Hey guys!

Just got wind that one of the more popular Fintech companies in Canada (Wealthsimple) opened up here in the U.S., and if my spidey senses are on point as they usually are, I think it’s going to be another great company to contend with in the investing space.

Outside of Vanguard, of course ;)

If you’re just starting out with investing and/or want a little more hand holding and automation, Wealthsimple may be worth looking into for you.

I’m not much of a Canadian connoisseur, but I’ve been following along their journey ever since they launched a killer blog which I am now GLUED TO (see below), and from all the awards and press they’re getting I definitely think they’re onto something.

Here are some of their latest blog posts – I dare you not to click on them! :)

- Jon Hamm Would Like to Buy a Time Machine

- Spike Lee Tells Us Why He Never Feels Bad Asking for Money

- The World’s Most Famous Sword Swallower on Becoming the World’s Most Famous Sword Swallower

I’ve since watched more and more Canadian bloggers talk about them over time, and then start moving their own money over as well. Most recently, my good friend and Rockstar Finance helper, Cait Flanders.

She just moved $50k over from fellow Canadian company, Tangerine (they had higher fees and weren’t as transparent w/ their funds), and she was finally convinced to *automatically* start investing for the FIRST TIME ever in her life too (Cait!!!). I think she’s since seen the light though, after seeing the projections Wealthsimple showed her if she keeps it up ;)

Anyways, enough of an intro…

Here’s what they’re about, and why they’re worth a look in my opinion.

What Wealthsimple Does

In a nutshell, Wealthsimple is a financial company that helps you build a portfolio of low-fee funds (ETFs), without charging you an exorbitant amount to do so. Then they’ll manage it all for you, help you grow it, and offer advice along the way.

So pretty much a “robo-advisor”, just without any minimum balance requirements and set up to be as simple as possible. They won’t charge you for trades or rebalances or account transfers (in fact, they will PAY any of the fees you might incur from moving over your money elsewhere!), and their main mission is to get people of any age and net worth to feel comfortable investing.

Here’s more of the corporate speak off their website if you prefer that version :)

“We provide world-class, long-term investment management without the high fees and account minimums associated with traditional investment managers. We invest your money in a globally diversified portfolio of low-cost index funds modeled after the same Nobel Prize-winning research used by the world’s savviest investors.

Our cutting-edge technology helps you earn the best possible return on your money, while also lowering your tax bill. This means we do things like automatic rebalancing, dividend reinvesting, and tax loss harvesting—services that most people couldn’t afford until now or found too time-consuming and tedious to do on their own.

Our financial advisers are always available when you need them. They can help plan your financial milestones and answer questions you might have about potential risks or what sort of investment accounts you should have.”

And looking at some of their stats and recent awards, I think they’re accomplishing their mission:

- They have over 20,000 clients now

- Managing over $750,000,000 of their money

- Was just named 2016’s “Best Financial Website” in the Webby Awards, as well as one of the Top 100 Most Innovative Financial Companies.

- And have $50 million in backing from one of the world’s largest financial companies (Power Financial)

A Look at The Portfolios They Offer

So how and where do they invest everyone’s money?? They use a similar approach that other robo-advisors use, which is basing portfolios on “Modern Portfolio Theory” introduced by the Nobel Prize-winning economist Harry Markowitz. Who basically proved that you can minimize volatility (risk) and maximize reward (money!) by diversifying your investments.

And as a refresher, typically the younger you are the more aggressive you want to go for better shot of growing your pot (and having enough time to recoup losses from major crashes), and the older/more conservative you are the more you’ll want to skew towards investments set up to *preserve* your money more than grow it.

Though of course you also have to factor in a number of other variables like how comfortable you are with risk, what strategies you believe in, if you care about socially responsible funds or not, etc etc.

