[Hey guys! If you ever doubted the power of a 401(k), this should help remind you again ;) My man Fritz from The Retirement Manifesto stops by today to share his own story (and love!) for his 401(k), and this might just become my new default article to send to future haters! It’s brilliant!]

*******

A few weeks ago, J$ shared a CNN piece on “401(k) Millionaires” over on his Rockstar Forums. When I replied that I, too, was a 401(k) Millionaire, he invited me to tell my story and I agreed to do so in complete and transparent detail.

Learn from it, apply the lessons, and you, too, can become a Millionaire!

The 9 Keys to Becoming a 401(k) Millionaire

The original story on becoming a 401(k) Millionaire cited 5 keys, of which I followed every last one, as well as 4 others I’ve learned throughout my life. I will be telling my story using all 9 of these steps, and will show you how they have helped my wife and I become 401(k) Millionaires ourselves.

Key #1: Start Young

On July 5, 1985 I started my first “career” job. At 22 years of age, and just one month out of college, I was pleased with my $21,500 starting salary. During my orientation, I signed up for our “new” 401(k) plan, and contributed from my very first paycheck.

Unfortunately, I’ve lost track of my exact 401(k) contribution %’s early in my career. I believe I started at 6% (don’t give up that employer match!), and I gradually increased it through the years. As I became more knowledgeable about personal finance, I got much more aggressive in my contributions.

I’ve been contributing 15% or more for at least 2 decades now, and max out my 401(k) every year. I’ve never taken any money out of my 401(k). Invest it, and forget it.

My daughter just started her first “real job” as a police officer, and we taught her these “First 6 Steps To Financial Wealth” . Before she received her first paycheck, we set her up with a Vanguard Roth and a Capital One savings account. We’re teaching her the lessons we learned early, and I’ve no doubt she’ll see the benefits of “starting young” as she goes through life.

Key #2: Crush It Early

While a lot of folks focus on “Frugality” as a key to wealth creation, a much bigger lever is to maximize your earning potential. Early in your career, go “above and beyond” to create your professional reputation. You only get one chance to make a first impression, and it’s never more important to impress the right people than in the first few years of your career. When “the right folks” notice early, you’ll be naturally propelled in the first decade of your career, and much better positioned for lifetime advancement and wealth creation.

I was fortunate to impress some of the “right” folks early in my career, and was offered my first promotion within 18 months. A bit of luck always helps, and the reality is that my promotion was driven by the closing of the plant where I was working, and my company’s desire to keep me in their employment. I’ll never regret going “above and beyond” in those first 18 months. It saved my job, and I gained a promotion in the process. Almost everyone else I worked with found themselves unexpectedly unemployed. I was one of the lucky ones, but I also worked hard for that opportunity.

Moving from an “internal” Customer Service role to an “external” Sales Role, I saw my salary increase to $29,800 with my first relocation to our Dallas, TX sales office in December 1986. In 1988, I received (earned?) my second promotion, this time from “Sales Trainee” to a full fledged “Sales Representative” with another relocation (this time to Atlanta, GA) and another salary bump.

To give you a sense of what “Crush It Early” looks from a salary perspective, here’s a history of my first 6 years in Corporate America (FYI: these were the days of stagflation, with high inflation, 15% mortgage rates, and much higher annual salary increases than today):

| Date | Salary | % Increase | Comment |

| Jul, 1985 | $21,500 | n.a. | Yay, My First Job! |

| Jan, 1986 | $23,300 | 8.4% | My first raise! |

| Jul, 1986 | $25,100 | 7.7% | My boss, taking care of me |

| Dec, 2986 | $29,800 | 18.7% | My first promotion!! |

| Dec, 1987 | $32,200 | 8.1% | |

| Apr, 1988 | $35,700 | 10.9% | My second promotion! |

| Apr, 1989 | $38,500 | 7.8% | |

| Sep, 1989 | $41,500 | 7.8% | Job grade bump (competitor wanted me) |

| Sep, 1990 | $44,100 | 6.3% |

Within 5 years, I had doubled my salary through hard work, making positive impressions, and having a competitor pursue me (unsolicited, but I listened. After careful consideration, I told my boss about the offer, and received a nice “mid-year” retention bump as a result).

