Another day, another person’s money to snoop around in! Haha…

And this time along with some nifty MONEY NOTEBOOKS! The budgeting method of choice from our featured reader today – Amanda – which I just love for a number of reasons. First, anytime you *physically* track stuff it tends to sink in better!, and second – it’s always nice to see a snapshot from someone early on in their journey and not a millionaire success story that we tend to feature a lot here ;)

When I found out that Amanda used notebooks to track her finances I asked if she’d be kind enough to snap some pics for us, and she not only did that for us, but also included some of her backstory as well.

So here’s the backstory along w/ the pics!! Gotta love that cheetah one, rawr!

Hey J!

Attached are the pictures of my money notebooks. The purple one was the first one and the animal print one is the one I’m using now. I’ve included pictures from my first month of tracking and the current month. It’s amazing to look back and see how far I’ve come over the last 7 years.

When I started tracking my finances, I was living paycheck to paycheck with about 3 grand in credit card debt. Today, I have $17K in my checking account, $40K in my $401K, and I’ve paid off two cars since October 2012.

I know this doesn’t sound like a lot to most people, but considering I only make about $33K a year, I think it’s pretty phenomenal! I have been side hustling all along as well. I’m proud of myself! I’m so thankful I found MMM’s blog and yours! They’ve both taught me a lot and keep me motivated to continue saving!

Thank you,

Amanda :)

And she should be proud!! That’s a lot of growth w/ a salary of that size! Some people can’t pay off jack with three times that, so good on ya Amanda… Here’s to the next 7 years of kicking ass!

