Got a quiz in my email this morning and thought we’d have some fun with it :)

Hi Jay,

We’ve used checking account balance data to develop a quiz that ranks your checking account balance relative to your peers in the US. We also tell you know how much banks are earning from you. Check it out:

https://www.hibenjamin.com/blog/quiz-rank-checking-account-balance-vs-peers/

I thought your readers would find this interesting.

Thanks,

Mark

I checked it out, and by jove it was interesting! And you don’t even have to enter your email at the end to see the results – imagine that? You just answer two simple questions and you’re good to go…. (both of which you should know by heart, though I’ll give you a pass on the 2nd one so long as you get the first one right ;)):

- What is your age?

- What is your household’s checking balance?

Then hit submit, and voila!

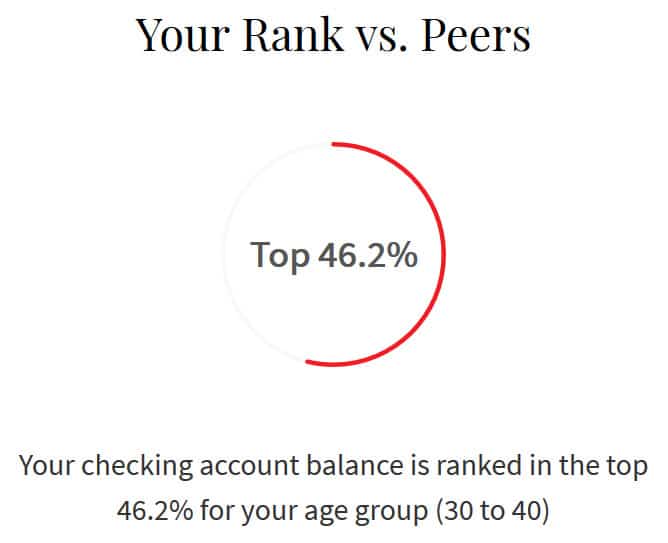

Here’s what it shot back after putting in my own info:

And here’s what I plugged in, since you know – we’re all about transparency ;)

- My age: 38

- Our household checking account: $2,091.66

Of course, on its own these stats don’t mean much since people stash their $$$ in all kinds of different places (you could have $5.00 in checking but $5 Million in savings! Or $0 in savings and checking, but $500,000 in investments!), but still kinda neat to see I suppose…

