[Happy Friday! Today’s weekly guest post comes from Owen of PlanEasy.ca – a financial planner and geek of all things personal finance. Do you fall into any these bias traps Owen shares today?!]

******

If you’re a personal finance geek like me, you probably check your money on a regular basis. Whether that’s weekly, daily or even multiple times per day.

Maybe you check your investments, or the stock market, your checking/savings account, credit card balances, mortgage balance, or maybe you even check them all. And financial apps and aggregators only make it easier any second of the day.

But beware, checking your money every day could be making you sad!

Why? Because we’re not rational people. We experience gains differently than we experience losses, even when it’s the exact same dollar amount. This is called “negativity bias” and if you check your finances too often it can actually hurt you more so than help you.

Let me explain…

We’re Not Rational And It Makes Economists Cringe

Economists assume that people behave rationally. For a given situation we should be choosing the option that provides us with the most benefit. But that’s not what we actually do.

For example, we perceive information differently depending on how it’s presented, which is something called framing bias. If we look back at events and believe that they should have been predictable, then we experience hindsight bias. And if you’re somebody who’s always trying to avoid loss, that gets filed under loss aversion.

We’re affected by all sorts of deep, ingrained biases, and each of these affect not only our behavior, but our mood too.

We also don’t perceive gain and loss the same way. Which is something called negativity bias. For the same amount of money, we’re affected by losses more so than gains.

“The aggravation that one experiences in losing a sum of money appears to be greater than the pleasure associated with gaining the same amount.”

– Kahneman & Tversky

What does that mean for your personal finances?

It means that if you unexpectedly gain $100 one day and then unexpectedly lose $100 the next, you’ll end up feeling sad. Even though you’re in the exact same financial position you were two days ago.

[Editor’s Note: Remember our post on how I’d scoop up poop if it made me happy? And how I mentioned how horrible it would be if you gained a lot of money, only to lose it all later even though you’d be back in the exact same position again? Guess that’s textbook negativity bias!]

The same thing happens when you gain 1% in the stock market and then lose 1% the next day. You’re roughly in the same financial position but you still feel the pain.

So Why Do We Keep Looking At Our Investments?!?

I just read this book called Fooled By Randomness by Nassim Nicholas Taleb. One of the central ideas in his book is that we are terrible at separating noise from signal. Humans seek patterns, even when nothing is there. We want to assign meaning to things even when it’s just randomness.

When it comes to the stock market, his point is that day to day, hour to hour, minute to minute, the stock market is mostly noise. It’s speculators making bets on the direction of stock prices based on external factors.

From minute to minute there is little meaning in stock market fluctuations. There is no appreciable change in information for any given company listed on the stock exchange. Yet, its stock price will fluctuate throughout the day. Up, down, up, down, up, down…

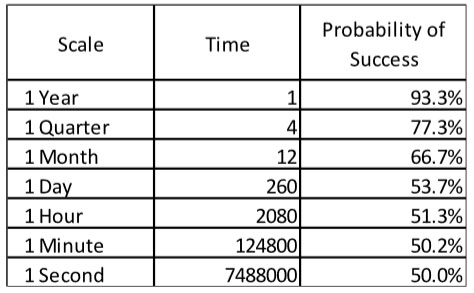

Taleb provides an example: he calculates the chance of a fictional stock gaining when it has an annual growth of 15% and standard deviation of 10% (standard deviation is a measure of the price fluctuations).

If you own this stock you only have a 53.1% chance of seeing it gain on any given day. The other 46.9% of the time you’ll see it lose. This is just noise.

However, over time this noise gets overcome by actual results. Over a long enough period, the noise is barely noticeable at all. This is why we invest for the long term.

If you check this stock on a quarterly basis you’ll have a 77.4% chance of seeing it gain that quarter.

It’s even better annually. If you only check this stock once per year you’ll have a 93.3% chance of seeing it gain, almost 19 times out of 20 you’ll have a positive year. That would feel pretty good!

(Fooled By Randomness, page 57)

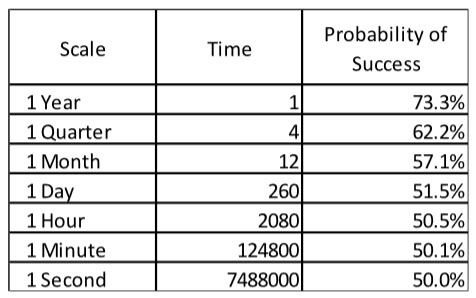

Just for fun I recreated Taleb’s table with the actual results of the S&P 500 over the last 30 years. The compound annual growth rate, including dividends, is 10.5% and the standard deviation is 16.8%.