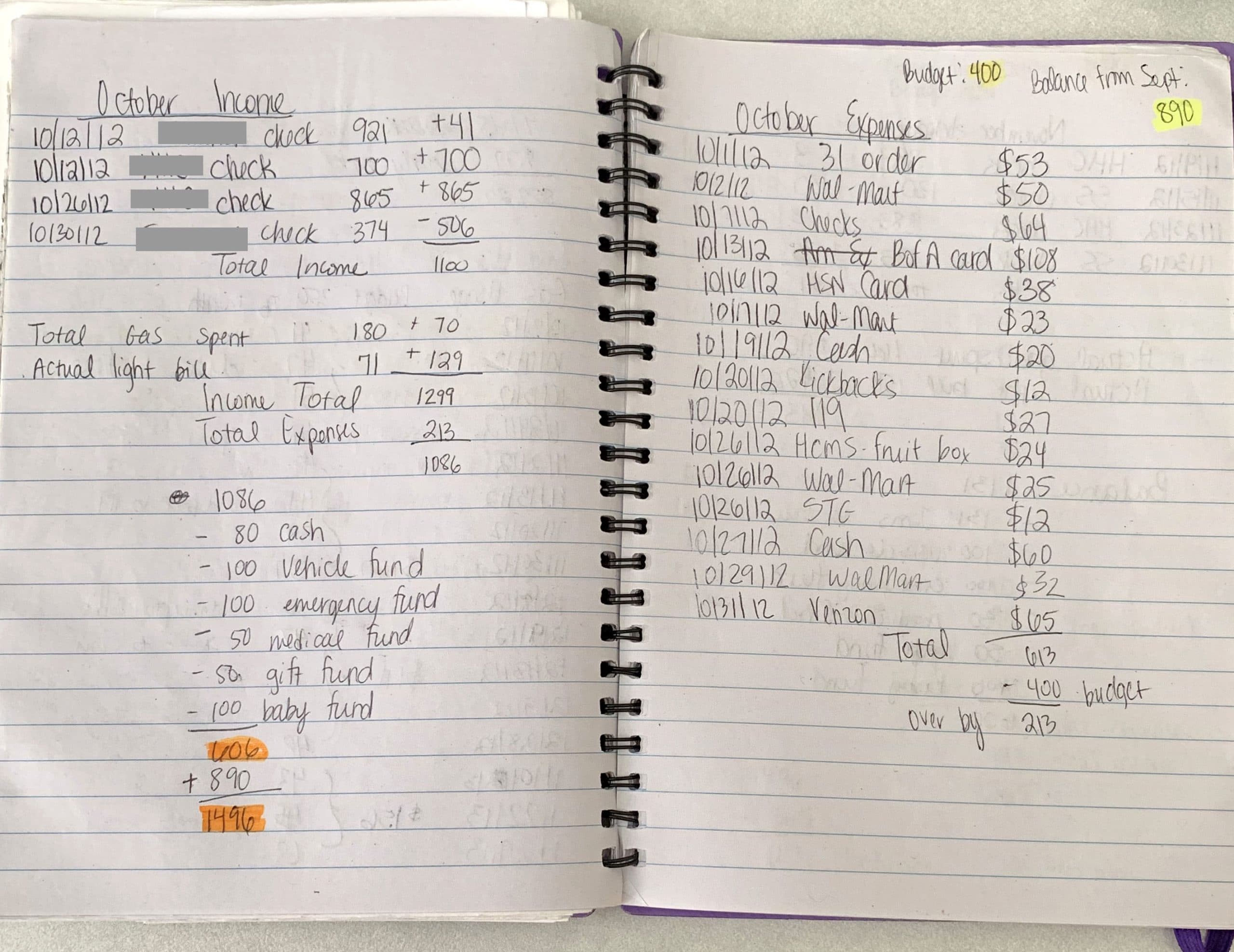

Amanda’s finances circa 2012:

[Click to blow up bigger]

You see all those savings funds???

- Vehicle fund

- Emergency fund

- Medical fund

- Gift fund

- Baby fund

A total of *5* for a whopping $400 every single month!! And again, all the while living off of a $33k salary, and probably even less since this was 7 years ago… (although the more I dig in the more I realize that rent isn’t included in there anywhere?! Maybe she’s pulling a “live with mom and dad to save mad money” deal there? A great one that I approve of during that stage of your life… Else you’ll turn out like me and waste away your money those first few years out of school! Haha…)

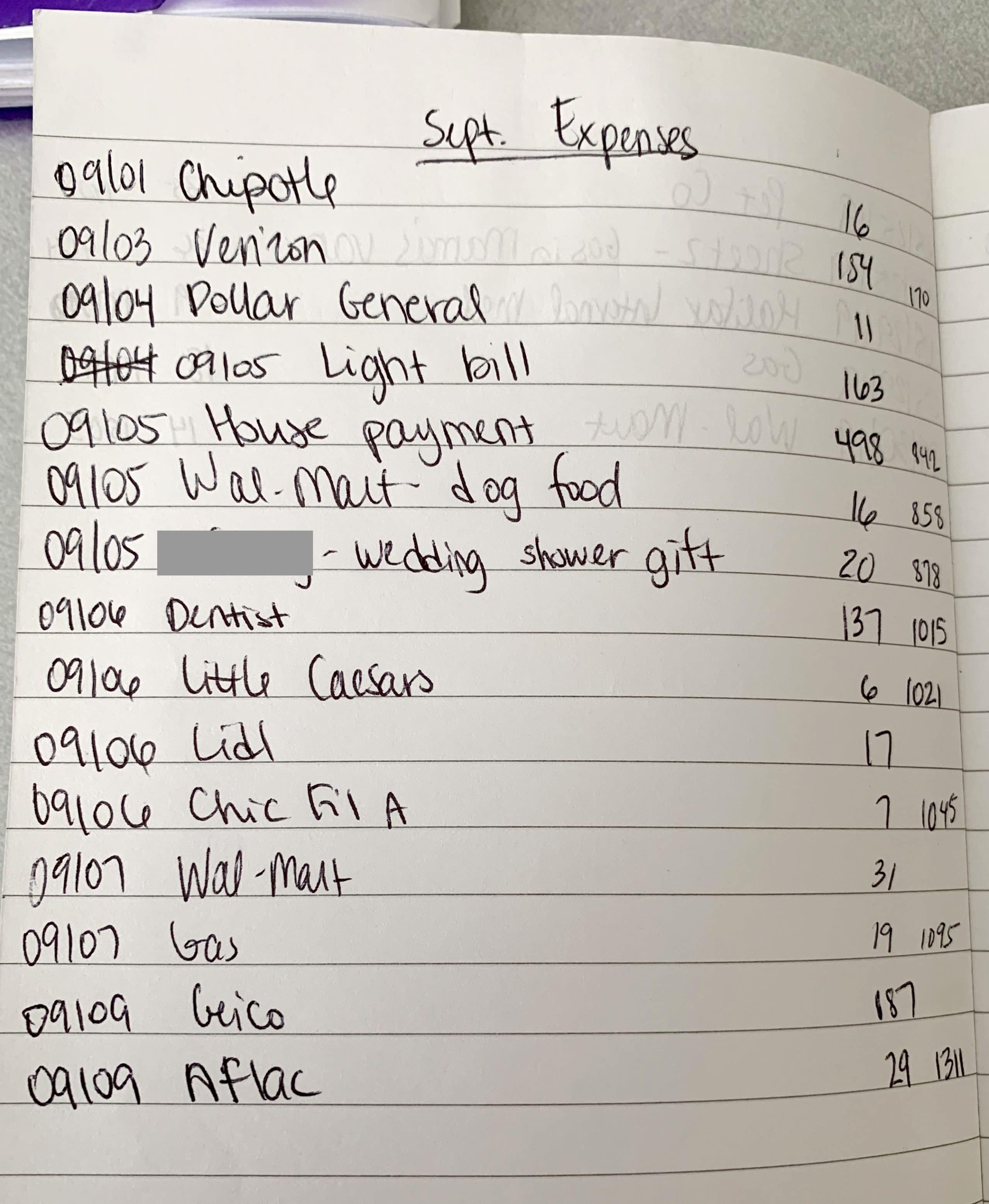

Amanda’s Expenses – Sep, 2019:

There’s the house payment! Lol… And not too shabby either at $500 – nice! We pay over three times that right now and that doesn’t even include the extra we throw against the principal… I wonder if she has roommates/partners she’s splitting the mortgage with?

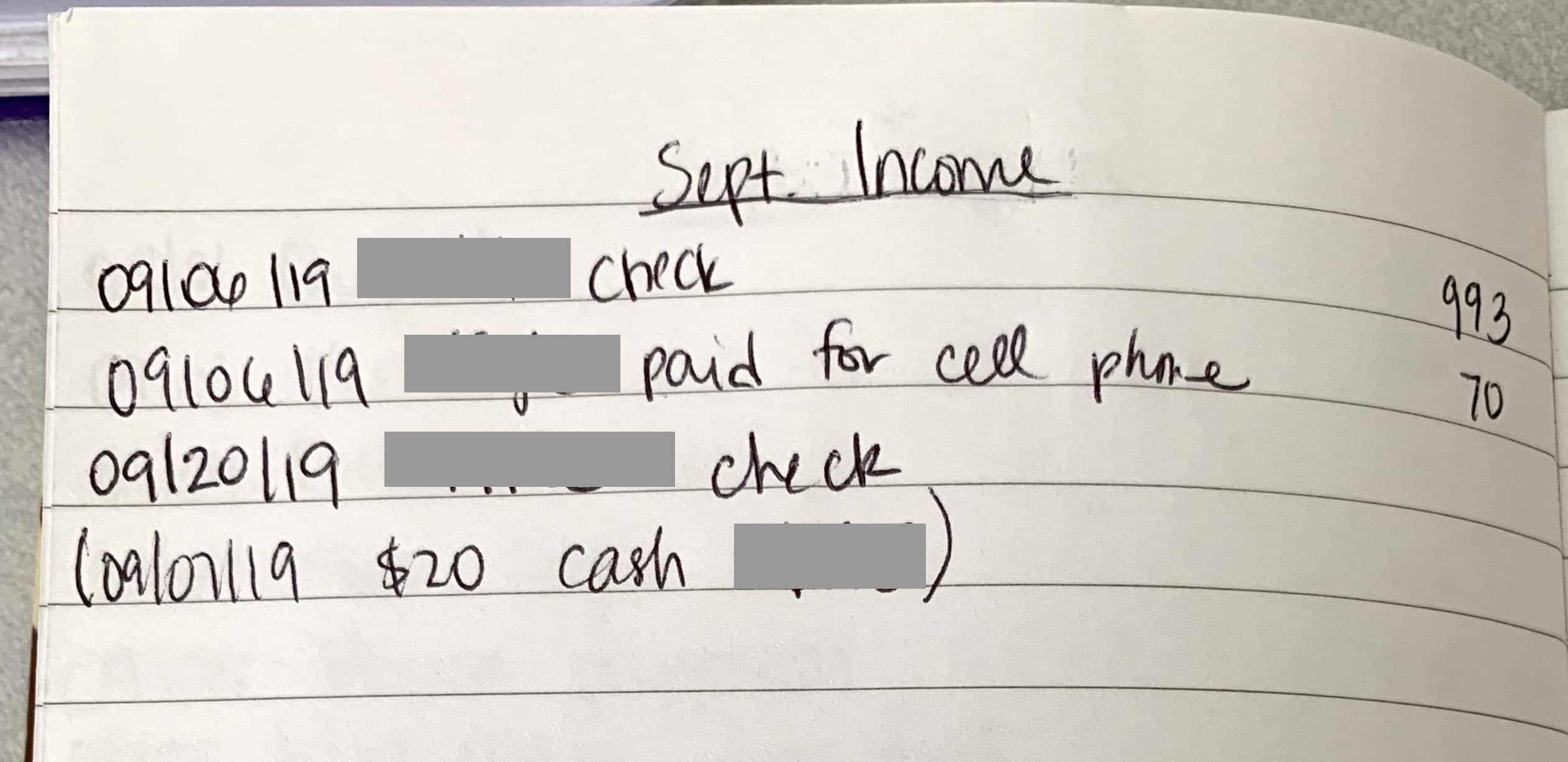

Amanda’s Income – Sep, 2019:

Lastly, here’s a snapshot of her income thus far in Sep… About $2,000 it’ll look like she’ll net by the time the month’s over, which is more than enough to cover all those expenses already listed and then some… Like those 5 savings funds if she’s still rocking them 7 years later?! They’d be pretty plump by now barring anything crazy!