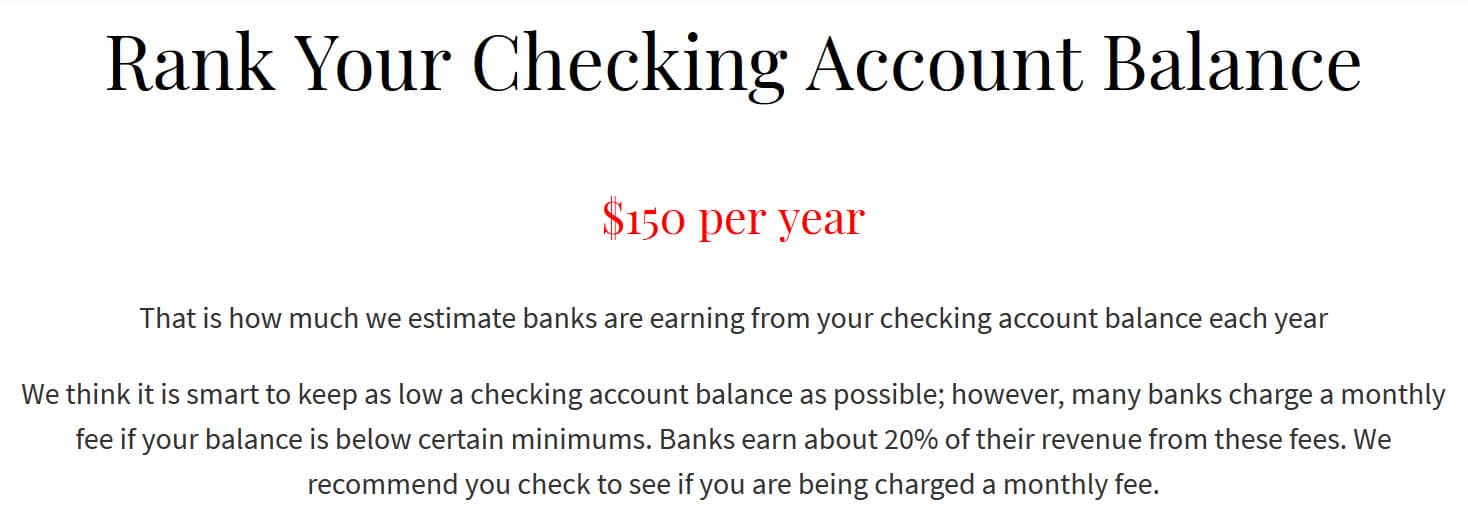

As for the 2nd promise of the quiz on how much banks are *earning off of us*, clicking the “next” button will get you to that screen next.

(Though FYI you have to look closely down towards the bottom or else you’ll miss it like I did the first time around… Also be sure you’re only entering dollar amounts and not the change in your checking account or its liable to inflate your #’s which is also something I goofed on the first go at it ;))

Here’s again what it showed for me:

So apparently USAA makes $150 off me each year :) Hope you’re enjoying it, guys! Haha… But honestly, that’s great news. They SHOULD be making money off me so I can continue enjoying all their free services! I’d even PAY them $150 a year if I had to to keep my accounts, haha… I absolutely love them!

Obviously not everyone feels the same way about their bank, so perhaps if this number pisses you off it’ll force you to act and move it elsewhere :) Though spoiler alert – this is how banks make their money: by using YOUR money while it’s just sitting there doing nothing.

So I won’t be changing up my game plan anytime soon, however I will say it’s INCREDIBLY fascinating seeing how much *others* keep in their checking accounts from all their data this company’s collected.

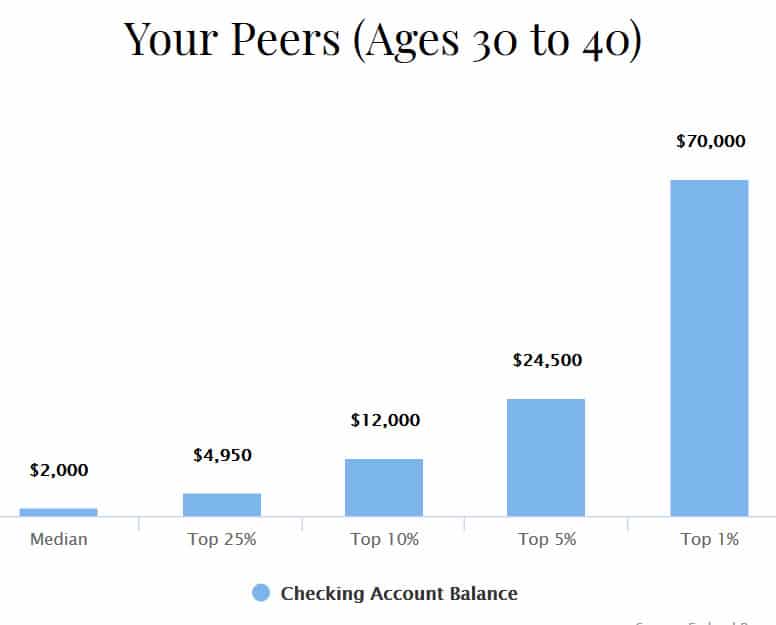

Check out this clip from that same quiz post:

We studied data on individual checking account balances and, unsurprisingly, there is wide variation in how much money people keep in checking accounts. On one hand, there are the 30 million households that have balances of less than $1,000 dollars. And on the other extreme are the 200 households who keep more than $20,000,000 in their checking account.

$20 MILLION DOLLARS!!!! IN A CHECKING ACCOUNT! Can you imagine?

Good for them for amassing so much, but wow… That’s a looooot of money being parked making verrrrrrrry little in return, man… At least move some of that money over and get it invested, right? Or maybe they are, and $20,000,000 is comparatively the same to our checking accounts because they have $200,000,000 parked elsewhere? Wouldn’t that be something?! ;)

Unfortunately we’ll never know the real reasoning behind it, but just to keep me sane I’m going to assume that’s the case because if you’ve managed to get $20 mil banked you’re probably smart enough to know what to do with it :) Or perhaps they finally realized they have enough and are now perfectly fine living off the interest? Because any % of $20 Mil would be more than enough to live off for decades/ generations to come!