Every time my salary increased, my wife and I took a portion of the increase and nudged up our 401(k) contributions before we ever saw the money.

Our Net Worth in 1988: $9,996.73

Looking through my files for this article, the earliest 401(k) statement I could find was from June 1988. At this point, I had been in my career for exactly 3 years. I had been married for less than a year, and my wife and I were $3.27 short of the $10k mark in my 401(k), as demonstrated below:

When we got married in 1987, my wife began work as an Executive Assistant. Knowing we wanted her to be able to be a “stay at home” Mom when that time came, we increased my 401(k) and set up some ACH transfers to mutual funds, resulting in us saving the equivalent of 100% of her paycheck.

This allowed us to avoid getting used to her income, as well as the mistake of getting into obligations that required her pay for expense coverage. When we adopted our daughter in 1994, my wife simply “retired” (at age 31, lucky girl!), and we cut back a bit on our savings to keep our take home pay constant.

From 1987 to 1994, our 401(k) balance increased from $10k to $59k as a result of that decision, and set us on the path toward our eventual “401(k) Millionaire” status.

Key #3: Seek Opportunities For Exposure

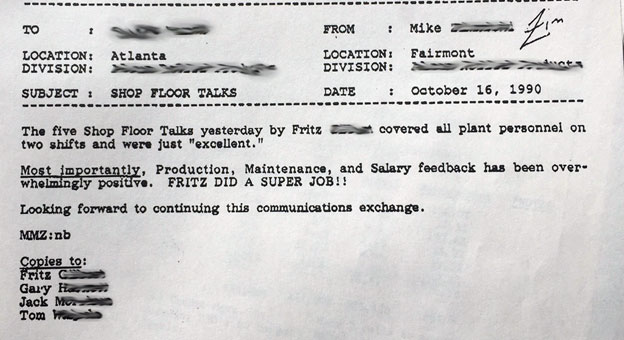

By 1990, I started getting more involved with a broader communication effort around the organization. One of those initiatives was to visit our plants with a “commercial update”, providing our plant workers a report from the “front lines” on what was happening with our customers and marketplace. I was 27 years old, and giving presentations to a room full of shop floor personnel.

Seek opportunities! The effort paid off with even more folks starting to recognize me as a “young guy with potential”, and my reputation continued to grow:

Keys #4 and #5: Get Out Of Your Comfort Zone (and Find A Mentor)

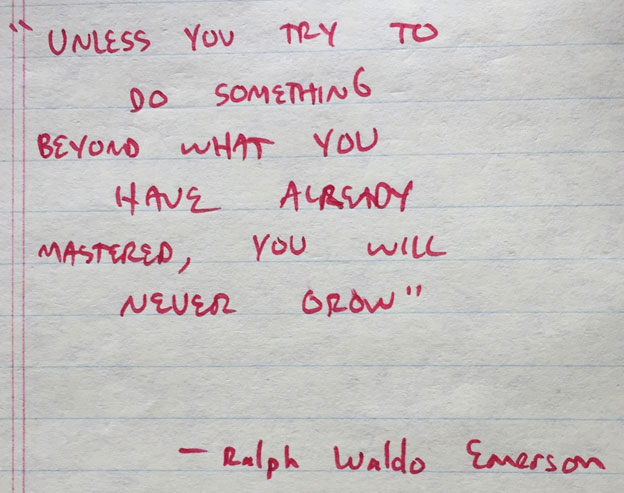

After 15 years in Sales, I was getting restless. I had a strong mentor who ran one of our larger plants, and I had some excellent career discussions with him in my mid-30’s. He kept an eye out for me, and within a short amount of time I had moved from a commercial role into my first “plant job”, planning the production & scheduling of a large operation.

That experience later led to opportunities for career advancement into national and global management roles, and I’m sure I would have never made those advancements without breaking out of the “sales track” which I had been on for 15 years.

Ironically, looking through my career files for this post, I found a note I had written to myself at the same point in my career when I had decided to “branch out”. Looking back, I had no idea how significant the quote would become:

Key #6: Watch Out For Fees

Fortunately, my employer had chosen Vanguard as their 401(k) provider, and I was rewarded with a low cost 401(k) plan that had excellent investment options. My employer also continued to improve the plan over the years, with expanded investment choices and continued low fees.

