This is an interesting topic I keep stumbling across lately :)

Tons of new research is coming out on how to gauge the creditworthiness of people who don’t have credit scores or any other type of financial history – or even bank accounts for that matter (think, underprivileged countries) – however they all do have one major thing in common – smart phones.

So a group of startups and app developers are starting to pinpoint the key data points that would help lenders decide whether someone can be trusted to pay back a loan or not.

And as Shivani Siroya noted in her Ted talk I just watched last night (look at me go – watching smart people’s stuff!), this is huge for a number of reasons:

There are 2.5 billion people around the world that don’t have a credit score. That’s a third of the world’s population. They don’t have a score because there are no formal public records on them — no bank accounts, no credit histories and no social security numbers. And because they don’t have a score, they don’t have access to the credit or financial products that can improve their lives. They are not trusted.

What a great way to harness all this new technology, right? Using it for GOOD!

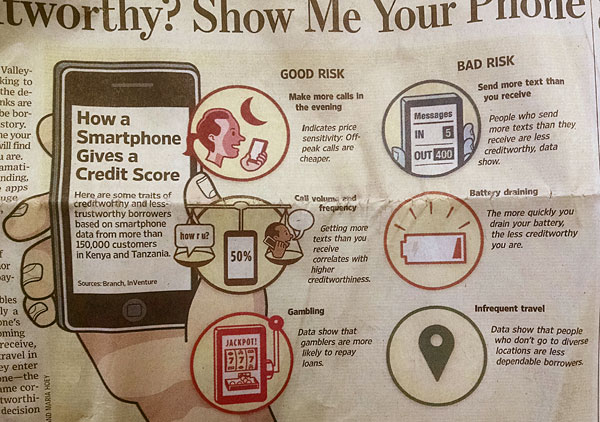

Good Risk vs Bad Risk Through Data Points

After watching that video, and then reading a similar article in the Wall Street Journal a little while back (where that graphic up top came from – crinkled up in my backpack waiting to be released one day!), I’ve compiled a handful of the more prominent findings here so you can see what they’ve uncovered.

Keep in mind these are just a few of the literally THOUSANDS of data points they’re collecting – but they’re some of the best ones. See where you fall :)

- Making more phone calls in the evenings than during the day – good risk. This indicates “price sensitivity” in that off-peak times are cheaper (keep in mind these are phone plans from international countries – not the U.S. where peak and off-peak seem to be going away).

- Sending more text messages than you’re receiving – bad risk! Data shows those who get more texts than they give out tend to be more creditworthy.

- Being a gambler – good risk!? Apparently gamblers are more likely to repay their loans – go figure. (Do people gamble on their phones?)

- Draining your battery faster – bad risk. ‘Cuz you’re goofing off too much on it? Or not organized enough to keep it charged?

- Consistently communicating with a few close contacts – good risk. Gives you a 4% bump in worthiness :)

- Having a pretty regular travel pattern – good risk. Data shows a 6% increase in repayment among customers who are consistent with where they spend most of their time. And I’d imagine if one of those places is “work” it’s even higher ;)

- Communicating with a variety of different people a day – good risk. People who interact with more than 58 different contacts tend to have stronger support networks – and thus be more likely to be good borrowers. Giving you a 9% boost in creditworthiness.

- Not paying your cell phone bill – BAD BAD BAD!!!! Haha… okay, so I made that one up ;) But for real – that’s gotta be in there somewhere, right? Or maybe everything’s pre-paid in those areas? (Actually, that’s probably right… if they have no credit history of course they don’t have bills, d’uh.)

So maybe it’s hard to compare your own data points with those in other countries, but if someone ever did task me on researching such things here in the U.S., here’s a list I’d provide them totally free of charge. And I wouldn’t need a phone to figure it out ;)

J. Money’s list of variables in determining creditworthiness:

- How much TV you watch every day

- If you know what the word “side hustle” means

- If you track your net worth

- If you read Budgets Are Sexy

- If you know who Dave Ramsey is

Credit Karma needs to appoint me their CEO ASAP :) And shameful plug as an ambassador* of theirs: they’re a great place to grab your credit score and report – for free. CreditKarma.com // end plug

All joking aside, these findings are HUGE to the billions of our world who have always believed there’s no hope for them within the financial industry.

I remember reading an article by Bill Gates once about how mobile banking is helping the poor transform their lives, and I feel like we tend to take it all for granted here. People would jump at the opportunity to improve their lives/businesses through access to capital, yet we over consume it to the point of being detrimental to our health, ugh… Could we just send them all our *excess* credit, please?

Anyways, just thought you might find this as interesting as I did :) I’m sure it’s only the beginning of what’s to come, which is AWESOME.