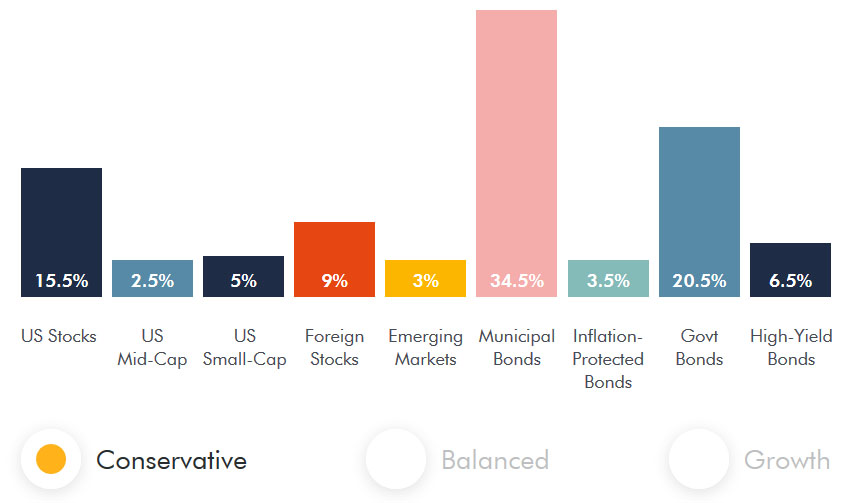

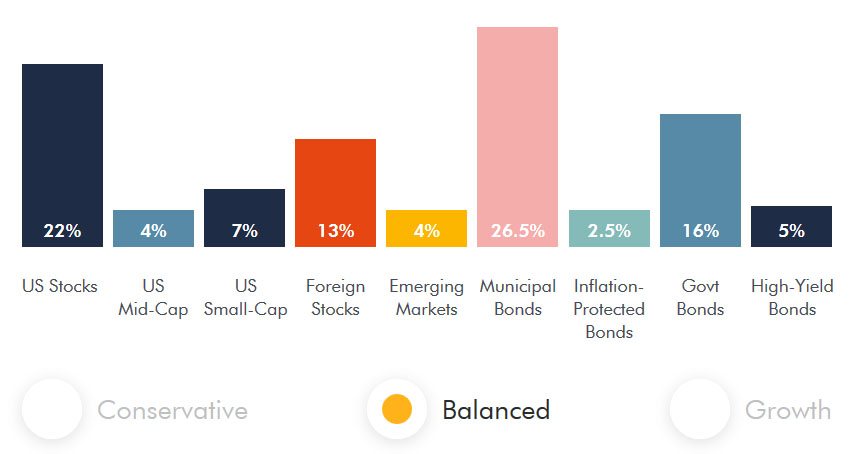

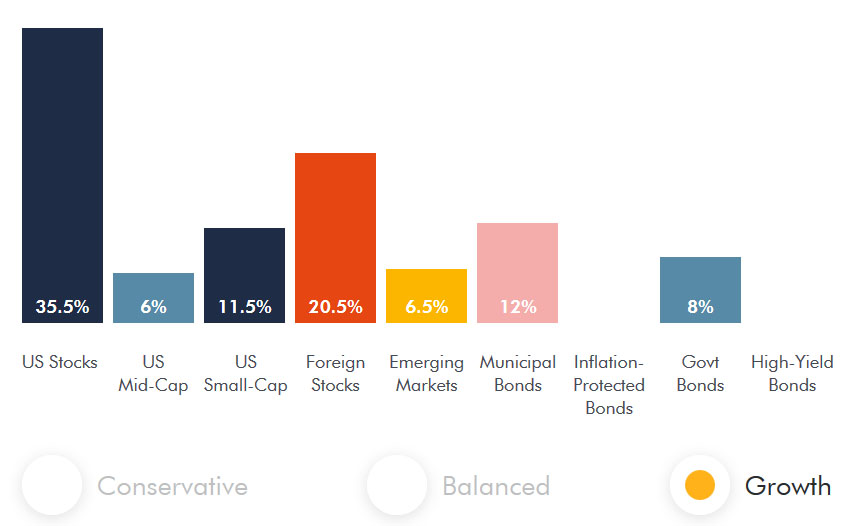

Here’s a look at the options they offer:

The Conservative Portfolio — You’ll see with this one *bonds* make up a bulk of the investments at over 70% because they’re the safest. But they also have the least returns, so those interested in growing their $$ over long periods of time probably want to shy away from this route (vs those getting closer to retirement and will soon be tapping their investments to live off).

