Hey guys!

So we all know that FIRE stands for Financial Independence Retire Early here, but did you know that there were actually different *types* of FIRE that you could shoot for? Depending on how comfortable you want to be in retirement, as well as how long you’re willing to wait to get there?

I caught these in that recent NY Times article that’s been floating around our community, and it’s been interesting poking around & selecting the version that best matches with my vision :)

Here was the article if you want to check it out (super click-baity, gah) – How to Retire in Your 30s With $1 Million in the Bank – but it features a ton of $$$ bloggers as well as these new-to-me flavors of FIRE:

- Lean FIRE — “retiring” and living off a lot less

- Fat FIRE — “retiring” and living off a lot more

- And Barista FIRE -“retiring” and then working part-time at Starbucks to get company health insurance or other benefits, haha…

And then of course there’s regular FIRE, which sits somewhere in between Lean and Fat, and was the only FIRE I knew up until this point.

(I put quotes around “retirement”, btw, since we all know you’re not truly retiring from doing stuff, you’re just switching your energy from doing stuff you don’t enjoy to doing stuff you DO. Whether for money or personal satisfaction. I have yet to meet anyone who’s FIREd and just sits on their ass all day!)

Do you see the FIRE that best fits you? Personally, I’m shooting for regular FIRE with a mix of Barista FIRE :) I don’t want to live real sparsely in retirement, but I also don’t need to live super luxuriously either. As long as my family has enough to survive + a little extra fun, I think we’ll be just fine. And since I always plan on working on *something* on the side anyways, whether on my own projects or at a coffee shop or bar or any other favorite jobs to try one day, any additional perks would be gravy. And I’d imagine it’s a lot more fun working on the side when you’re not in it for the money! :)

