is the reason why any investor should sign up for the service. All of the other great features are just icing on the cake.

Any I too dislike Zillow. At times the prices make sense while other times, not so much. I’ve given up on estimating the value for the time being.

That’s kind of how I feel about zillow. It’s just slightly more useful than the value our county tax assessor sticks on our property once every 8 years. I don’t use the auto-update figure from zillow in personal capital for that reason.

What a coincidence here J. Money! I’m a huge fan of PC and they changed my financial life with helping me get a hold of investment fees. Just today, I created a massive post pitting Mint.com against Personal Capital. It’s an incredibly detailed piece about both services and which one comes out on top, in my opinion! I find it funny we post posted something about them today. Thanks for sharing Justin’s story about PC! It’s nice to see others loving their service as much as I do!

Rock on! Pretty funny timing indeed – going over now to check it out (though I have a feeling of which will be coming out on top ;))

Like you, I have plenty of sheets that track 90% of what Personal Capital (PC) can do with a lot less labor. However, I just cannot bear the thought to give one application access to my every account due to security breach concerns. Just look at the headlines last week about a $1B bank breach at a major institution with highly staffed security and fraud departments dedicated to watch-dog-hacking. I’m certain PC has measures in place, but I don’t believe they have the resources to stay ahead of the trend and will eventually be low hanging fruit.

I come from the mindset, of stealth wealth. If they can’t find it, they can’t steal it. The risk of putting all account information in one place, no matter how secure anyone says it is, will keep me from seriously considering this tool.

respectively submitted.

True true true.

Something always good to keep in mind no matter what site you’re considering using online. Though, I’m pretty sure Personal Capital and other similar places just store the “handshake” and not your actual usernames and passwords, etc (which are only stored on the respective sites). So if they were to get hacked they wouldn’t have account info and just be able to see how much money you have and where (you can’t do any transactions through them, unless your investments are with Personal Capital). At least in theory :) Also, I could be wrong here haha…

I think there is a huge security concern here. If you have put your credentials in PC, then they do sit in a database somewhere and they do traverse the internet to the various banking sites, albeit encrypted.

The big thing I DON’T hear people talking about is the liability, or lack there of, if PC does get hacked. My money will disappear in minutes; and when I call Etrade, BoA, etc. to notify them, their response is likely ‘Oh, I see you freely gave your credentials to a 3rd party service, sorry sir, that voids your protection (FDIC and/or what ever the other protections are that banks have in place for their customers).

Not a risk anyone should take.

Information is more valuable than $ to hackers, and I’ll eat my hat if sites like PC aren’t being target every day. Its a matter of time and I’m not willing to give up the protection I have in place with my financial institutions.

I’d be interested to hear others thoughts around this.

My net worth is still under 100k, so I don’t get the calls, but I love the tool. Especially when it comes to churning my credit cards. I never worry about forgetting a stray balance I haven’t paid off yet. It’s sitting right in front of me.

Ahhhh is that the threshold for the calls? Interesting!

Awesome breakdown Justin, especially with the personal touch to it! I’ve been using PC for about a year now and there is just too much to like that it’s a no-brainer in my opinion. Like Jon pointed on above, the investment fee feature alone is worth using it. It can be horribly eye opening, but in a good way. I too learned that nicely telling the advisors that I was good helped stop the calls.

Do you use the app much at all, or do you just stick to using it from your PC? I just started using the app as well and love having it throughout the day when I want to look at something.

I’ll use the app maybe once a month. If I have 5 minutes waiting in line somewhere, I might pull up the app and check on month to date spending or make sure everything is categorized correctly. Otherwise, it’s probably 99% from my desktop since I’m not a huge smartphone user. I also don’t go to work so I can hop on the computer to play with my finances whenever I want.

The app is very clean too though, and quick and responsive the times I’ve used it.

I keep hearing more and more about Personal Capital so I’ll have to check them out!

Been meaning to check out Personal Capital, just need to carve out the time. Still rocking the spreadsheets myself. :)

The important part is that you’re tracking it all :)

I am a HUGE fan of Personal Capital. I don’t personally use it because I have a similar program that I run for my clients, but I recommend this over mint.com to people all the time.