The Balanced Portfolio — This one’s more even across the board, and probably the one most people start with when first dipping their toes into investing. You’ll get 50% stocks and 50%’ish bonds. Still wayyyyyy too conservative for my blood, but it is balancing more risk/reward than the previous option.

The Growth Portfolio — Then we have the one I’d personally put my money into if I weren’t all in VTSAX with Vanguard (which is even MORE aggressive as it’s 100% stocks ;)). With this portfolio of only 20% bonds and 80% stocks, your money is set up to grow much faster while at the same time lose money faster during all the downturns – which is a matter of *when* they’ll happen, not *if*. So again it’s EXTREMELY important to know what your comfort levels are and what you’re willing to risk or not.

Though keep in mind being “risky” with ETFs (which are GROUPS of funds – not just a single stock) already waters down the risk pretty heavily. So while you are still investing in stocks overall, it’s like investing in 100 different stocks vs just 1 main one like, say, Apple or Facebook. Which rise and fall much more sharply on any given day.

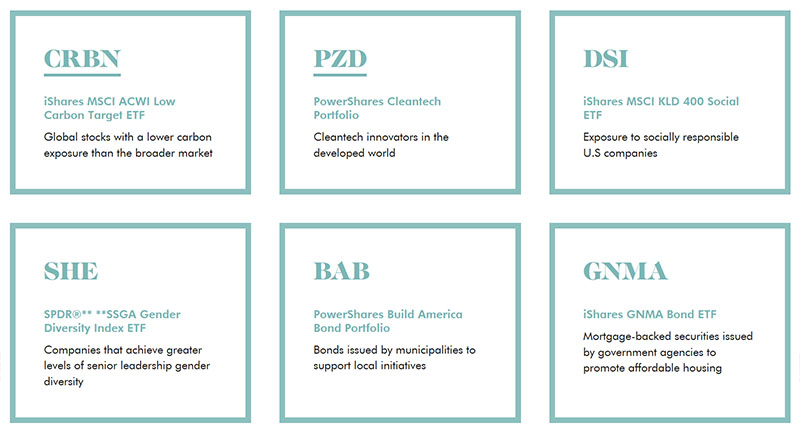

Lastly, we have the Socially Responsible Funds — these are the funds set up that prioritize the impact companies make on the world around us. For example, you won’t find cigarette or alcohol companies in here, nor maker of hairspray bottles :) Though I’m not totally versed in these, so good to check out what exactly these hold to make sure they align with your own overall goals. Pretty cool to see though how investing companies are catering to all types of preferences out there!