But outside of gawking, there is another reason for me posting this up today. While I am curious to see how much you guys are keeping in your checking accounts, I’m more interested in knowing the “whys” behind it. Similar to our millionaire friends above.

- Do you keep a lot in there because it makes you feel comfortable?

- Do you keep a little in there because you prefer maximizing your returns instead?

- Or are you somewhere in the middle – like me – who probably has more padding than needed, but still devotes a bulk of their money elsewhere like with investments?

We typically always keep between $1,000-$2,000 in our checking just for padding, which I don’t think is too much, but on the flip side we have wayyyyyyy more than we “should” in our savings account right now ($90,000+). Mainly because it’s a nice change for us to see (I always recommend holding onto cash when you come into a large amount, just to let it all soak in!), but also because I’m self-employed and now have like a billion babies to feed ;)

I know others though that have maybe $100 in their checking and $200 in their savings, but every other dollar maxed to its gills because they can’t stand their money not working for them!

No right or wrong paths here, but only if it’s all being done by design and not out of laziness or lack of thought :)

And I have to re-share my post here on how you DON’T need every last dollar maximized in order to “be good” with your money, btw. In a perfect world that would be nice, but we don’t live in perfect worlds and we’re all different creatures with all different emotions. So again, it’s a matter of lining up what best works for YOU, and not necessarily doing things just because others say it’s “better.”

If you’re not happy with your situation though, or curious to see how others are managing their money, then keep your minds open and hopefully the comments today will help you put things in better perspective!

Which is my ask of everyone reading this today: Will you share with us how you manage your money when it comes to banking and systems? How much is in your main checking account right now, and is it by design or default?

Quizzes are fun, but they’re even better when there’s a point attached :) So share your juicy #’s with us today and help us learn from them!! Especially if any of you are sitting on $20 MILLION!!

*******

PS: For more quizzes with and without points, see below:

- What Kind of Saver Are You?

- Could You Pass This $$$ Quiz?

- How Serious Are You About Early Retirement?

- QUIZ: How Broke Are You?

Get blog posts automatically emailed to you!

Omg $150?! That’s about 7.5 percent interest! I’m considering now moving all my checking account money to my savings account at the very least…

Also, pretty surprising what percentile you’re in for just a few grand. It’s alarming for our nation.

Guess it’s the money multiplier allowing them to leverage checking account capital?

I’m not sure *how* they use our money, but they’ve certainly figured something out, haha….

They turn around and lend it out to other customers as mortgages, business loans, farm loans, auto loans, etc.

I have my system down that I just keep enough in my checking account to cover my mortgage and my credit card bill, both which bill on the 1st of the month. The first is fixed of course but the credit card bill I have to track, which forces me to track my spending. Any excess goes into my real investments

Wow, I didn’t have to read too far into the comments to find someone with the exact system I have. Mortgage is the 5th, credit card on the 6th, just in case my direct deposits hit a snag.

My bank doesn’t charge for being under a minimum balance, but I try to keep an extra $100 in case of math errors. I’d rather have that $100 not working for me than make a math error and pay a $39 overdraft fee.

Amen to that!

It will vary depending on the time of the month as every week has something that is budgeted to be paid out. I could have anywhere between 500 to 3500 sitting in it. When it gets above 2000 then for me its time to start thinking where I want to put it or is there something that Ive been putting off that needs attention, ie home maintenance usually.

I dont use a bank but a credit union. They started charging a monthly fee a couple of years ago but if you do a couple of thing such as use your debit 10x month / pay online with their bill pay system / have direct deposit …. etc then you get your fee returned to you. For me its $6mo but I use almost all the features other than being over 55 and having a high mortgage so I get $6 back and then some.

90k sounds like a lot but to each his own. I keep 6 mos emergency in it, the annual insurance fees and a general savings account that fluctuates. (for when I have the I WANTS and cant wait lol). All in all I keep it around 50k. Anything above that goes into IRA / investments.