Here’s that Ted Talk again if you want to check it out – it’s only 8 mins:

Happy Friday!

———

*I get compensated to be an ambassador for Credit Karma whose services I love and use personally

Get blog posts automatically emailed to you!

Interesting topic. I’d like to see the stats on the the people with no credit scores and if they where lent money based on their smartphone credit worthiness what where the % who paid back, defaulted, etc

Yup! Shivani touches a little on this in her talk:

“Our credit scores have helped us deliver over 200,000 loans in Kenya in just the past year. And our repayment rates are above 90 percent — which, by the way, is in line with traditional bank repayment rates. ”

Incredible, right?

Wow, 90% is amazing. Maybe P2P lending companies should adopt this phone monitoring scheme. Oh wait, how do they collect the data anyway? Probably need to work with the NSA here in the US…

Man, that was a cool little post. Love that I started my Friday with a little humor. Aside from actually knowing my credit score, I feel validated knowing my phone would provide a similar financial profile on me – except for the draining battery part. Major fail. I goof off on it too much. But I always have a backup mobile battery ready to go! That should definitely count for a few positive point, don’t ya think? ;)

I’ve just recently started to seriously track my net worth as a way of staying motivated. I published my first post about it today. I’m even considering submitting it to Rockstar Finance. Talk about holding myself accountable! Yikes!

Mrs. Mad Money Monster

Nice!! Let me know anytime and we’ll gladly add you up on it! Nothing helps you stay on top of your $$$ more than knowing you have to publish it to the world every month, haha… I’m pretty sure it’s helped me save at least $100,000 more over the course of my 8 years doing it :)

(And total bonus points for carrying a back up battery – that proves preparedness! I’ll give you back 5% creditworthiness for that.)

Pretty amazing what can be done with statistics and analytics. It’s like Moneyball for creditworthiness. Thanks for sharing!

Great post, it is good to get the perspective and see the challenges others face in getting credit. Just wait until “Lending Club Africa” opens up… :)

The Green Swan

Not feeling this…..I’m a landlord and the three top “challenges” I see in applicants are : 1.) Student loans – Folks take these out and many times do not finish their education….but they still owe the money. Because they didn’t finish they don’t advance in their career and earn more money. I have seen student loans payments that rival house payments. 2.) Car payments – When an applicant shows up in a new car my heart sinks….And when they say ” I just had to have it”….”we’re toast”…. I have seen car payments that go 4 figures per month and can’t count how many folks are “upside down”. 3.) Cell phones – My rule of thumb …. “the larger the phone…..the poorer the credit score”. In addition the more attentive one is to their cell phone the less desirable the client. This is a communication device….not an infant that needs to be attended to. I have seen cell phone bills that exceed electric bills. And true these folks “have everything” with their service….but then again they may need it …..as they may be living in their car…

“I have seen car payments that go 4 figures per month…”

I would have a heart attack. If it’s that expensive of a car, any work that needs done isn’t going to be cheap (my pockets are crying). I don’t know anyone that has one that large, but I wouldn’t doubt it. I know a lot of “just had to have it” people (even if they have 10 of the item, they just loved the color/blingy-ness/new-ness/”my friend has it so I have to have it, too”-ness of this one).

Never thought about the size of a cell phone. Interesting.

What happens with cars I’m told is that folks show up at the dealership ready to buy BUT their present car is worth less than what is owed against it…NO WORRIES….the dealer pays off the old car loan and then “rolls the balance” into the new car loan. After a couple of these you can see where it is headed….

I’d be interested in seeing how you’d size me up at a first meeting ;) What does ratty car + mohawk fair in your calculations?

I’ll admit I totally check out my rental applicants fb profiles! You can get a good sense of a person by what they put on their public profile. Things that count against them: Complaining and seeming like a victim of life, drunk photos and photos where they are flipping off the camera- especially if that is their profile pic and too much drama. (All 20 something’s: You are now warned. If you post stupid things on your profile, people you want to impress aka: employers or landlords, will see it)

Mohawks are fine. Bonus points for beards. =)

HAH! I used to be infamous for flicking off the camera all the time… I don’t know why we feel the need to do that, especially as a rather happy person, but I guess the alcohol does things to you :)

My beard waves hello.

I hear you. Ms. Financial Slacker does work for a real estate guy who is worth $1 billion plus and drives a POS beaten-down old pick-up truck.

Be careful using outward appearance to judge financial worthiness.