If you don’t have a good plan, I would still encourage you to participate in your plan. At a minimum, do not give up the employer match. It’s free money, and the 50 – 100% “return” you get from your employer’s match offsets any high fees and poor investment choices you may have in your plan.

Review your plan now, and if you’re not maximizing your employer match, increase your contributions before your next paycheck!

Key #7: Max Out Your Contributions

As my salary continued to increase, we continued to increase our 401(k) contribution. If I received a 3% raise, for example, I’d increase my 401(k) contributions by 2% in the month the raise took effect.

Our take-home pay would increase by 1%, and we’d feel like we had a bit more money. More importantly, our 401(k) investments increased on a compounding scale. We did that every year, until we hit the limit that I was allowed to contribute to the plan.

We still do the “mental gymnastics”, but we now (since we’re maxing out the 401) use external mutual funds and ACH transfers to capture the increases in annual savings %’s.

Key #8: Live Frugally

As my salary increased over the years, the strategy of increasing my contributions at the same time we received a raise helped avoid lifestyle inflation. I’ve seen many, many co-workers increase their living expenses as their salaries have increased, and I suspect most of those are not yet 401(k) millionaires (or any millionaires for that matter).

My wife and I have always lived below our means, and I firmly believe that’s played the biggest role in becoming a millionaire. We’ve always been generous, and have contributed annually to our church and charities of our choice. [Editor’s Note: And also to projects your blog friends put on! Thanks again for the financial boost to our Community Fund :)]

We also only pay cash for our cars, and of course drive them right “into the ground”. Today, at 53 years of age, my wife drives a 2011 Hyundai, and I drive a 2010 Nissan. We could both be driving newer and fancier cars, but why? Our cars get us where we need to go, and they keep our expenses down. Keep up with The Jones?? Please!

We recently downsized our home in preparation for an early retirement, and are now ENTIRELY DEBT FREE. As my dad used to tell me early in my career:

“It’s easy to become wealthy. Just spend less than you make, and do it for a long time.”

Key #9: Automate Your Savings

For the past 31+ years, I’ve automated my savings. Starting WAY back in July 1985, when I had my very first paycheck automatically directed into my 401(k) which hasn’t stopped since. Automating those savings has “forced” us to live frugally, below our means.

We Officially Become 401(k) Millionaires!

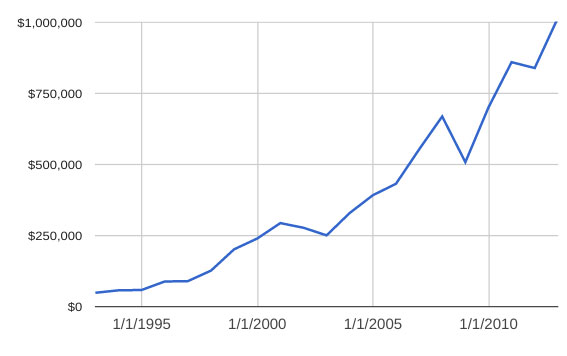

For years, our 401(k) balance inched, ever so slowly, “Northward”. It wasn’t too exciting for the first 10 years, and we pretty much ignored the growth. Starting in 1992, I began tracking my Net Worth (if you’re not doing that yet, start NOW!). I now have 24 years of annual Net Worth data, in a nice little spreadsheet that shows us what we’ve accomplished.

Pulling from that data, you can see the progression of our 401(k) balance through the decades:

In March 2013, we officially crossed the $1 Million mark in our 401(k). After decades of diligence, we can now officially say: “We’re 401(k) Millionaires!!”

In Conclusion…

There you have it. The 9 steps that led me to becoming a 401(k) Millionaire:

- Start Young

- Crush It Early

- Seek Opportunities For Exposure

- Get Out Of Your Comfort Zone

- Find A Mentor

- Watch Out For Fees

- Max Out Your Contributions

- Live Frugally

- Automate Your Savings

Apply as many of them in your life as you possibly can, then give it time. Do it right, and you’ll find yourself among a very small minority of folks who will have realistic opportunities to retire at an earlier than “normal” age.