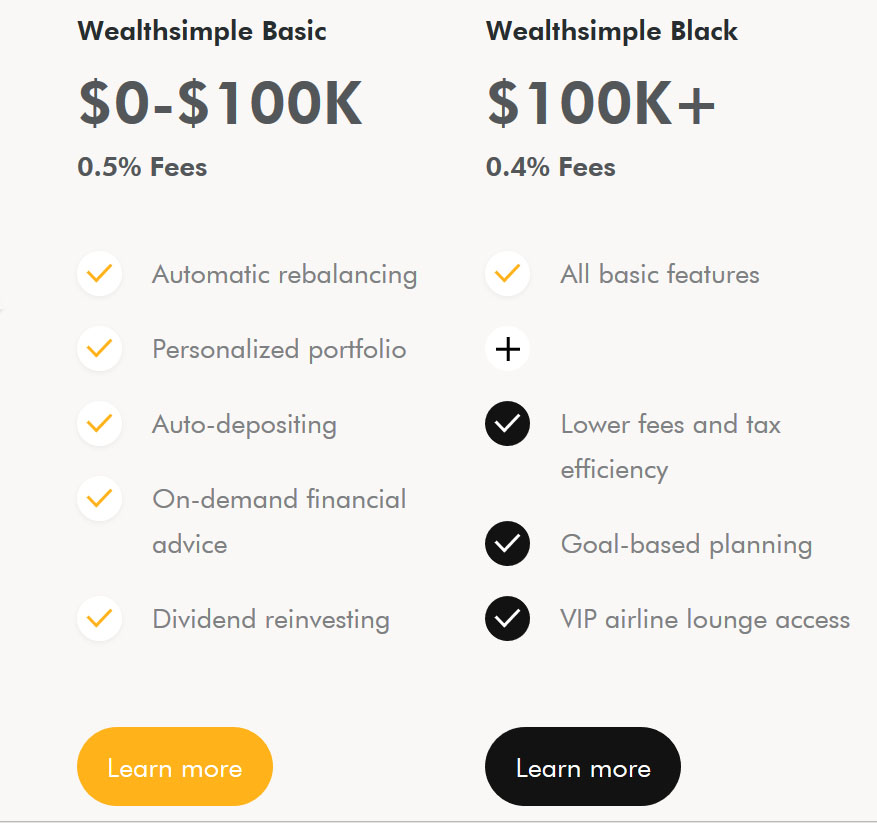

Okay, So Does Wealthsimple Cost?

Smart question – good job asking :) For the first year they will charge NO fees managing your money, as long as your portfolio is under $5,000. After that, they do start charging, but much less than you will see at other places (at least for *actively managed* funds – not doing it yourself).

Here are the two options they offer:

So it’ll cost more if you have less invested, and will cost less if you have more invested – pretty typical. If you’re already investing, check this with your own funds/firm and see how it compares?

As a reference, before I started managing my own investments I was paying anywhere from 1% to 3% in fees losing THOUSANDS over the years. And I’m a financial blogger!! (Albeit a pretty dumb one up until recently…). So wherever you put your money, just PROMISE ME you’re paying attention to all the fees you’re paying – they’re important.

Who Wealthsimple is For, and Who They’re Not For

Okay, so all that being said, here’s my personal opinion on who I think they’re for and who they’re not for. Since obviously not all Fintech is good for all situations (or people).

Who Wealthsimple IS for:

- Anyone new to investing and just wanting to get started

- Anyone who doesn’t want to spend the time researching on their own

- Anyone who doesn’t want to spend time managing any of their funds

- Anyone who’s spending exorbitant fees having other people/companies managing their portfolio

Who Wealthsimple is NOT for:

- Anyone who wants to manage their own money

- Anyone who wants the bare minimum fees due to managing their own money

- Anyone who prefers picking individual stocks or other investing strategies like dividend investing (Wealthsimple only gives options for ETFs)

- Anyone who isn’t comfortable managing their money online or via apps

Basically, you need to know yourself and your goals way before giving Wealthsimple, or any company for that matter, your business. My goal on this site is to show you a variety of avenues to help you pick the one that best fits :)

Other FAQs

- Is money insured with them? Yup. Wealthsimple accounts have SIPC coverage up to $500,000. It doesn’t mean your money is safe from losing money, but it is protected if anything should happen to Wealthsimple. (I.e. they can’t use your money)

- Is their technology safe? Yup. Similar to other apps/financial companies, they use state-of-the-art security measures when handling financial information.

- What type of accounts can you open with Wealthsimple? Personal brokerage, Roth IRAs, Traditional IRAs, and SEP IRAs.

- Do they have an app? Yes, for both Apple and Android – here are some screenshots:

(The shots feature Canadian retirement accounts above (RRSPs are like our 401(k)s I believe?) but the app works and looks the same in the U.S. version)

In Summary

Wealthsimple is the new kid in town, and they want to help you invest your money simply, no matter how little (or much) you have. And so far they look promising – but of course ultimately it only matters what YOU think :) My job is to just share the stuff I think is worth consideration…

You can learn more about Wealthsimple, and sign up, here: Wealthsimple.com

(Budgets Are Sexy readers receive a special $50 bonus when you open and fund a new Wealthsimple account, and another $50 bonus if you end up transferring enough to qualify for Wealthsimple Black. Just make sure to click & use that link above if you want it as it’ll track that you came from here)

If you’re one of our sexy Canadian readers, use this link instead :)

(Same bonuses apply)

********

PS: Did I tell you they had a good sense of humor too? :) The above is part of one of their older campaigns, haha… You might have caught their Super Bowl commercial “Mad World” too.