I like using Personal Capital to keep track of the investments, net worth, etc. I don’t really touch the spending part, but that’s mostly because I track every dollar on my own spreadsheet. Thanks for having the details of PC, i’ll have to check it out more in depth this week.

I’m basically a Early Retirement junkie, if you don’t include Root of Good, I’m calling your people to complain.

So you’d be calling yourself? :)

I am absolutely obsessed with personal capitol as well. I am also a daily net worth checker as well :) personal capitol is a great way to check the total well being of all your financials with the click of a button it has totally replaced the use of my net worth spreadsheet and saved me about an hour of work a week.

I think Justin is a great candidate for the early retirement series!

That’s pretty powerful! Spreadsheets (esp net worth ones) are hard to give up! Haha…

This sounds like a great tool. Now I just have to find the time to check it out and get it all set up, haha.

This is a super-cool tool, thanks for introducing us to it.

Right now, I’m just using Mint for everything (really love it), but as I expand my investment strategy, I imagine it’d be awesome to have a tool like this tracking everything for me and showing me these cool, fancy reports.

How do you get to the fund fees? I use Personal Capital every day as well, but haven’t seen that one. Thanks!

Ha I just looked around and found it. I’m paying 0.07% over all of my investments. Yay that makes me feel great!

Super low! :)

Good review. Unfortunately, another thing to note is that they don’t yet have a connection with Tradeking, which is where I hold all my investment accounts outside my 401k, so I can’t get any value from the investment tools.

Well that stinks. Have you let them know that? Seems like they’d be a big one to connect with.

I have the bulk of my investments in TradeKing and still use it. You just have to manually enter the amount of shares you have. If you have many different stocks and trade frequently, this could be too much for you, but I just have 3 accounts with Tradeking and a total of under 10 investments. I do have to manually add new stock/funds when I buy something or receive a dividend. But it works for me.

Whoa.. Budgets Are Sexy meets Root of Good?! My two worlds are colliding in the best way possible.. ;)

I’ve signed up for PC, and subsequently deleted my account like 5 times running now. I get tempted by all the pretty graphics and monitoring in one place — but I am super picky with categorization and for some reason it felt like PC would categorize everything wrong for me. It just irked me so that’s why I stay away. I suppose I enjoy crunching my own numbers every month but I definitely don’t make such pretty graphics… compromise..

Justin — I see that you count repayment of personal loans as income. I’m curious why you do that? I have some personal loans out as well, and while I *do* put them under expenses/income in the month they occur, I don’t really factor it in my calculations when I think of monthly spend/gain. Though I guess if for some reason I don’t get repaid (possible but not likely), it will outgoing money as an “expense” that never turns into income again..

And yes, J. Money, you should totally feature Justin in your early retirement series!!

Ahhh, Tiffany, you didn’t know we knew each other? All of us money bloggers hang out all the time. :)

Good question on the repayment of loans. I actually went back and took that out of the “income” for the month (after creating these graphics!) since I didn’t count it as an expense when I loaned the money out. You’ll have to check out my monthly expense update next week for the 100% accurate version! ;)

I don’t pay as much attention to the income side of things since I can always sell another chunk of stock if I need more cash. I suppose I would have to write it off as an “expense” if the borrower defaulted.

Thanks for the detailed review! As I get more accounts I’ll definitely look into setting up an account with PC. Right now I have so few accounts, that my own spreadsheets work wonders without a huge time commitment.

Definitely feature Justin in the early retirement series! As a 24 year old civil engineer, I would love to read about his story! That made me excited to see that he used to be a civil engineer as well (makes the dream of early retirement seem so much more realistic!)

Duly noted ;)

I signed up an account a while ago but didn’t spend any time with it. Need to figure out whether Personal Capital supports us Canadians or not. Haven’t been able to get an answer anywhere…

I just did some searching around and I don’t believe it’s compatible for Canadians – unless you’re a baller and having accounts set up in the US? :)

D’oh! So disappointed that we Canadians get shafted once again from such awesome services. :(

Sounds like a great (and free) tool. I’ve been using Quicken for a long time. It doesn’t quite have all the functionality and requires updating every few years to link to accounts. However, I do have 20 years of historical data. Hard to pass that up. I assume PC starts when you sign on and won’t have that history, right?