The probability of seeing the S&P 500 gain over one day is just 51.5%. Over a quarter it’s 62.2%. Over one year you have a 73.3% chance of seeing the S&P 500 gain.

If you checked the S&P 500 daily you’d lose money nearly half the time!

Remember! From one day to the next the stock market is mostly noise. But from one year to the next you start to see actual results.

By checking your money every day, you open yourself up to these sad feelings.

One day your net worth is up, the next day it’s down, and now you feel sad. Nothing has really changed in the market. It’s just random fluctuations. So why do we torture ourselves? Why do we look?

In the past this wasn’t a big problem. You got your quarterly account statement from your stock broker in the mail and most times you’d be up.

But in the age of financial apps and instant information, it’s easy to get your net worth updated by the second, and that can be dangerous.

But Does It Really Matter?

The question is, does this really matter for you?!? Probably not. Because hopefully you’re still making contributions to your savings and investments on a regular basis.

Unless you’re super wealthy, my guess is that your contributions are still larger than those daily fluctuations. Thanks to these contributions, when you check your net worth you’ll see it growing and this can be super motivating. As a financial geek, I get really excited when I see my net worth grow or when dividends come rolling in. This excitement is a very powerful motivator.

When should you stop checking your money? Probably when the daily fluctuations start to overcome your contributions. At this point it might makes sense to check your money less frequently. Maybe once per quarter or even once per year. This should help avoid those “sad” feelings.

Until then, keep checking your money, just be aware of this psychological trap!

Editor’s Note: How often do you all check your accounts? I used to log into my banking EVERY SINGLE DAY because I was obsessed, but now I tend to only look a few times a month just to make sure everything’s kosher. Investments-wise, however, I only check in *once* per month when I sit down to calculate my latest net worth. Which, come to think of it, is probably why I’m always happy each time I run it – the odds are always in my favor! Haha… Yay stats!

******

Owen is an avid traveler, father, and creator of PlanEasy Inc. – a financial planning company and blog sharing weekly tips around personal finance. Find him on Twitter @PlanEasyCanada, or in person the next time you’re in London, Ontario!

[Shameless plug: If this post hasn’t scared you away from $$$ apps, check out our new Directory we just built out over at Rockstar Finance ;) We feature over 50 of the most popular and best $$$ apps, as rated by 150 financial bloggers!]

Get blog posts automatically emailed to you!

Yes, it can def drive you crazy if you check every day/too often. SRGO came up with a perfect term for those who check too often: “Helicopter Investors”. And I came with the opposite term for those of us who only check a few times a year:”Free range Investors”.

But I have a feeling that once we payoff the mortgage and start redirecting the extra $80-$100K/year to investments, we will turn into helicopter investors. God help us :-)

Ha. That’s the first time I’ve heard the term “helicopter investor” but I think it’s an apt description.

We check our investments every four months. We do a financial “check-in”. We order takeout and talk about our personal finances. It’s kinda fun!

I tend to be an obsessive about a lot of things. If I’m super interested in it, I’ll check it a million times a day and get frustrated all day because it’s not doing what I want as fast as I want it to.

Luckily, my husband is the main one who checks our finances. I like to be up to date on everything a few times a month, but he’s a daily checker for all our finances. I do think the joy of all the hard work is gone when you study each little change, versus seeing it as the big picture.

You’re right Ember, by checking too often you never see those big changes. It loses some of the impact that way.

For new investors I think twice per month is good, assuming you make contributions with each paycheck (which you should!), then every time you check your almost guaranteed to see an increase.

Before I started blogging, I would check Mint every day. It didn’t necessarily make me sad, but it was a useless task.

Now, I’ll check in 1-2x per week to see about a specific account balance and to double check credit card transactions, but I only look at the overall picture once per month (net worth update day!)

That’s another great point Mrs. Adventure Rich, the time.

Even checking a few times per day will add up over the course of a week.

I remember when I started blogging I would check Adsense 10x per day (I don’t know why, it was basically pennies). I estimated that I was wasting about 30min each day just checking Adsense.