So for the test at my age its: Bottom 26.5% (Your checking account balance is ranked in the bottom 26.5%. This may be a smart move.) It also says $150 a year, hmmmmm… lets see 6×12=72 if the accounting wasnt a wash..

Median is 2300 / top 1% is 110000.

Credit unions are dope – all “owned” by its members and focused on the local communities. If I weren’t w/ USAA (also dope!) i’d be with a credit union :)

I keep a pretty low balance in my checking because I like to create a false sense of scarcity that prevents me from spending money needlessly. Right now there’s about $450 there but I have a check coming out for $320. When I get paid, I’ll add up what needs to come out, leave a $50-$100 buffer in case I forgot about something, then put the rest in savings or towards debt. I use a credit card for groceries/gas so I just pay that off once or twice a month.

YES!!! Great idea! If you can’t see it, it’s harder to spend :) That’s how I tricked myself into investing early on – I knew that once it was in my retirement accounts I couldn’t touch it so I moved as much as I could over and then made do w/ what was left in my checking/savings… I’ve heard of people opening up bank accounts across town to automatically divert money over too, and then not getting debit cards or signing up for online access so not only do they not see it pop up in their daily routines, but it’s also super annoying to go get money out because you have to drive all the way over! Haha…

Yeah my savings is with an online only bank and I don’t have a card so I only transfer money if I need it and it takes a few days. I’m not quite at the point where I can invest heavily as I have student loan debt but when I have more funds I’ll allocate more directly to my 457b.

There’s more in our checking account than our savings account. At all times there’s about $5000 in there, for expenses and the mortgage.

Is that chart accurate? The 1% (30-40) have 70k in their checking?? Ummmm…geez… You don’t have to maximize every penny but… whatttt.

Checking is about $500, savings about $3500, the rest invested.

I put all my pay directly into savings (after my investments like my HSA, 403b and 457 come out) and then transfer over my monthly budget before paying bills at the beginning of the month. During the year I’ll let savings grow so that in January I can max those IRA’s.

If I am planning a major purchase I’ll cut back my investments and let savings grow a little faster beforehand.

I like it :)

We usually spend our checking account down to zero each month, so at the end of the month we have very little in the account, but at the beginning we have more. I’m curious how the bank profits off of this money? Interesting post today!

The way that banks traditionally earn money is by a spread in interest rates. If you have $100 in a checking account that earns .5%, the bank will in turn loan that money out at say 2%. These days, banks make money in plenty of other nefarious ways, but that’s been the bread and butter for a long time.

I used to be in that top 1%. I was young and stupid. I maxed out my 401k and did’t know what else to do. I knew not to spend it, and everyone I knew (“responsible” adults included) encouraged me to spend it, so I just let it stack up in my checking account.

Then someone at the bank suggested a money market account, so I did that, and then I heard about Wealthfront on a podcast. I wish I had heard about Wealthfront years earlier. I would have made much more money.

I would say you won pretty good there already by *keeping* all that money over the years! That’s the hardest part of the battle – having the money to then invest/etc! So yeah- sucks it wasn’t earning as much, but could have def. been worse if you listened to all those “responsible” adults :)

We have about $8300 in checking together… (wife and I still keep separate accounts!) After maxing out my 401k and then finally hitting my 6 months of expenses in my savings account, my good spending habits have now presented me with the great problem of having more money than I feel I should have just sitting in my checking account. Need to figure out how to make it work for me before I spend it on something stupid like a turbo for my daily driver…

Edit: I’m going to look into this ‘Wealthfront’ thing that the person above me just posted… sounds like i’m the young and stupid guy that G used to be! haha

HAH! Good!

WealthSimple is another one to take a look at too who we’ve covered here before: https://budgetsaresexy.com/wealthsimple-review/

Also Betterment: https://betterment.com

Wealthfront sent out a survey this afternoon asking what I thought about them opening up savings and checking accounts as part of an online bank. So be looking out.

I put in a different number and it also told me $150 a year, so I’m not sure how scientific it is.

We currently have enough cash in our joint account for three months of expenses, daycare, and mortgage.

We are trying to up it since we are having our second baby in about five months. The only other reason why we would have so much cash in our savings account is to save up for a down payment.