I think you’re right. From what I’ve seen, they import about 90 days of account history and then update it going forward. Now is a great time to start though so you can get all of 2015’s data in there so by year end you’ll have a full 12 months of data and not a partial year.

I didn’t mention this in the main summary, but looking at year over year trends is easy with PC once you get that history built up. And I think that’s where people’s finances slip up – they slowly drift into higher spending over time so gradually that they don’t realize they have expanded their lifestyle.

I’d love to sign up to Personal Capital, but doesn’t seem like they’ve expanded their shores as far as Australia yet unfortunately. The best we have here is ‘Pocketbook’, but it’s nowhere near as sophisticated as Personal Capital. Fortunately I’m all over the spreadsheets myself, so I can still analyse some of this stuff, but would be awesome to have something much more streamlined online to use (and I know it would tell me my portfolio is waaaay too risky :) )

I’ve got to say, I’m really enjoying the way this app is seeming to lay out everything plainly for me. With graphs! And charts! I can visualize my money in a way I just can’t do in a lot of other personal finance apps. Thanks so much for sharing this!

It’s the graphs that really seals the deal – brilliant thing for them to focus on :)

I have personal capital too, but haven’t used it much as I love my spreadsheets!

Thanks for the post, I need to look back into it. And yes, I would love to see Justin featured in the future, he is good people!

Started using PC after I stumbled across it last month. Only thing I dont like is I can’t manually import balances to true up to the start of 2015. I have a 1/17 start date and added my 401(k) a week ago so the numbers are all over the place.

This is a great tool from what I read all over the web. IT seems like they are providing great value for many investor junkies. I have to jump on the bandwagon. Thanks for the review.

Great Review. I signed up for a Personal Capital account recently but have not spent much time exploring it. I did get my first call you talked about and told them that I would reach back out to them if I thought I needed help managing my money.

I was trying to be as polite as I could.

It will be hard for me to switch since I have pretty much been using mint from the beginning. But it would be nice to be able to pull some of the visualizations from Personal Capital.

Cheers!

Haha yeah… small price to pay since they give us access to it all FOR FREE! :)

Maybe you can connect up PC to run in the background and then eventually move over once a lot of data is over there or you find it’s more helpful? Would suck to lose all that data for sure (not that you’d lose it, lose it, but that it’s separated out)

One of the best reviews I’ve seen. I’ve been using PC for almost 2 years and really find it useful. There’s so much information there so you can easily find out where you need to change some things.

So glad you liked it! Even more so since you’ve been a user of it for a while – thanks for chiming in :)

I’ve been using Mint for about 7 years now, so the amount of data and categorization and tags I have in that account makes me hesitant to fully switch, but Personal Capital seems really awesome – especially all the investment stuff. That’s definitely one area where Mint is lacking!

I am starting to love using spreadsheets because it can really make me focus on my cash flow, expenses, and savings. The use of graph can really give me the real scenario of my status. Yay! I agree with you J, it’s hard to update every spreadsheet. I wish there’s an app that can do it automatically. That would be great.

I have never heard of personal capital until this post and I’m considering looking into it, I have tried both mint and Learnvest, both of which seem to have issues with refreshing accounts because of validation (Security questions, etc.) Have you had issues with accounts not updating because of this with Personal Capital? This is the reason I left both Learnvest and Mint, the accounts were never accurate and I had to reauthenticate each account once a week at least.

Hey Bradley!

Great question. I haven’t had any real problems with account validation requests at Personal Capital. There might be one account once a week or once per month that I have to “reconnect” or “revalidate” (the account has a red exclamation point next to it if it requires revalidation) but normally clicking refresh will do the trick. Very rarely Personal Capital will require me to input the answer to my security questions at my bank or investment firm.

Definitely not a big problem that takes more than 30 seconds once per month. I have a couple dozen accounts linked FYI.

Awesome article! I now need to find the time to check out this service. Even though I worry about security and having all of my accounts linked in one place PC would definitely make it easier for me to track my net worth and view how well my investments are making out.

Thanks for the info! Love the personal touch.