PPS: This post was in partnership with Wealthsimple, and just like with any other companies we love and promote on the site, the links above to them are affiliate links. Meaning we get compensated if you end up using them to sign up. You’ll also get a nice bonus as well, but regardless we only share stuff we think can help you or your wallet. Your trust and readership is much more important than a few extra bones, which you hopefully know by now :)

Get blog posts automatically emailed to you!

I can’t decide if these automatic investing services are good. I guess it’s better than the historical ‘adviser’ (salesman), but I also think that it pushes the boundaries of the manual-to-automated spectrum. There’s some ideal point on that curve that lets you have control AND understand the situation, and if it’s fully automated, you definitely lose that.

For sure. In a perfect world *everyone* would take the time to research and learn and then manage it all themselves, but we all know what the reality is so I’m all for places that help you to pull the trigger until/if you get to that place. Same with all the other automated apps for saving or paying off debt, etc… It’s all better than doing nothing!

Sounds like a lot of these Fintech companies are pushing out the marginal investment advisors. It’ll be interesting to see who is left in 10 years as the gain more of the market share. Although from what I read Vanguard has been killing it with a bunch of money flowing into passive ETFs. Should be interesting to see how they respond to Charles Schwab lowering their fees. Maybe one day these companies will pay us to hold their funds :)

HAH! That would be something! :)

Over the last three calendar years, Vanguard has seen about 8.5 times more money flow in that the entire rest of the U.S. mutual fund industry combined!!!!!!!!!

https://www.nytimes.com/2017/04/14/business/mutfund/vanguard-mutual-index-funds-growth.html

It’s good to see the great advancements that are being made to help the population get better at investing. If I had learned about this 6 years ago I have loved to get started with them. I remember when I first started thinking about investing and having no idea where to go or how to go about getting started. Luckily I had at least heard about Vanguard and was able to get it figured out on my own but this sounds like it would have made the process much easier. But now I’m so thoroughly into Vanguard that I don’t think its worth moving unless I come across a ridiculously good deal. Thanks for sharing.

Yup! I think ALL of us would have been better off had these technologies come about years ago… Some (like Betterment) mainly only use Vanguard funds too which is pretty cool. I’m also not leaving them :)

I think it’s great that you added the info about the type of investor this type of company is targeted to. I think with blogs like this one, all except the real beginner doesn’t need much knowledge to start. I realize that many are intimidated and need a hand, which is why these relatively inexpensive companies will have a place but the fees do add up, even low ones. Spending $400 for every $100,000 may not seem like much but over 30 years (and the loss of investment returns on those fees) may mean it will take an extra year or so to get to FIRE.

My strategy is similar to yours – pick one of the low cost mutual fund companies (Vanguard (my choice too), or Fidelity), stick to 2 or 4 funds and you can mirror the investment portfolios of these robo companies. My mix is more conservative than yours but I’m older too — 65% Total Market, 20% bonds and about 15% International. Rebalance one a year and you’re good for the long term.

As always, thanks for keeping me informed.

Glad you liked, brother! Def. true about fees over time… It’s pretty funny – we always talk about the difference of what a few hundred dollars can do over time comparing fintech apps with the likes of Vanguard, but 95% of the other funds/companies charge you *thousands* more widening that gap pretty wildly. I can’t even tell you what I was paying just 4 years ago before wisening up – it was multiples of Wealthsimple + Vanguard combined!

I’m not as well-versed in the investing world as I probably should be. However, these fintech companies do interest me. I was considering putting some money into Acorns. Anybody have success investing Acorns or another company like Wealthsimple? Do you pause at the fees? I like Acorns is $1 per month up to $4,999 and anything $5,000 and over it’s 0.25% per year.

Love Acorns!. I’m not sure how much as an investment account vs just for the fact it puts away my spare change. I have had them about 20 months now and have about 1k in that account. I am mainly using it as a way to save up for a vacation. If you prefer to do chunks of money there is also wealthfront as they have no fee under 10k or 15k if you find an affiliate link. Over that amount I’m not sure, I am not there yet but these fees seem a little higher than wealthfront and betterment, still reasonable but I would rather pay .25% than .4-.5%.

About your question “do you pause at the fees”, not really, I mean I am aware of them but I’m choosing to believe that Tax loss harvesting will at the very least pay for the fee. I could do it all myself in Vanguard or similar and avoid the management fee, but I am not a stock market guru and choose to put my mental energy into something else.