My wife and I plan on heading out for extended road trips in a 5th wheel within the next 18 months. We’ll be 55 years old, and will never have to work another day in our lives. We’ve not done any crazy extreme “frugal” living. We’ve lived well, we’ve traveled the world on vacations, we raised a daughter (and paid for her college!), and we don’t feel we’ve sacrificed while on “The Journey”.

Learn from our experience. With time, and a bit of luck, someday you can also be a 401(k) Millionaire!

******

Fritz is a commodity trader with a large multinational corporation, with his eyes on achieving an early retirement in 2018. He writes about personal finance and his preparation for retirement at The Retirement Manifesto, and can also be found on Twitter (@RetireManifesto) as well as on Facebook (facebook.com/TheRetirementManifesto).

Get blog posts automatically emailed to you!

“Crush It Early!” That’s powerful advice. Starting young and focusing on increasing your salary while resisting lifestyle inflation and investing the difference is pretty much the recipe for success. Congrats on your 401(k) millionaire status!

I wish I hadn’t allowed relationships to get in the way of my early savings strategy. I would’ve been sitting here retired already. Another key factor, in my opinion, is choosing a partner with similar views and values when it comes to money. Making a poor decision in this area could easily sink everything.

Mrs. Mad Money Monster

MMMM, I agree, the biggest lever is starting early, and hitting it hard. Compounding is an amazing thing, and once you miss that chance, it’s gone.

Nice addition of “choosing a partner w similar views”, also a big factor!

Fantastic advice. Nothing further I can add. I too started contributing to my 401k with my very first paycheck. I started at 20%, and outside the period where my wife quit her job to go back to school, always contributed between 15-25% during my early years. Recently, I began maxing out my 401k at $18k per year.

Starting young has such a big impact. Our biggest asset when we first start working is time. Becoming a millionaire through your 401k is really pretty easy. Consistently make contributions and let the compounding work its magic!

20% at the start!? Whoa, now that’s crushing it! Congrats. If you’re not a 401(k) millionaire yet, you soon will be at that pace!

Congrats on hitting the $1m threshold. I’m less than halfway there at age 36 but by continuing to follow many of the steps you’ve outlined I hope to be there in the next 10 years.

At Age 36, I was only at $250k. I hit $1M at Age 50. Looks like you’re ahead of my pace, congrats!

I’m with you Alex – only at 37 :)

Time, Time, Time! This is the one that gets me sometimes. I’m currently in that stage of watching the 401(k) value slowly inch upwards. I know that it will hit a point someday that it takes off but waiting for that day can feel arduous sometimes. I’ve only been working for just over 3.5 years and have contributed 17% of my salary towards (about $13k after company match) my 401(k) for most of that time. It’s already grown to $41k but it does seem like a slow process, go glad I started as soon as I possibly could have. (I’ve always had struggles with patience ;))

I’ve often though about increasing my 401(k) contribution because we have the room in our budget to do so but my concern has been that I don’t want to end up in a situation where all of my investments are tied up in accounts that I can’t touch till I hit the age limit. since I hope to be able to retire before I hit 40 I will need to be able to have investments that I can draw from for over 20 years before I’ll even be allowed to touch my 401(k). I fear getting to the point where I can retire but not being able to because the funds aren’t available to me. Any suggestions?

You’re being smart. For real FIRE (<Age 50), make sure you're also building your After-Tax accounts, since you'll need to live on that $$ til Age 59.5! You need to achieve a balance, both tax advantage AND FIRE liquidity. Then, be patient (time, time, time!).

Yes, you’ll need external money but you can also do a Roth conversion ladder which gives you access to funds converted from 401k’s and IRA’s through a new Roth IRA. After 5 years you can take it out. This likely won’t eliminate the need for external funds but it will reduce it.

That’s what I plan on messing around with too once the time comes… Almost every penny of mine is tied up in retirement accounts up to this point.

Hey BoS,

You should look into a Roth IRA, while you still can. As long as you don’t make more than ~135k (single) or ~195k (married) then you can contribute up to $5,500 a year (Post-Tax) to a Roth IRA.