Very very smart (and congrats! :))

Like a lot of people I keep enough in my checking for rent and regular monthly expenses. Everything else is in savings or investments where I’ll get a bigger return!

I guess its definitely all relative though, if I had $200M I don’t think I’d worry about having $20M in a checking account either! ;)

Wow. That’s quite the spread. We keep about $25k in our checking account. This is a recent change from our usual $1k. Our credit union gives us a 2 percent return on our checking up to $25k. So we now keep our emergency fund in our checking.

Wow – that’s really really good!! Can’t say i’ve ever heard of a place offering rates like that for checking?!

We have about $4500 in our checking right now. That amount fluctuates a bit, but we keep a little buffer in the account. The rest of our cash is in a separate savings account.

I keep about a month of expenses in checking. It’s not the most efficient method but keeps me from having to check if there’s enough to pay the next credit card payment or mortgage. All my bills are on autopay so no time is dedicated to managing cash each month. That time savings is worth the “lost” interest to me right now.

I would agree with that :) The less you have to think about your money, the better (so long as it’s all going *UP* over the course of time, of course, haha… Otherwise you’re just like any other person in our country ;))

This is a difficult time to answer the quiz because most of us are lining up money to pay taxes.

Anyway, I do agree with J Money… I really hope that banks make some money because in return I can use a number of features all free.

I don’t pay: 1) debit card, 2) wire transfers, 3) maintenance of the account, 4) payments.

So please make some money, I don’t mind.

:)

I average about 1-2k but have been known to dip to near 0. This is by design. All money in its place keeps idle hands from spending it.

It’s really interesting. Two of the tips that comes up over and over again in personal finance articles is to “pay yourself first” and to automate your savings. For me, that’s exactly what I do. The day I get paid, I’ve got money automatically going to my RRSP, TFSA, emergency fund and mortgage (including additional payment). The rest is for day to day expenses (food, entertainment, etc.). If I’ve got leftover at my next pay day, I’ll direct it to one of my savings accounts (TFSA, RRSP, emergency) depending on what needs it the most and where I have room.

It’s a beautiful thing!

depends on the time of the month, right now $1500 in checking, I leave about a G for buffer. In savings, I have the $5 minimum my bank requires. I figure if my emergency needs are more then $1K than I just charge and address more fully the next month before I have to pay interest.

Combined, my wife and I have about $6k in checking accounts and about $43k in savings. 80% of the latter is our emergency fund, good for a year if we’re tight; the remainder is money we’re casually stashing for home improvement and vacations, which increases at around $500/month.

Maxing out 401(k) plans and our HSA comes first — we don’t invest beyond those. Any windfalls (especially non-taxable windfalls) go into our Roth IRAs, which some years get funded and some years don’t.

Gotta love that $500/mo increase!! Must feel pretty good :)

Thanks for the thought-provoking post!

I put enough in our checking account to cover our monthly budget. I also like having extra so that I don’t have to worry about overdrawing.

However, our checking account is currently over $17K which is pretty high. I do get 0.60% interest on our checking account which is not bad but I could get much more interest in a savings account. Hmm…I need to think about this more. I’m leaving money on the table.

What about maxing out 401k/IRAs for a while and then going back to saving more? so you can keep your stash there, but work on other goals since you don’t need to throw in more?

I keep at least one month of my net pay in a checking account (around $6,000). With CDs and MMA interest so low, there’s not much incentive for moving a few thousand in them. Besides, nobody ever got rich from bank accounts besides the bankers themselves.

On a separate note, I’ve read somewhere Floyd Mayweather keeps $123,000,000 in a checking account :)

Somehow that doesn’t surprise me w/ that guy :)

I have about $1100 in there right now, which is high for this time of the month (I get paid the last day of the month so it always goes way up then). Generally, what’s in there is what’s in my “spending” budget, including sinking funds like car repair and travel. I haven’t used those funds for a while.

How about $223,000+ in a near zero interest checking/savings account? Yes, it just sits there waiting for the (Fi) RE plan to be executed in December 2018. It didn’t just land there in one chunk. It started snowballing due to annual bonuses and taking stock profits from investments that I held for over 20 years. Cash deposits grew faster than my plan to re-invest it. I also no longer needed to cover college tuition for the kids when they both graduated.