Agree with Paul – I’ve been using them for two years now (though will prob stop just to streamline my accounts more) and have over $600 saved from purely round-ups. It’s a fun easy way to pad your accounts more, and I’m totally fine paying the $20 total over the time for that. They have tons of ways to automate and invest more too just like a “regular” account, though similarly to Paul I just use them for extra investing.

I think whatever gets you to *START* is the most important. You can always move everything around later – it’s all about just stashing that money aside early and letting it start working it’s magic!

With ya on the portfolio allocations, very conservative but I can see this being a good intro just like Acorns is. More competition = Lower Fees over time, hopefully, they start competing hard for our business.

Thanks for the in-depth review as usual

Very interested read. My question would be:

How do you compare Wealthsimple vs Betterment?

Great question!

I know TONS of $$$ bloggers use and rave of Betterment, but I’ve just never really stopped to fully look into or review them over the years. From the little I know though I feel like they’re very similar in what they do and their vision? Mr. Money Mustache had a good write up on them the other year and then created a page to track progress when he compared them to Vanguard… let me find it for you…

here we are:

http://www.mrmoneymustache.com/betterment-vs-vanguard/

Could be helpful for ya :)

I’m glad more and more players are entering the robo advisors space. They will push each other to be better and cheaper and consumers will reap the rewards. I’m happy managing my own money and I use a combination of a small number of Fidelity and Vanguard funds (heavily weighted towards Vanguard), but I know that that isn’t for everyone and these new companies are doing a great job of getting people who wouldn’t otherwise invest to dive right in.

Yep! My thoughts exactly.