Haha… I still do the same thing, but with my stats. Even though 99 times out of 100 nothing crazy is going on :)

Checking our money daily is definitely something I try very hard not to do. Unfortunately, I tend to often fail miserably. You’re so right, I feel like a loss of a few dollars makes me sad, even if it was preceded by a gain of more than $100. It’s totally irrational.

But like you mentioned, were adding significant amount to our investments on a regular basis which keeps our net worth climbing, despite the various losses.

Thanks for pointing this out. I’m going to make a plan (and try to stick to it) to stop being a checker. ;)

It’s hard to avoid those sad feelings!

For those of us still adding to our investments I think a plan to check once per month is the perfect timing. With your monthly contributions you’re almost guaranteed to be up for the month, and this feels great.

Yes. Some days it makes me sad, but lately we’ve been on such an upswing I’m worried I’m getting too used to the up-slope trend. Expectations? Watch out. The same is true with our real estate portfolio – home values are on a crazy surge since 2013. Brace thyself…

Yes!!! Lately that positive feedback loop has been very addicting. It’s tough not not get excited when you see gains 9 days out of 10. Statistically I think they’d call that an outlier though.

I check everyday.

Yes, it’s probably far too often.

But: (A) it keeps me on top of things, (B) offers a daily reminder to forego indulgences that I don’t really need to keep my net worth growing, and (C) since I’m looking at a spreadsheet that now goes back to April 2014, I can see the growth so I’m less discouraged by daily/weekly (or even monthly for that matter) declines caused by the “random noise” — I know this works over the long term because I can SEE it’s worked over the long term.

Hi Chadnudj! If the reminder helps you stay on track with your finances then by all means check daily. Just watch out for those sad feelings, it’s not rational, but they still happen.

I’m on #TeamTenTimesDaily but as you pointed out, that’s because I’m still in the part of my journey where my contributions matter a whole lot more than any gains/losses I might experience.

Having said that, I checked Personal Capital while in my car last night (at a red light) and did a little happy dance when I saw I clicked over $200k Net Worth, just 16 months and 9 days after hitting $100k. Checking 10 times daily is super motivating to me.

Go Team!

Checking often can be super motivating, I agree. As long as it makes you feel good I say go for it!

Nice! Congrats!! The first years of learning/tracking this stuff is the best :)

Wow, I’ll have to check out that book. I try to limit myself to checking the first of each month, it’s really hard though when you see the news headlines…..maybe why a certain mustachian advises to limit your news intake?? Haha. I can see where checking just annually would be beneficial but very difficult for me to do.

It’s an interesting read, I would recommend it. Taleb can be a bit hard to follow sometimes though.

Yeah – I had to unsubscribe from following his tweets cuz I just felt really DUMB not understanding him 99% of the time haha…

I do check my accounts regularly. Partially, because I want to see if my money is performing or not. The other part is to check that everything is correct and I am not being charged for services that I did not sign up for.

In recent light of the EQuifax fiasco, I want to be vigilant and to make sure that my identity is protected and there are no unauthorized access to my accounts.

In a way I do agree that once the fluctuations of your account on a daily basis is higher than your regular contribution, it makes it meaningless to check you net worth on a regular basis. I now resort to only doing it once a quarter.

Looking out for fraudulent charges is a good practice. Usually banks give you at least 30 days to dispute any charges.

I don’t check my money every day since I know it’s going to be the same. And there’s no investment or financial opportunity that I know of is going to take us to the next level overnight. It takes time to build wealth.

I go, however, check my blog traffic constantly every day hoping that there will somehow be a magical spike and gets really sad when there is a dip. I guess that’s how some people feel about checking their money every day too.

Ms. Frugal Asian Finance I feel your pain! I also check my blog stats waaaaay to often. I think your site is great though, so keep up the good work and don’t let those stats get you down.

OK, I’ll admit it – I check my account everyday.

I use Mint to track spending and investments, so I check my transactions everyday in Mint to make certain nothing hinky is happening. I can’t help but accidentally see my investments and net worth. :)

It’s ok! I admit, I catch myself doing it too sometimes.

Same here – I just use Personal Capital.

Getting a daily email recap helps to identify any issues. A few years ago, I didn’t check and it took nearly 3 days to realize I had $500+ of fraudulent charges on my Amex (although their fraud team shut down the card after a particular attempt to buy a whole lot of booze).