The beauty of a Roth is that: 1) They are post-tax dollars, so you pay the tax now and can withdraw the compounded earnings TAX-FREE later, and more importantly for you, 2) You can withdraw the principal at any time for FREE (you have to leave your gains alone), 3) Plenty of life events qualify for 100% withdrawal for free, such as 1st time home buying and certain medical emergencies.

I, too, have only been in the workforce for a few years (wow.. actually more than 4.5 now) and both my wife and I plan on contributing the max to our Roths for as long as we can. I started following J$ about 2.5 years ago now and was inspired to calculate my net worth, which was then only about 60k.

Now, the wifey and I also contribute as much as we can to our 401k’s, I have a brokerage account, and we recently bought a house (which has appreciated over 50k since we bought it!!!) which puts our net worth currently @ 315k.

Keep up the good work, with enough patience compounding will start to explode and you’ll be happy you had some exposure in post-tax earnings ;)

Love to hear that, John!

Thanks for sharing Fritz – 401k millionaire is a huge accomplishment. It’s hard to image it growing that big when you first start out. Thanks for giving me hope!

Hey Cuz!! Nice to see your numbers all in one spot. You’ve been tracking since 1992?? Between that and the forums, I would never leave my house if I had that much to look at! Ive only been tracking my assets since 2012 but I love comparing all my spreadsheets – especially the expenses. Lord knows what I would do with and extra 20 years of data!! Your daughter is very lucky to have you guys as great financial role models. I cant wait to see you hit 2 million!!

Cuz!! Yep, tracking since ’92, but I only update my Net Worth once/year. No need for a spending budget: automate savings @ 20%+, then just spend what you have left over (and nothing more). I spend ~2 hours/year tracking this stuff, that’s it! BTW, I’m the lucky one to have my daughter, and proud of that kid!!

Great post, Fritz! You nailed it with your 401K. I love how you focus on career growth. Asking for more responsibilities, performing well, getting good exposure, and having good mentors early on have really helped me propel my career (10 years and running). My wife and I are almost 401K 1/2 millionaires and should eclipse that $500K mark this year. We’ve been maxing them out now for the last 5 years! Slow and steady drives some amazing results!

Thanks, TGS!! One thing I’ve learned as I look back, it was my early career growth that led to the success. LOTS written about frugality, but a focus on the income side is the biggest lever. Looks like you’ve had the same experience, congrats on the $500k mark!!

Awesome job Fritz!!! So many valuable lessons packed into this article. I think my biggest take away is the Emerson quote. Personally for me it’s hard to get outside of my bubble and explore new things. But in the back of my head I know how valuable it it to get stretched so that I can grow in my career. This is a nice kick in the pants :)

Mustard, I was SOOOO excited when I found that OLD Emerson quote in my files. Can’t believe it kept it for 25 years! Happy to see it making an impact so many years later, it certainly impacted my life, in hindsite!

Thank you for providing an example of good and steady progress. When you are 26, like I am, the light to FI seems so far away. I just have to stay on path.

Patience Is A Virtue. It seems like it takes FOREVER, but eventually the compounding kicks in and that line on the chart starts a beautiful curve “up”. Hang in there, your time will come!

Great post Fritz! You could fill an entire personal finance book with the knowledge in this post. I love how you invested in yourself throughout the years and the money came as a result of that.

Starting early is so incredibly important mathematically and your story is a fantastic example.

“You could fill an entire personal finance book…”

Trust me, I’ve thought about it. For now, my 5+ decades of experience are giving me lots of fodder for my blog! SOOOO glad I started in my early 20’s. You can never get those years back, and there’s no bigger impact than compounding!

I agree – would make a helluva catchy book title too! No way people wouldn’t pick that up!!

Consistency is key. Setting up a 401k to be automatic and building your lifestyle off the remaining cash is easy once you get to the max. At that point you don’t even think about that money as yours to spend. On the way up it does take a bit of self control though. Still as shown it works. Thanks for the insights and perspective.