Yeah, that is a level of comfort that some people aren’t willing to give up. I figure these days almost EVERYTHING is done online, and especially with money, so my stuff is already out there and adding one more won’t make a difference – hah. Especially if you have a good bank who has your back when fraud and the like occur. USAA has always caught any nonsense from scammers on my end which I’m more than appreciative of.

Does anyone have any idea how I could access Personal Capital from Australia?

Personal Capital only works for U.S. accounts :( Here’s a note from their support:

“Although you can access the Personal Capital application from any location, we currently only support U.S based financial institutions (currency, USD) for linking accounts. Note that to sign up for Personal Capital, you will need a valid U.S. phone number for security reasons.”

Personal Capital is so popular. Just about every PF blogger gushes about it. Are there any other opinions? (I see a comment from Franklin above with some good points.)

How can I say… It is nice that there is something that people like so much, that is so popular, that I have been unable to find any reviews that have anything non-wonderful to say… (“If it sounds too good to be true…”)

So I will say it. I have reservations. Not that Personal Capital isn’t a great tool. It is. But there must be considerations otherwise.

Not meaning to bash Personal Capital or any similar sites. I am sure the people there aim to do a great job. But the data you give them is your data, it is your complete financial life.

Yup – they’re def. not for everyone :) In fact, I use old school spreadsheets still, but only because I like the more hands-on approach than automated (the #’s feel more real to me that way). That being said, most of society can’t stand dealing with their finances, so being able to see all your money in one place like this is great! Whether with Personal Capital, Mint, Clarity Money, or even just your online bank… And these days, most of our financial data is already scattered around everywhere so for most of us it’s too late :)

I’ll check our Personal Capital. this is the 3rd time I’ve heard someone talk to the wonders of it.

I’m a self spreadsheet kinda gal. Do you know if Personal Capital allows you to track numerous rentals with the mortgages, income received and expenses associated with the rentals?

Hi Pamela,

You could certainly track the rentals. Each rental could be input as an asset, and in fact you can set it to update the value in real time based on Zillow value (or keep it simple and leave it as a static value YOU control/update :) ). Then link the mortgages. Then you can create custom income and expense categories (rental income/rental expense or rental 1 income / rental 1 expense, rental 2 income, rental 2 expense…).

You could probably set everything up in 30-60 minutes and then it’s just a matter of a few minutes per month to click and categorize the expenses to the right category/property(ies). And the system has smart categorization, so once you categorize a vendor/payment a certain way it’ll default to that category in the future (which you have to keep an eye on because sometimes Walmart is a grocery expense, sometimes home maintenance, sometimes might be a rental expense, sometimes gift, etc).

I’ve started using personal capital again. I don’t like their budgeting system (income and expense) categorization so much, but I do use it. The downsides to the income and expense is that I tend to have to re-categorize a lot of transactions. The biggest one for me is that most of my transfers get recorded as deposits. This is because of the way Capital One 360 calls the transaction “Deposit from Account ####”. The web interface for this is a little slow for my liking, so it feels like too much of a chore to keep up on.

As to the phone calls, I did bite the bullet and allow them to manage a portion (~$120k) of my assets. Personal Capital uses Pershing to hold managed assets. The fee for management is 0.89% of managed assets and drops as assets increase. Their philosophy is to have a more balanced sector holding than market index funds tend to have and are invested in low cost (and no load) ETF’s. My investments are almost entirely in Vanguard funds with them.

Their team also works with you on other financial aspects, for which they do not have any products to offer, as part of their fiduciary philosophy. They have done an insurance review, legal entity review, 401k review, and estate review for me.

Hey, thanks for the insight man! Super interesting to hear, appreciate that.

Just signed up today, sorry it took me so long. I like the graphics, however, I am having trouble linking. My bank sent code via text, entered it and still it won’t link. Same with a credit card I attempted. Checked and updated all logins and passwords to be certain they were all accurate. Not sure how to resolve the issue. Anyone else have this problem? Also, would like to set up a short term goal for saving, not just my investments based on a retirement date. Does that exist within the program or am I just missing it?

Once again another nice review J Money, I appreciate that my dude! I also read your millionaire to do list, very good read and recommend it to others. Peace!