That’s the downside to not checking daily, yup… You’d prob be good just looking at banking/checking accounts regularly, as long as you can ignore the *stock* accounts which is usually what gets you :)

This is a great post! I love the detailed analysis and background. I tend to check my numbers daily, mostly because that’s what I do when I focus on goals. But I only check on days when the S&P 500 is up. Gives me a little boost in motivation. Like you said the contributions are flowing anyway.

Great point by FrugalAsianFinance too. I check my blog traffic to much. I should think of a little hack, maybe check only on post days. The posts will keep coming anyway.

Thanks Handy Millennial. I like the idea of only checking your net worth on days the market is up.

Every day… Its dumb I know. But I got rid of Mint and only look at personal capital now. I don’t really budget anymore as it wasn’t good for my psyche. Day 1 of getting paid when my account is plump, I just put everything I need to in my investment accounts. Then I know what I have to play with each month. I hated spending categories with a passion, I know how much we normally spend so I leave an additional $500 buffer and it seems to work out. Could I dial in my spending a little more, sure, I didn’t need to buy all 9 seasons of Dragon Ball Z on Blu ray, but you know what, I don’t really care. My investment first approach has been working and now I don’t have to stress if my wife brings home some Wegman’s sushi every now and then.

I do this too! I’ve read that it’s called reverse budgeting. Pay yourself first and live on the rest. I’ve been doing it for years, it just feels more natural to me.

Nice post. I try to focus on slowing down and making effective decisions to get past these biases. Right now I only update my net worth spreadsheet twice a year. I guess I see the numbers more often due to aggregators. I look at those just like a halftime score and I don’t get too worked up about them.

Thats a good way to look at it Jason. Its only halftime, the games not over yet, time for a pep talk, get those stocks moving in the right direction!

Thanks for your comment!

I like that “halftime” thinking :)

I glance at my investment almost everyday. However, I don’t pay much attention to the fluctuation. It doesn’t affect me anymore after 20 years of doing so.

The only time I feel something is when I update my spreadsheet, once per month. That’s when I see how the price fluctuation changes my net worth. It’s not a big deal to glance at the market.

This is a good point Joe.

I also check my investments daily just to see what’s going on in the market but I only calculate my net worth every 4 months (Jan, May, Sept).

The longer I’ve been in the market the less I watch. When I first started I checked daily. Now I only check 1-2x/month, and some of those times are because I am using Mint or Personal Capital to check overall spending.

It also helps that while we are doing a good job saving, we are nowhere near retirement. I imagine as that time approaches (TBD) I’ll have more interest in the daily fluctuations of the market, as it will directly how I spend.

I call that the “auto pilot” phase. You’ve got your system setup and you don’t need to check-in quite as often.

We’re sort of in the same phase, we’re doing a ‘financial review’ every 4 months now. January, May and September. We keep and eye on the markets in-between but we don’t actually check our net worth until the review.

For me I believe it’s important to check every day just to make sure that everything looks proper. If you wait even a few days and there are fraudulent charges or withdrawls, this could add extra hassle to your attempt to recover your money. Plus, the closer I am to reviewing my transactions to when they actually happened, the more apt I am to remember everything. I mean, we’ve all had those times when you look at a charge and you can’t, for the life of you, remember what it was for. Even if it’s legit, it drives you nuts until you figure it out. I think those instances happen more often the further you go between checking your money.

As far as it making me sad, well yes, there are certainly some days where that happens. However, there are days when checking it makes me feel good if I like what I’m seeing. That’s just like life, some ups and some downs.

Yeah – much easier to catch issues checking regularly like that for sure.

I fully admit that I check my personal capital account two times a day. ONce in the morning to determine what expenses have gone through and then in the evening if the market has gained to see if my net worth has grown. I admit it does make me a bit sad when it goes down, but i haven’t done anything about changing anything.

I used to check accounts all the time when I was just starting out. As I grew wealthier I started to care a lot less. Whether I had $1.01 million or $1.04 million on a particular day is mostly irrelevant since I’m earning only thousands per month and making spending decisions on $1, $5, $100 type things on a routine basis.

Now that I’m closing in on $2 million, I check even less! And that’s in spite of being a FIRE/PF blogger! Just doesn’t cross my mind to check on things routinely since I know I have enough whether the number is $1.4 or $2.0 million.