Anyways, another great way to track this stuff if it fits your personality, and if it doesn’t here’s a list of some other options you can try as well if you still haven’t found one that clicks –> List of free budgeting spreadsheets and apps. There’s also that calendar method we featured here the other week as well –> A reader’s review of CalendarBudget.com

Hope something here helps!! And would love to see YOUR way of budgeting if you’d like to spill your numbers/screenshots with us?! ;)

*******

Addendum: The $498 house payment is the *entire* monthly mortgage payment plus house insurance and property taxes! Amanda apparently lives in a super low COL area (“where gas is $2.19 per gallon right now”) and she tells me all her savings funds are still in full effect too, though now combined into one main “emergency fund”… Go Amanda!!

Get blog posts automatically emailed to you!

For budgeting, I’ve used excel and now YNAB. Pretty boring stuff. But the real magic is in my money board, where I track the current goal of paying something off. $1 usually represents $1k. Each time $1,000 is paid off, a dollar moves from the left side of the board to the right. When the debt is cleared, the money moves back to the left and a new goal is set. I’ve paid off tens of thousands of dollars this way. The last $27 is on the left because I am paying off my house and will be completely debt free next year!

Ahhh that’s so cool!!!

Is this a *physical* money board, I presume?! How big is it? Can you send me a picture???! :)

How much do you think you’ve paid off in full since trying it?

I too want to see a picture of this board — it sounds like an excellent way to stay motivated!

Okay, third request to see this board. I also use YNAB, but am looking for something to motivate us to save more (we’ve paid off all debt but the house), and this sounds like it might be right up the alley. Please do a guest post for J!

I’ve shot you both emails w/ it ;)

That’s a good ol fashioned profit and loss statement right there! I love it!

Haha yup! How it was done for thousands of years until computers ;)

Hi J! I like to use a simple google spreadsheet and the zero based model of budgeting, meaning everything that comes in for the month gets assigned (to bills, debt if any, savings). I also use between 5 and 6 saving funds, some are long term and others are more short term where I plan to use cash out of. I just opened a bunch of e-savings accounts on my bank’s website and named them. The biggest drawback is honestly waiting for my next paycheck so I can do it all over again! We live very below our means (hubby and I make just under $65k/year), so it is possible even for modest income people to do this too. Hope this is encouraging to others to start budgeting and saving!

Yayy!!!

Always good to hear how others work it!

And totally get the thrill of waiting to spread out that next batch of dollars, haha…

Thx for popping in :)

Congratulations, Amanda. You’re discipline and intention have allowed you to accomplish much. Nothing you have accomplished is by accident or luck. Your success is all you, and you are doing it in the most marketed to country in the world. Keep up the great work.

You’re discipline = Your discipline. I caught that right as I hit the submit button! :::facepalm:::

Your excused ;)

(see what I did there??)

This is great! And very inspiring. I earn about the same and I often think I don’t earn enough to really move forward.

J$ I wonder what you’ll think of my 2 saving funds and *goes look* 11 sinking funds… it’s just Excel jfc, in the bank all sinking funds are lumped in one account.

Actually, I’d argue that modest earnings usually mean you need more sinking funds. With those earnings, even a once-a-year €200 expense can mess up a month’s budget if you haven’t planned ahead, while a high-earner would pay it painlessly when it came.

Very true indeed!! And if it’s working for you – great!! That’s the hardest part of it all – figuring out the best way to manage this stuff :)

Very inspiring story Amanda! Goes on to show it’s not just about how much you make, but what you do with it.

J, thanks for sharing with us here

Yes, the money board is a bulletin board that hangs on the wall in the office. It’s about 18”x22”. I’ll email you a picture. It’s pretty plain looking… it’s literally money on a bulletin board! :-)

My husband and I have paid off approximately $249k in debt over the past 13 years using it.

INCREDIBLE!!!

LOVE this! The options for budgeting out there are endless, pretty cool to see evidence of not need much more than a notebook, pen and calculator. At its core, budgeting really is that simple!

Kudos to Amanda and thanks for featuring something we don’t see that often in the personal finance space!

:)