No, I didn’t foolishly try and time the markets, I reached my own saturation point of profits and took them. Yes, I left some money on the table in my taxable accounts. My 401k and IRAs were getting fully funded and maxed out for years and they are still riding the market.

The taxable account profits are gravy money that did not go back into the market. For me, I determine the value of the cash that I have on hand. The investments currently have in the markets are determined by analysts and traders. Come a day they will decide that they will lower its value and start selling. Last week was an example. When the tide is high and the markets too, everybody is counting their CAGR. Last weeks correction is the trigger for me to go shopping for a few bargains. I have some cash to play with.

Why do I keep so much cash? I have enough cash on hand to live off of for the next 5 years. The stock market can do anything thing it wants until I may need to start siphoning off cash in 2024. I sleep very well.

Essentially, I will have near zero AGI when I sign up for the ACA medical plan in 2020. I get a significant subsidy and for once, I get to tip the tables toward my balance sheet.

The White Coat Investor and ESI Money both wrote that if you’ve won the game, stop playing. That’s what I did. It took two years to screw up enough nerve to stop playing.

It takes a lot of courage to stop playing especially when the market continued it’s run.

As member of the FI community, the FOMO was running through my head. At times, I felt pretty stupid as I could have had 12% more.

I’m sleeping pretty good sleeping under a blanket of cash as I plan RE in 264 days.

Again, thanks for having coffee on line with me every morning.

Wowwww good for you, man! That IS hard to do – especially hanging around this crowd!

But you’re right – if you’ve already won, time to count your blessings and be happy with yourself. Congrats on “making it” and even more so on your impending retirement!!! You’re at where all of us want to be one day! :)

I think my online savings bank, Syncrony, makes a lot more. On 3/24 I withdrew $$ from my online savings account (transferred it to my local bank’s checking account). Syncrony immediately stops paying interest on this $$ on 3/24 BUT Syncrony emailed me saying the $$ will not go into my local bank until 3/29! So they hold onto my $$ a total of 5 days in this instance. If today was a holiday, it would be 6 days. These days wire transfers usually only take 24 hours so I’m sure Syncrony is making a lot more! However, they pay a higher interest rate than most other banks.

Forgot to say, we keep a $1000 cushion in our checking account for emergencies but tend to have a $2000 balance on average. The quiz said our bank makes $150 a year on us. That’s okay with us since our checking account is 100% free.

Haha yup, probably… I’ve heard good things about them too :)

I keep about $1,000 in checking for overdraft protection. I am retired and I have $ in a money market account in my Roth IRA at Fidelity that I can access in a day or two if necessary.

We have about $20,000 right now, but that’s because we’ll have to send the IRS about $15,000 in a few weeks. Once that’s done, I aim for around $10,000. That’s 2-3 months of expenses. Enough padding for me.

Yup – that time for quarterly taxes! We always end up overpaying throughout the year despite my best intentions, so hopefully it’ll be the same again and we’ll take a break from paying this quarter… The best kinds of payments ;)

In our joint account we have over $3,500 – we usually try to keep it over $1000 at any given time as a cushion.

In my personal account, I’m over $5,000 but that will drop once the first of the month comes. I try and keep just over $2,000 in my personal bank account – I’ve had my bank account for a long time so I don’t pay any bank fees if I keep $2,000 in the account. If I don’t, then I’m usually dinged for bank charges of $18-$19 per month. Every month I’m successful, I figure out what the bank charges would have been, and then save that money in one of my savings account. Yes, the bank gets to use my money, but the money I’m “saving” from not paying fees is earning more.

That’s some good “spavings” right there!!! Boom!

We keep about 2.5 months of recurring bills in a separate checking account. There’s 16k currently in the account – we live in the baltimore-dc metro area…expensive to live here but our salaries make it worth the high cost. Our discretionary account is usually less than 1k, as we do most of our spending on CC and pay it off before the bill comes due. That leaves us with 17k in checking.

We also keep 10k in laddered CDs for emergencies and 10k in a savings account to replace our roof in the next 2-3 years (the other half of a new roof is in investments). It’s more money sitting in savings that I would prefer, but it’s a number that keeps the hubby happy and we take that stance that the more conservative financial decision wins in our marriage.