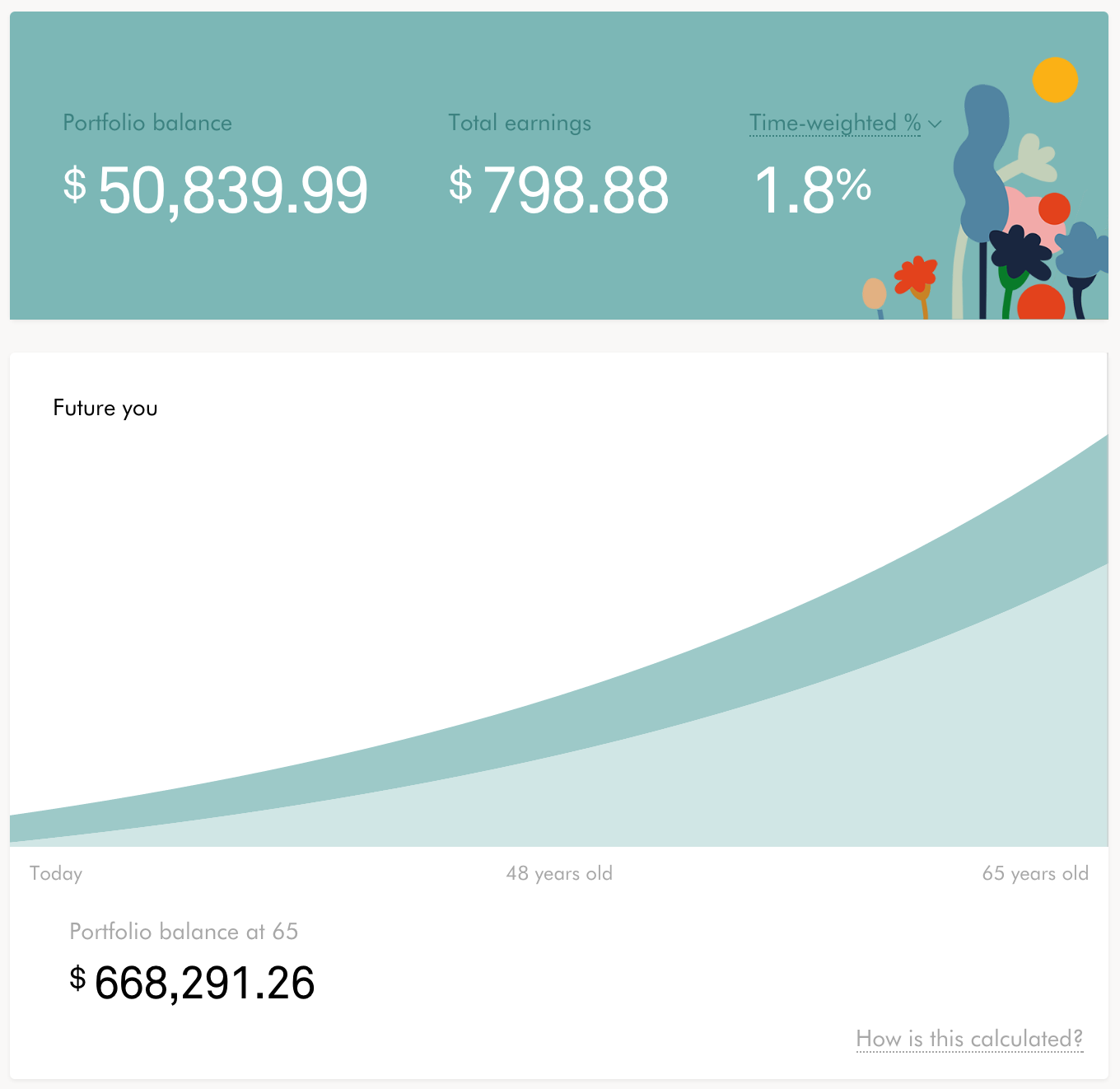

It seems like a good option for investing. It will ultimately compete with Betterment, as it has similar services. I like the compounding simulation and its good to see it every time one logs in.

It really does looks like a nice layout of the app. Sometimes that is what you need to keep coming back and keep that involvement up. I like to have some visual representation of what my money is doing. It helps me focus more. Cheers

Especially if it always trends UP :)

Hi J. Money,

I have taken many of your recommendations. I had digit. they were sort of pain, because it started by taking small sums of money and then was taking $40 at a time. With zero sum budgeting, digit didn’t really work for me. I was just transferring the $ back to my checking account every $100-$200. When they just announced their money fee, I closed this account.

I also use Qoins for round ups on a credit card and the payment goes to the credit card. And I have acorns for investing the round ups. This uses my checking account. I have close to $600 in that since you recommended it.

I am saving for my next used car with that money. I imagine when I have a few thousand or so, I could move it to wealthfront. My that time there will probably be more of these companies (apps) out there.

Thanks for seeking out this info and passing it on. I love the ones that deal with round ups.

Good work experimenting so much! That’s the name of the game really – finding those that work well for you, and shutting down the rest…

Glad you’re finding them helpful :)

Hey guys. I’ve been using WealthSimple since November and here are my thoughts:

1. Their customer service history is questionable, a quick search on Reddit will show you a bunch of complaints, attributed primarily to the expansion into the USA.

2. Transparency of fees and what is/isn’t included vs WS Black wasn’t noted on any registration screens, nor could you find it simply by browsing the website. So, when you set up a portfolio with a 401k and a IRA, the WS algorithm doesn’t acknowledge you have these accounts and won’t set them up to be tax efficient unless you’re a WS Black member. Just something to note.

3. The app and website are great, but the data and projections provided are rudimentary, not good if you’re a data and numbers person.

4. They connect to Mint. Not sure about Personal Capital.

5. It was great for me to just get started and moving away from my other institutions which charged an arm and a leg for very modest returns. I’m not sure if I’ll stay with them long term but it’s a great option to start with.

Excellent notes – thank you!!

#5 is the most important one in my view – you’re making moves and looking for the best home for your $$$, even if Wealthsimple isn’t it.

Thanks for the raw feedback :)

It’s cool that more robo-advisors are entering the investing space! I still think something like Wealthfront is better. Wealthfront manages your first $15,000 for free, then it’s 0.25% after that. Betterment has a similiar fee of 0.25%. Wealthsimple seems good but I think their 0.50% fee is a little high.

Oh nice! Haven’t poked around Wealthfront much, but have def. heard good things about them too :)

Thanks for the info. Been looking for a great place to invest in bonds. Will definitely check it out.