Gaaahhh, I am so jealous of that employer match! I opted for a Roth IRA since it’s a little more flexible, but wow, you can’t beat an employer match. I get zilcho matching so that sounds like free money to me. :) I completely agree that the key is to have time on your side. Fortunately I started my IRA when I was 22 as well, so hopefully that will set me up for success in early retirement!

Do you recommend maxing out 401(k)s while still in debt? Mr. Picky Pincher and I are tackling our $60,000 student loan debts with ~6% interest, so I’m not sure it makes sense to divert those funds to retirement, but I’d like to hear your thoughts.

Mrs Picky!! You’ll love the Roth once you start withdrawing tax free!! Sure, no match sucks, but starting at 22 will go a long way to offsetting that!

As for debt vs. retirement, depends who you listen to. Personally, we did both. I think it’s dangerous to go 100% to debt, even at the 6% rate you’ve got. “Tilt” toward debt, but max out your Roth every year, at a minimum. My thoughts…

I’ll just chime in here too and say that I make most of my decisions like this on *what excites me the most* at the time. This way I always enjoy doing it whichever path it is – AND – I can switch it up later if I get bored and the other route starts exciting me more. For me I feel like as long as the actions increase your net worth one way or the other, you really can’t go wrong :)

I’d love to know what your average annual return was over that time. I’m 36 and started investing out of college. By my calculation, I’ve earned an average return, since 2002 of 7.44%.

I’m willing to bet that you did better than that over the years. The frustrations part is that we’re sold this figure of 8% by those who earn fees off our investments and I’m not sure that we can reasonably achieve those returns because of fees and somewhat reluctant growth.

If you have that figure, I would love for you to share.

Btw, @ 7.44%, I forecast to be @$1M in 2028, 26 years after my wife and I started. That’s slightly faster than your 28 years, but again, it’s a FORECAST…….while yours is reality!!

Nice work, good advice, thanks for sharing

Great question, Braden. Afraid I don’t have those numbers, and it’s be impossible to back calculate since I’ve had to adjust for my contributions. I would expect I was around 8%, as equities were ~10%, but I also had fixed/bonds in my asset allocation at a lower return.

I agree future stock market returns will likely be softer, given current high valuations. Just keep contributing, control what you can control. Sounds like you’re on great track!

Hey that’s awesome you will reach FI in 2018. Reaching a million is a great goal and hopefully you can find financial peace. When I hit my number I will stop the accumulation and just focus on other things. I just saw a forbes list of 1500 billionaires, that is an insane amount of money. Some might be satisfied while others are still trying to grow funds, which I don’t get, but to each their own. Good luck in 2017.

Ironically, I’ve always had Financial Peace. Money’s never been a big focus on mine. Crazy, right? Keep things in perspective, life’s about a LOT more than $$$!

Move over Dave Ramsey, David Bach, and Mr. Money Mustache. There’s a new financial guru in town. Way to go, Fritz. If this post doesn’t get the reader excited about crushing his or her finances and pursuing early retirement, I don’t know what will.

Wow, putting me up there with the heavies!! Thanks for the kind words, Mr G, but afraid those legends are far above my league!!

Congrats! That’s a great accomplishment. Starting early is the way to go. We’ve been adding our 401k since ’96 and we’ll get there soon. It just take a little time. Your graph is very telling. You can see the steep gain in the last few years. nice.

Good point about the steep gains, a clear example of compounding. I think of it as a “Demoninator Effect”. The bigger the demonimator, the bigger the annual gains. The exciting part is when the gain in your 401(k) exceeds your annual salary. THAT’S an exciting benchmark to cross!

I love this post!! I’m 38 and have $291K in my 401K and my husband has $140K. Plus we have Roth IRA’s and regular IRA’s. So excited to see that saving $1 million in your 401K is doable. We are now starting to focus on our taxable accounts this way if we do decide to retire early, we will have some money to live on for a few years.

Thanks for posting!

Kristy’s CRUSHING it!! Good call to start building taxable accounts as well, especially for FIRE. I’ve done the same, tho this article only focused on the 401(k) aspect. You definately want tax diversification, and liquidity if you’re targeting an early retirement! Nice addition to the discussion, thanks for stopping by!