Haha I hear that…. Your husband and my wife would get along pretty well :)

I work at a Credit Union (woot woot) – and with the stage I am in right now I try to keep a minimum of a $1,000 in there and chucking away at debt with working two jobs right now. Once I get down to just my mortgage I will probably build up a nice nestegg in my checking. The reason being the checking at the credit union I work at currently has a checking that has an interest rate north of 2% (currently 2.30% and rates trending up).

Amazing!!! Tell me you work the counter too and collect all those rare coins and dollar bills that come in??? (If not – will you save them for me?? :))

I’ve got about $9k in checking and another $6k in savings right now due to a combination of holiday gifts, bonuses, tax refunds, etc that I haven’t dealt with yet. I’m meeting with someone from Schwab today to get assistance with rolling over an old 401k and am going to discuss using some of that cash to max out my Roth for 2017. I should also just transfer some of it out of checking & into savings since that has a higher interest rate.

Good idea :) (And also a good problem to have!)

$450!

Lowest it’s been for a little while because I just paid all our bills up through April 4th and it all deducted by the weekend: childcare, CPA, mortgage, food/gas bills, flights for our summer vacation, all our utilities, my life insurance premium. It was a heck of an expensive month but we had it all covered, thankfully ;) I usually keep a few thousand in there mainly to cover any expenses through the month but everything else lives in a savings account.

I share your love for USAA so I don’t mind if they’re making some money off me without taking it out of my pocket, I’m not paying fees and somewhat lower interest on savings accounts are fine since I keep the bulk of my money in higher interest holdings.

We keep a base of $1000 in checking above bills. Interest is a little over 1%. Then around $500 in savings for maintenance type things. Our credit union gives 5% on the first $500. In Betterment we keep our emergency fund that’s giving us just under 5% interest. I also have put the kids college funds in money market accounts since they’re either in college or will be in a few months. It’s safe and compounds interest more often than checking accounts.

Man, those credit unions are on fire these days

Current balance is $40,000. Our bank (along with several others in the area) offers 3.25% interest on up to $25,000 in Rewards checking as long as you meet certain criteria (minimum debit card swipes, direct deposit, paperless statements, etc.). I made over $800 in interest last year (which is taxed, of course). Banks in my area need lots of cash on hand to lend out to farmers/business at higher rates, so they offer great interest to chumps like me who have so many sinking funds (vehicles, vacations, future home repairs, etc.) and am also completely buffered by at least a month (a la YNAB method) that I always have about $25-35k in my account. I make minimal interest above $25k but have a surplus right now waiting to make some home improvements. But, I AM looking for a better place to park about $10k that is technically an emergency fund, but would only be used after the $25k in checking is used, so doesn’t need to be terribly liquid. Will look into some of the resources mentioned above.

What area do you live??? :)

Rural Iowa. We love when local banks compete. They do a lot for the community…hosting tailgates for high school, handing out ice cream at Little League games. It’s a great place to live and earn interest.

I only leave $100-$200 in our checking account. Only because:

a) I like my money to be “working” so leaving too much money in an account that earns nothing stresses me too much.

b) Even though we have hundred of thousands on other type of accounts, having so little in the checking account makes me feel broke. And I need that pressure to keep my day job, otherwise I would be too tempted to quit (which I will one day but I am not where I want to be yet)

Haha… I hear that.

I usually have 3-4 months in our checking account but it’s currently at its lowest point because we just finished paying off our student loans and I got too anxious :) Now we’ll grow back to 3-4 months and potentially save for a second car on top of that.

Congrats on being loan-free!! That’s gotta help with that anxiousness! :)

All of our money, except for brokerage account and digital currency, is in multiple checking accounts. For the quiz, I used one checking account which put us in a 13% category. If I’d used our largest balance checking account, we’d be in the top 1%. This is rather amusing, as our household income is very low. I use checking for savings, and am not worried about what the banks make off of me – for multiple completely free checking accounts – but enjoy the triple digit dollar interest paid by Capital One. Was considering opening “savings” at Barclay since it is paying 1.5% interest, even higher than Capital One. I think you can’t really get accurate results/information unless your subjects conform to standard ways of financial management.