Hmmmm…..From what I understand J you choose to live life deliberately…to not “go with the flow”. History has shown me these folk tend to be my BEST tenants. They usually understand what is to be provided and what is expected. As for the “hair-style” … couldn’t care less. My concerns would be your student loan debt and if you are current…Pulling up in the “Franken-caddy” would be viewed as a gift from the heavens….NO CAR PAYMENT. And if and when you pulled out your cell phone to take pics of the place and explained to me the “stellar deal” you have landed….I’d know I had found my new tenant….Mohawk and all!

I do rock Republic Wireless for only $25/mo…. and it’s still a smart phone – woot woot!

Have to admit that I was surprised that gambling was an indicator of good credit worthiness, I would never loan someone money if I knew that they were needing it to feed a gambling fix. But if that’s what the big data says I’ll go with it. Is this just going to come out in underprivileged countries or would Americans have access to the technology as well because I would love to see how closely the cell phone data compares to the scores that Credit Karma gives.

This is a great article! Fascinating!

I’m finding these results suspect though. My credit score is top-notch, but they’d likely consider me a poor risk.

So let’s think of who even knows when peak hours are, rather than just going by generic minutes… Oh right, old people… Who generally have better credit than young people. (ok fine, I’m old, but not old enough to think about peak)

My battery drains fast, and I use lots of apps – GPS, audiobooks, night blue light blocker, music, chat apps. I feel like that’s pretty typical of young people, but completely atypical of old people. So again, old folks generally have better credit than young.

My texts in vs out are equal, since I am having a conversation with someone I know. Not sure what that means. :)

Consistent travel – that makes sense, it likely reflects steady employment and strong social networks.

It would be interesting to see the ages in comparison to creditworthiness for sure. In both the US and overseas!

This one is shocking for me…”gamblers are more likely to repay their loans” !!

That Jon Oliver clip you left at the very bottom of the article was a great watch. It is shocking to see credit agencies advocate for people to use credit scores in their application process, but then have literally no data showing a good credit score correlates with good performance. My favorite part, “a really great credit score MIGHT mean you’re perfect for handling money on the job…OR, it might mean you’re so perfect at embezzling money that you’ve never been caught!”

I just don’t know J Money…if I let them tell it, I’m not creditworthy because I send a TON of text messages as it’s my preferred method of communication. The only person I talk to every day is my mom. But my credit score definitely doesn’t reflect that. I guess I’m an anomaly, lol!

I must be an anomaly too, Latoya! I prefer email and texts and talk on the phone maybe once a day (and I don’t gamble!), but my credit score is good. Fascinating way to evaluate credit, for sure!

People talk about the unbanked in the world but I’m more saddened by the 100’s of thousands in the US who are unbanked. In low income and/or predominantly minority/immigrant neighborhoods, banks aren’t always common, and those that exist still offer pre-paid debit cards and advertise them for people to put their paychecks in (a bank should be offering a bank account only!!! Makes me angry). I had a coworker for the longest time who always cashed her paycheck. Luckily, she could cash for free at our job because it was a private school that often got paid tuition in cash. But I would talk about my financial goals with her, and I think it encouraged her to get a checking and savings account. And although she still had money struggles (single parent who was owed a lot of child support), she seemed to be doing better financially because she could better track her spending.

As someone who lives in the Bos-Wash region of the US, I’m always saddened when I go to the south and see title loans/check cashing places on every other corner and realize they are often the de facto “bank” in many neighborhoods.

AGREED! Those payday places are horrible, even though they exist because there’s a need for them :( You’re right in that most articles around this focuses on overseas than here in the U.S. too. I wonder if anyone’s applying some of these same cutting edge concepts to the underserved here as well, and perhaps it’s just not “sexy enough” to be covered in the media?

Interesting, I don’t even really understand how US credit scores are calculated (I get the basics but not how everything is weighted)

I would be curious to hear someone’s story about moving to the US from another country and the challenges of getting credit without a score.

I do use credit karma!

Here’s the weights that FICO uses:

– Payment history: 35%

– Credit utilization: 30%

– Length of credit history: 15%

– New credit: 10%

– Mix of credit in use: 10%

Thank you – good info

I’m a fan of your credit worthiness list, although it would probably reduce the availability of loans for most people (a good thing in America?). Great post and great TED Talk!

Interesting.

For the battery drain item, I wonder if that has to do with Internet access. For some, their phones are the only gateway to the Internet, which can drain a battery very quickly. I’m not familiar with Tanzania and Kenya, so I don’t know much about living in those areas.

“J. Money’s list of variables in determining creditworthiness:

How much TV you watch every day”

I read an article a good while ago that talked about number of TVs in a house vs the household’s “class.” If I remember correctly, poorer households had 2-3 or more TVs while richer households had, on average, 1 TV. I thought that was pretty interesting.