Excellent post. I will be sending this to my colleagues (many of whom make 6 figures right out of school) who say they don’t have enough money to contribute to their 401k, let alone max it out! Very sad when a number of colleagues told me that.

Another thing people don’t take into account is that contributing $1,000 into your 401k doesn’t mean your paycheck is $1,000 less. You don’t have to pay taxes on that $1,000 for that year, so if you’re in a 25% tax bracket you actually only “lose out” on $750. You’ll have to pay taxes on withdrawal down the line but having tax free growth over decades more than makes up for that.

Syed, great point on the “net” impact of contributed before tax $ to a 401 (k).

To Syed’s Friends: QUIT KEEPING UP WITH THE JONES!

Yeah, it def. hurts less w/ those paychecks coming out that way early on. Especially if you’re already feeling like you can’t contribute to your 401(k) (which we all know most people can!).

Nicely done Fritz! Congratulations on the 401k millionaire status and on a really well written article explaining how to duplicate your success. I think my favourite part of this post were the typed out memos – actual old school paper memos! We don’t see those anymore.

I’ve been maxing out my 401k since the start of my career in the U.S. Unfortunately, that start came at 30, because that is when I migrated here. Oh well. Better late than never.

Mrs B! Trust me, 30 isn’t late. There are many many 50 year olds who haven’t started yet. Hate to say it, but they’re, um….kinda screwed.

You’ll be fine. The best day to start was yesterday. The second best? Today!

Way to go, Fritz! I love that you point out it wasn’t extreme frugality that got you that 401(k) million. :)

The chart really shows how growth happens exponentially. You don’t see a ton happening early on, which I think can frustrate some people, but when you get to the end there, it just really starts to shoot up. People just need to have the patience to get to that point!

Patience is the key! A snowball starts small, but about 1/2 way down the hill it starts to grow exponentially! Fun to see it happen first hand!!

Great job, Fritz!

Congratulations on the 401(k) millionaire status! Thanks for explaining how to duplicate your success as well!

I’m doing the same right now and maxing out my 401(k) every year and because my money goes into my 401(k) instead of my bank, I don’t spend as much because I “don’t” see it. What’s not there can’t be spent!

Welcome to the club. I think your steps are the hole nine yards. Thank you and congratulations.

Time (T) + Discipline (D) = Compounded Returns (or Cha-Ching) ;)

Ooooh that’s good :)

Hey Fritz, I’m talking to teenagers tomorrow and definitely going to mention the ‘starting early’.

And LOVE the Emerson quote…. I feel the same and have switched from SMART to DUMB goals: Daring, Uncomfortable, Meaningful and Balanced.

Great to read your post!

Talking to teenagers!! Good for you!! We all need to find a way to reach folks while they’re still young enough to take advantage of compounding. Glad my post came out in time to help! Good luck with the young ‘uns!

Those nine steps are brilliant as it can assure to be a millionaire afterwards. I’ll start taking care my 401k more seriously and make sure I become successful at being a millionaire. Thanks!

Brilliant!? Wow, Kelly called me brilliant! All is good with the world! Wink.

Great job Fritz! It’s good to see confirmation that saving steadily over long periods of time, and compound interest, really does work. Even though you’ve been through the dot.com bubble & crash and the Great Recession, investments come back. “Staying the course” as they say over in Bogleheads really does work.

Appreciate you mentioning the “Corrections” in the market during the timeframe shown in my chart. I always “maintained the course”. Always investing, always Dollar Cost Averaging, never withdrawing.

Yep, it works. You just need time. And patience!

Wow, I can hardly believe our similarities. I think I was just a year ahead of you but two incomes may have been the difference. You are so right, Networth is all that matters.

automate savings has helped me. it’s true if you don’t see it, you forget it. Networth is all that matters not the fancy car.

At 37 I am at $81k between 401k and Roth IRA. I started at 33 When i received my green card. I know I can catch Up so I am going a full speed ahead with maxing both accounts!

Congrats on hitting that 401k million. It’s a nice thought to be able to retire at 55 and your wife was even luckier by retiring at 31!

Congrats, Fritz, on the impressive investment performance. That’s all through 3 U.S. recessions and countless market corrections. I always have to shake my head when I see folks give up on investing after one market correction. If you keep investing, even and especially through the downturns you see the real magic happen, see the chart above!