I want to know more about your digital currency :)

Well, I got a Coinbase account 4+ years ago, and never used it – until I saw that had I purchased Bitcoin when it was low-priced, I could be a millionaire today! I could have waited 4 years ;) I decided to purchase $1,000 worth of Litecoin based on a bit of reading and speculation, and then wanted to put a bit in Ripple XRP – however, Coinbase does not sell it. Had to get another account at Bitstamp, and then wait 4 months to have that account “verified”. At that point I did a transaction from Coinbase, so it involved no new money/gambling.

Very interesting! I like seeing stuff like this – thanks :)

We have about $22k in checking right now by design before a hefty loan payment and our monthly bills come out. According to the quiz, we’re in the top 1.4% of 18- to 30-year-olds. Not for longgg.

Thanks for sharing!

I have $22k in my checking a/c and this is normal. I have deposits coming in (payroll, expense reimbursement from business travel, monthly dividends) and I have credit card balance payments on auto-pay. There a constant churning in & out so I keep a high balance at all times.

“Your checking account balance is ranked in the bottom 3%. This may be a smart move.” :D

We had some extra expenses in this months, that’s why currently only 10$ sitting there. Often it goes like getting the salary, cash out, buys euros, payback mortgage, leave there as much as needed for the bills and other monthly expenses. I keep my money buffer at hand (you know that from my money map already ;)). Having a healthy amount at your checking account gives you peace? If you have ever read my hyperinflation story you know why it does not do the trick for me.

I have, and it’s super scary!! I’ve got a stash of those billions and trillion dollar bills from Zimbabwe too – just incredible!

As for checking, just enough to pay bills and a bit of padding for an occasional movie, dinner, etc. I did however keep most of my emergency fund in the savings account earning pretty much ZERO just because it made me feel comfortable. I thought about a money market, but again pretty much zero relative to my monthly contributions to it. However, I just now finally bit the bullet and took a large chunk out and put it into a conservative 50/50 tax managed mutual fund with an expense ratio of 0.09. I figured, OK, if its a true emergency (I get struck by lightning, leg bit off by a rabid crocodile) it will be there and I won’t care about the minimal loss if I need it soon. If I don’t need it for awhile, hey, at least I’m getting a conservative 5%-6% in the long haul.

Haha.. I like it. I don’t know what *truly* counts as an “emergency” these days anyways… Though certainly lightning and crocodiles count :)

I guess it’s time for me to move some money into my investment account! Good reminder.

I’m at $6k right now, and am getting paid Friday. I keep several thousand in my account to cover work expenses – just in case my reimbursement comes in after the credit card bill. But thanks to an improved work expense process, that hasn’t happened in years. So perhaps I’ll move $3-4k over today. :-)

I usually keep up to $10K in my checking amount and since we have our paychecks deposited into there I usually transfer money to my savings account or one of my investment accounts if it goes over $10K. Don’t want to have too much in there because like you said your getting that I’m not getting much of return.

And the money in the checking account goes in and out. Along with the paychecks, we use it to pay our bills and rent. So it’s pretty much standard use for a checking account.

As for the main checking account…a few hundred bucks. Certainly by design. In my financial system, I use a total of 7 accounts (combo of checking and savings). The main checking is used for day to day expenses, such as gas and food (and maybe a few PF books :-) ). No need to keep a bunch of money in there. I used to freak out when I had $100 of less in my checking account, but with the system I now use, having less than $100 right before payday is a good thing…it means funds were allocated appropriately :-)

You’ve become a master :)

“Your checking account balance is ranked in the top 8% for your age group (40 to 50)”

We’re actively looking where to keep said money instead of in our checking. Already contributing to several tax-deferred accounts and Roths, but need a post tax account for money to sit.

We have $2,000 in our checking account in order to get the account free. Otherwise, every dime that comes in immediately goes to online savings account (for short-term) or to Vanguard. I probably over-optimize but, hey, everyone has their vices :)

Hah yeah – a good “vice” right there indeed ;)

I keep the bare minimum and it’s usually down to less than 100 right before I get paid. I try to figure out my budget to the penny ahead of time and I’ve gotten good at it. I take 50% of my income, invest it right away, and pretend it doesn’t exist. Treat each day like I’m starting over at $0 and challenge myself to hit 1k

50%!! So beautiful!!