Interesting! I do enjoy the monthly updates you do on your blog, please don’t stop :)

Interesting post, J.Owen brings up an important point. I personally do NOT check my money often. Sure, I balance the checkbook and such, but counting my net worth constantly? No way! I have a life to live.

I encourage my clients to NOT check their money too often. When people play with their money too much they start wanting to PLAY with their money, as in trading. That always ends in tears.

This is important work and I hope plenty of folks see this. Having money can make you unhappy if all you do all day is sit around counting it.

I agree with you Wealthy Accountant. Checking too often gives you that urge to “tinker” with your portfolio. Best thing to do is set it and forget it.

Great post. I broke this bad habit years ago. I once read that you do not have your house appraised every day, so why look at the value of your stocks everyday? That made sense to me. I check my total asset allocation twice per year. If my allocation is off, I buy low and sell high. Looking at it everyday can only lead to emotional decisions. To succeed as an investor it is important to keep your intellect ahead of your emotions (i/e).

Absolutely Dave, if you have a diversified portfolio there is absolutely no need to check daily.

I’ve gotten a lot better on checking my accounts now that I’ve got systems in place to run most of my finances on auto pilot. The big thing for me now is just going through the motions and letting the market do its thing.

Losses suck but unless I cash out, it’s just paper losses.

We’re also in the “auto pilot” phase. We’ve been managing our budget/spending fairly tightly for a while, now it just feels natural. I still catch myself logging into my online banking a bit too often though. Can’t resist the urge sometimes.

I check my investments once a day during weekdays. It’s a habit I’ve formed – my ETFs are around $98,000 and I want to see them hit the $100,000 mark. It’s been fun to watch them climb, but if a big drop happens, I’ll probably change to once a month or less. I’m in for the long term and only rebalance once a year so it’s easier to handle drops by burying my head in the sand.

That’s a huge milestone, congratulations!

I totally agree, it can be really fun to watch your investments climb, and lately the markets have been on a pretty good streak.

Congrats! The first $100,000 is the hardest!

https://budgetsaresexy.com/the-first-100-thousand-is-the-hardest/

I think checking financial balances should be done about as often as checking weight. Too often and you are not motivated by the slow changes. Too infrequently and you don’t have time to make necessary course corrections. Way too infrequently and you wake up one day broke and out of shape (trust me; I’ve been there!).

Thanks for the comment Jason, you’re right about the slow/small changes, checking every day kinda takes the “wow!” factor out of checking your net worth.

Oh lawd, no. I think looking at any kind of report daily doesn’t do you much good. I work in marketing/SEO and this is something I struggle with when educating my clients. They think going down in rank one week is the end of the world; they don’t see that there are long-term trends. The long-term is our focus, not the short-term.

That reminds me of my last job. Daily reports were a big thing. Most people had email filters that put them into a folder every day. Not very effective.

I check my investment portfolio 5-times a week only when we’re in a bull market. For me, it’s a source of entertainment. I’ve learned not to be fearful when the market drops. Not sure about being sad though. If I were 65 and had no retirement savings, maybe. Sadness is a totally different feeling altogether. It stems from the feeling of hopelessness.

During bear markets, like that of 2009, I do not bother checking my investment portfolio knowing that I’m already well diversified. Nothing good will arise checking your portfolio on a daily basis on a downturn. You’ll be your own worst enemy if you let your emotions get the best of you.

Because of the renovations and majillion expenses involved, I got back into the habit of checking my bank accounts every day to see what’s been cashed or withdrawn to update my spreadsheet. I find that the depression that resulted was only because money was leaving the account as expected, and that was purely temporary because at least the project (and related spending) had an end date. XD

The nice thing about knowing that you have a long horizon and a plan is that the frequency with which I check my accounts (like a nervous twitch some days) has no impact on what I do. The plan tells me what I’m going to do, not my reaction to anything. But I’m also not an nervous investor. I check my taxable brokerage account several times a month because it’s at Ally and right at the top of my screen when I go look at my savings but I don’t care about the stocks’ ups and downs. Or more accurately, as a buy and hold dividend investor, I don’t care much about how my individual stocks are performing unless I see them all bleeding red, then I go check to see if any of my Buy list is on sale :) Our retirement accounts don’t have any impact on my day to day life, I only check them for my monthly updates and since they’re not meant to be used for another 30+ years, I don’t worry about which way they’re going on any given day.