Cheers everybody and have a great weekend!

Haha AGREED.

What a powerful story! Thanks for sharing what our end results could be.

How do I become a member

I love how you attribute getting out of your comfort zone and finding a good mentor as keys to your success. A lot of people are risk adverse and it’s the risks that truly help you grow and often lead to the biggest rewards. Same goes for mentors – no one has to got at it alone and a good mentor loves helping as much as you appreciate the help. Pay it forward. I’m seeing this now with my own employees – I just really like helping them succeed. I love seeing them excited and passionate about learning new things. I also encourage them to take risks. it’s a win win for them and the business. As im sure your mentor saw as well. Everyone needs a mentor no matter how successful you are there is an infinite amount of new things to learn. Stay curious and your salary will grow – one of my employees just double his salary in 2 years!

Fritz, those early salary gains paid dividends even beyond your investing gains. Thanks for sharing.

I’ve come to the conclusion that some of are blessed with the ‘toy adverse’ disposition. Whether it was from growing up with little or nothing (me) or just being born cheap it is just the way some of are.

There was a point in my life when I realized if we didn’t want to worry about that dentist bill, the tires on the car, an oil bill or any of the thing life throws at us we a pile of money. It occurred to me I needed to save and get serious. No we didnt have a sit down talk about finances the Mrs was frugal from the ‘get go’.

1) I became the plumber, carpenter and handyman

2) She became the painter and coupon clipper extraordinaire

3) Entertainment became $1 movie rental and take out Chinese or pizza

4) Windfalls like bonuses were 90% saved

5) we bought practical cars and drove them forever – witness my 130,000 mile CRV that the son is driving today

6) Or cardinal rule NO DEBT.

Lunch often came from home with home made bread.

My Passion is a inexpensive fishing rod some bait and time in the sun. Hers is varried and includes quitting, and deal shopping. As time went on the pile allowed for vacations in sunny places but the saving never ends…

Doesn’t get much better than that :)

This advice is GREAT! The first year out of college I definitely lived above my means. I had never seen that much money in my life, and all I knew what to do was either put it in a simple savings account or spend it.

Fast forward 3 years and my fiancée and I now contribute the MAX to my Roth 401(k) and our Roth IRA’s so that we can learn at a young age how to truly live below our means. The crazy thing is that even after maxing out our retirement accounts, I still feel like we live a good life and have a great time! When you never see the money, you don’t ever worry about it. Then it’s always nice to check your retirement accounts at the end of the year and see how compound interest took affect:)

Hell yeah man – you’ve figured it out early, with plenty of time for it to grow now! You’re gonna be all set!

Thanks for the advice sir. I was thinking about when I get a raise put 2% in my pocket and invest the other 1% in my 401k and capping it at 10% with a 6% match from my company; this totaling 16% annually! Thanks to your update I realize that I’m getting older and should be more aggressive. Going forward I will do 2% in 401k and keep the remaining 1% in my pocket. God I wish I knew about you guys when I was 18 years old. I’d be a decamillionaire by now! lol

Haha… all that matters is that you’re here now and making moves! Keep inching those %’s as time goes on and you’ll be sitting pretty :)

Low fees are very important. The other SUPER important 401k rule is be involved. While contributing 10% I missed a notice of investment changes and my balance and future contributions rolled in to a cash account with basically zero growth for a long time. I’m contributing 16% now, but it doesn’t make up for the lost compounding time.

Everytime I think about that mistake i sigh knowing I’ll be working until I’m 60 when I could be retired now!

Ack, great tip! If only it had gone to cash during a market crash!! :)

This is really a powerful story! Since there are no 401k plans in Germany, I haven’t really had any contact with them yet. But one thing is always the same everywhere: If you start early, you will have more of it ;-)

Yep! Financial best practices are universal. Invest early, invest often!

Your post is amazing. I have started early in my 22 years. I have some savings and investments. It is growing a little bit. Each and every month I am investing on stocks. While starting it looks like too small. But now I have a little bit higher amount. I am also increasing multiple streams of income one by one. Thank you so much for this blog post.