Indeed!

Lots of studies between TV watching across the spectrum..

Here’s one of my favorites from a guy named Tom Corley who studied the habits of the rich for years and then wrote a book on it:

“6% of wealthy watch reality TV vs. 78% for poor.”

Here’s an article I did on it along w/ other fascinating stats:

https://budgetsaresexy.com/2013/11/why-im-obsessed-about-rich-habits/

Very interesting. I appreciate your point about how we as a culture tend to over-use credit to our financial detriment, while others have no access to capital that could pull them out of poverty and open new opportunities. I think it’s a little creepy to be analyzing people’s cell phone use so much, but if it allows people access to new resources, it seems like it’s for the best. I know of some poverty relief organizations that use microloans to help people start small businesses, and their criteria for lending is based on completing training courses in relevant skills training and managing finances.

Love that!

I used to participate in Kiva.org a lot which is pretty good in this field too, though if I recall correctly they don’t help a lot of these folks where this cell phone stuff is being implemented… Not sure where the barriers are though?

Just paid off my purchased used 2011 odyssey took 2 years. Debt free except mortgage…FTMFEW, which will take optimistically another 11-12 years, Putting me at 45 best case scenario. Hopefully I wont need credit ever again at least that the goal.

Before anyone says anything about market returns vs payoff, etc… I know, and I don’t care. It more important to me to psychologically to own free and clear.

1) Had to google FTMFEW cuz I’m not hip enough, haha… love it.

2) Mental happiness trumps numbers for sure!

HAHA, that’s how I learned the acronym as well.. Which I guess makes sense since we are pretty much the same age.

Saw the headline, figured the article was going to say something along the lines of “I’m with Republic, paying $24 / month for two cell phones combined, must mean I’m good with money”, but I like this article even better. I’m going to use it to show my wife that I need to start gambling.

Hah! That one would have been just as accurate ;)

You can tell a boomer came up with that list because it mentions time of the day people make calls. Who makes calls anymore?! :P

hahahaha yes! It said I needed to make my comment longer, but I really just wanted to laugh in agreement. Is this enough characters?

That’s a very interesting study, correlation. What happens if you don’t own a TV at all? Does that give me 100000000% good risk points?

It means you love money :)

“Having a pretty regular travel pattern” This is terrifying. All those apps that you’re sharing your location with are probably selling them to credit companies now! Yipes! I know I’m not as good as I can be with all of my data even if I’m probably more selective than most (no thanks FB app, you’re not going on my phone).

Well if it makes you feel better, all these people in this particular case have to opt in to be traced :) But it’s definitely getting freakier over time for sure…

I wonder what kind of score I would get for my cell phone use:

50% of calls missed because phone is missing

7 voicemail’s never checked

20% of time phone has no charge

Only responds to 1 in 3 text messages (the rest I think about responding to, but forget before it actually happens)

No calls over 3 minutes because of constant interruptions from 5 kids.

Hum… I don’t think that looks like a 760 to me.

Haha yeah – you look shady! :)

J. I think I gotta use my phone more often to practice and to have those good risks!

As a non-gambler, socially awkward person, and infrequent traveler I would get a low score.

But then again, as far as gambling is concerned, does the stock market count? I gamble only when I win on average, so casinos are out, but index funds are not so bad!

Some of these criteria seem a bit spurious and flimsy, but in the absence of any other information, hey, firms have to go with what they can their hands on. Despite all the complaints about our sometimes defunct credit rating system (got a good laugh out of the John Oliver video) I am now greatful about our half-way objective, though sometimes inefficient credit rating agencies.

I think, that not having access to debt by not having a credit score is actually a blessing in disguise. In most western countries, were we have access to more lending organisations that you can count, what do the majority of people do? Oh yes, hock themselves up to the eyeballs with debt from an early age, and then spend the rest of their lives paying it off. In fact, if you take a person living in a ‘poor’ country with no debt, who works and lives within their means, however humble this may be, and compare that with Joe Average, living in a ‘rich’ western country, who mounts up thousands of dollars worth of debt over his lifetime, who is better off? It’s just a thought.

Financially wise that’s probably accurate – they have a higher net worth than the average U.S. citizen who’s riddled with debt – but not having access to credit in this specific case also means not having access to a host of OTHER – more important things – to live your life that we take for granted here too :( So def. a trade-off I’m willing to bet people would swap for.

That is definitely interesting, and agree there is probably an inverse relationship with the amount of TV watched. Time of TV watching would be interesting as well, as a lot of informational historically came on in the late and very early hours of the night. Now with streaming services, maybe amount of binge watching would be of interest.