I’m on more of a once a month or less look. Much of that is due to the reason you mentioned but some of it also is because I find no actionable reason to do so. My money invests automatically and I’m not near retirement so up or down this week makes no difference. I do have to wonder if it would be harder to resist if I were retired and it was my primary income source.

Good question! I generally have no actionable reason to look at my investments either, other than possibly buying but that’s not often. I’d probably log in daily if I were retired just because I LIKE looking at the numbers but there wouldn’t be much reason to do anything then either.

Thats a great attitude Revanche! I try to not let it affect me but I find it easier to just put my head in the sand (so to speak) and check every 4 months. In-between I follow the market but I won’t check our total net worth.

Gotta do what works for you! :)

Very cool concept Owen. I myself tend not to get too worried about the day to day but do need to admit as a MINT user I am checking everyday. That being said I probably check every day more so to monitor our credit cards as we use them for business transactions for our retail stores.

The bonus to this post is finding another cool Canuck financial blogger :)

Hi Chris, thanks for the comment, I’m definitely going to follow you, you’ve got some fantastic photographs on your site!

I manually calculate my net worth once a month so I only EVERYTHING once a month. I definitely watch my checking account daily because it changes and I like to know exactly where I am. I check some of my balances a few times a month because we are trying to pay some things off and I love to watch those numbers go down. I’m pretty okay with fluctuation in long-term accounts.

Great article.

Richard Thaler won the Nobel Prize in Economic Sciences recently for his work in making retirement plans auto-enrolled for employees. Understanding Behavioral Economics and the impact it can make on decision making is a huge, huge part of potential financial success.

YES!!! Auto-enrolling is so smart too as people are too lazy to change it!! :)

Absolutely. Personal finance is half numbers and half behavior.

Great post as usual!

This can definitely be a trap especially when you trade cryptocurrency and want to refresh your app 100 times a day.

Why can we just leave these alone and enjoy life more, especially if they are long term investments?

I used to check my brokerage account multiple times a day. I forced myself to now only check once a month, for the sake of entering our net worth in my spreadsheet.

It’s hard not to check. I still check market news daily I guess, so I’m still sad a lot

Once a month is good. From my perspective checking the market is ok, as long as you’re not seeing a net worth number or investment total.

I check market accounts (HSA and retirement) daily. Yeah, sometimes it’s no fun when things drop, at least until I remember I’m buying on sale and that’s great.

But here’s how I get around it: I’ve factored in estimated retirement balances for the next thirteen years, assuming $30k/yr contributions and 7% interest. Those estimates suggest a thirteen-year horizon will work out well; the figures are predicted annually and tallied in the column next to our ACTUAL January 1 retirement balances.

Through a combination of market performance and higher contributions, actual balances have blown estimated balances clear outta the water. So if I notice I’m down over the last week or month, but realize I’m still up $16k over where I expect to be in early 2018, that feels pretty daggum good.

That’s the power of tracking it, baby! You can easily compare and see how far you’ve come! :)

I don’t check everyday, but do check once every couple of weeks or even monthly – just to make sure things are flowing in and out the way they should be. Fortunately (or unfortunately depends how you think I guess), my money, investments, and portfolios do not go through huge swings so I am comfortable that things won’t change too significantly for me to worry about it daily.

Yes! I agree James! With a well diversified portfolio you don’t need to worry about it daily. If someone feels the urge to “tinker” with their investments daily then they’re doing it wrong. Long term investors don’t need to watch the market daily.

While I’m still in the learning phase, I find checking things to be useful to me. So I see what fluctuations are like on a small-scale. I’m hoping this is training me to be prepared for fluctuations when I have a lot. If I develop the non-chalance muscle, it should be easier to stay the course.

I’ve never heard of a negativity bias,…that’s really interesting food for thought! I’ve stopped checking my investments every day because I have ZERO control over the stock market, and check my checking every few days to make sure it lines up with my budget.

I recall reading of an experiment, conducted by some psychologists, that concluded people feel more pain from the loss of $100 than the joy they feel from a gain of $100. I think that is right too.

Besides, it seems obsessive to check finances every day.

Haha yup! Losing $$$ is more painful than a lot of things in life :)