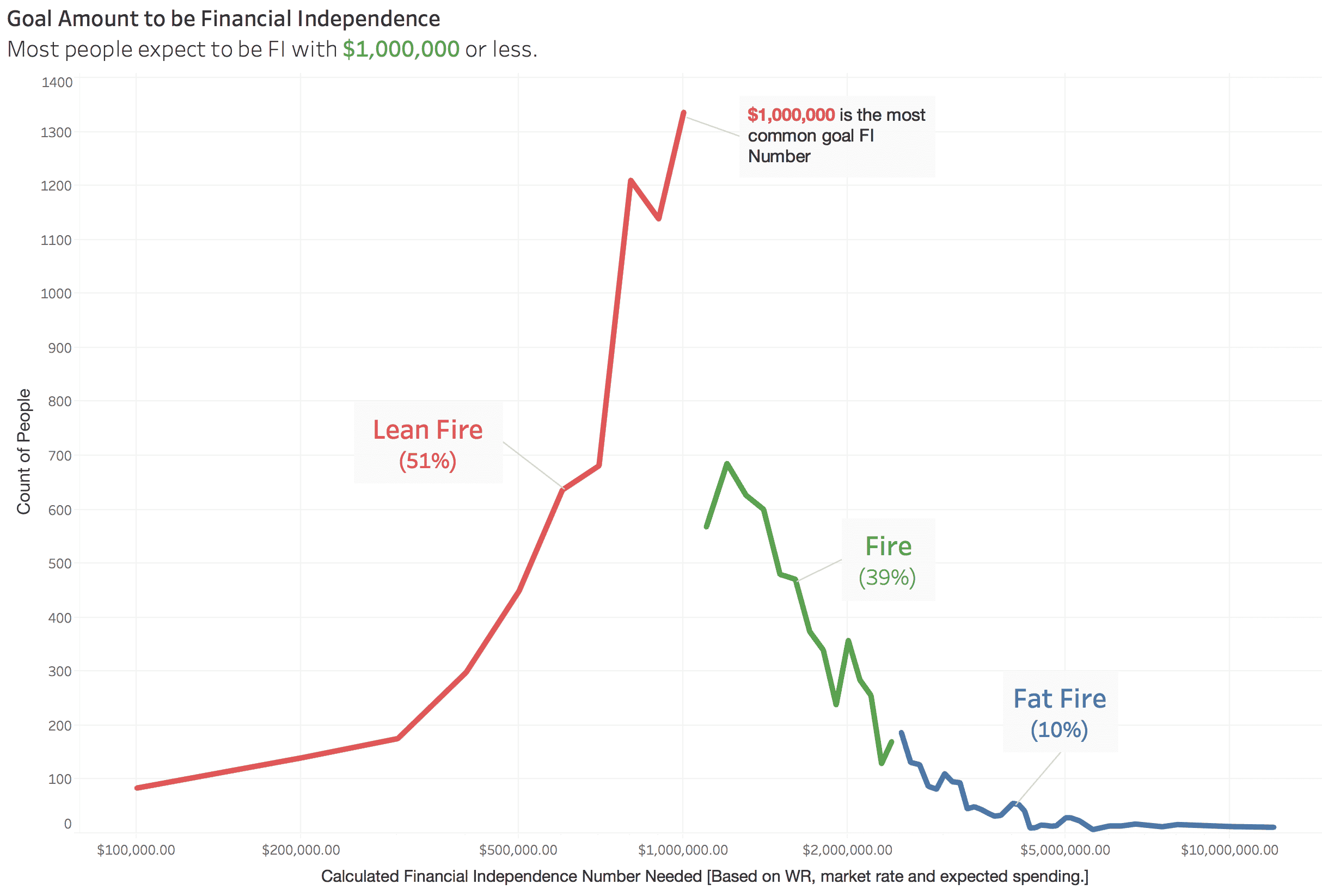

To put some hard numbers around this stuff, I refer you to Adam of Minafi.com who put together a pretty impressive – and much more in-depth! – report around these variations of FIRE for better context: What’s the Difference Between Fire, Lean Fire, and Fat Fire?

He came up with the following framework based on his research and polling of the space to help pinpoint the version that fits you best:

- Lean FIRE: living off $0 – $40k yearly income (<$1,000,000 needed)

- Regular FIRE: living off $40k – $100k yearly income ($1,000,000 – $2,500,000 needed)

- Fat FIRE: living off $100k+ yearly income ($2,500,000+ needed)

- (Barista FIRE: the above range that fits you best, minus estimated insurance/perks?)

The number “needed” to hit these goals is based on the Trinity Study that many of us follow, which basically says you can live off 4% of your investments or calculated another way: 25x your yearly expenses. So if you plan on only needing $40,000 a year to live off, then you’d need $1,000,000 banked which is 25 x $40,000 and drops you in Lean FIRE range.

For me, it comes out to $1,800,000 if I want to retire with my current standard of living ($6,000/mo x 12 x 25), but in a perfect world it would be closer to $1,200,000 ($4,000/mo x 12 x 25) which still falls in the realm of regular FIRE. And in which case I’d need to have a paid off house or my kids out the door or any other substantial change in my lifestyle to make it a reality, haha… All of which is pretty far away!

It’s cool seeing these different versions though, because it really helps remind you to pay attention to your *future vision* vs your current one. Something I have a hard time keeping in mind myself, since I can barely forecast my life past tomorrow, no less the next decade or two ;) But maybe you’re better at this than I? And possibly already living off your ideal expenses, making for an even smoother transition down the line?

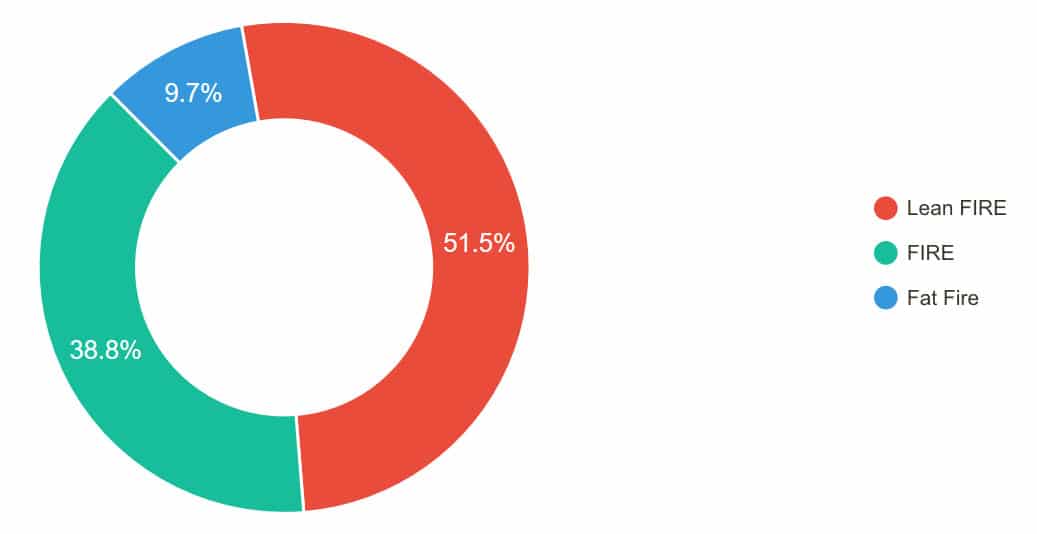

At any rate, check out that article by Adam if this stuff interests you because it’s packed full of great stats and breakdowns, and also includes some excellent charts around what others in our community are working towards as well.

Here’s a couple of them below. What version of FIRE are you shooting for?

[click to enlarge any of the graphs]

UPDATE: An astute reader mentions there’s actually another variation of FIRE we left out: Fart FIRE ;) Check it out – it doesn’t stink!

Get blog posts automatically emailed to you!

I’m going for “Forest FIRE” which means I’ll have plenty but will still seek a part-time gig doing something in the outdoors or outside, maybe to keep healthcare and maybe just for fun.

Oooooh I like it!!

But make sure you get to wear a spiffy hat while doing it for triple the fun ;)

Fat FIRE is what I’m shooting for! Only for the reason that it requires me to think more creatively and use my intellect better to get there. The path and the end result will be more enjoyable!

Very true! Could do a lot of *good* with all the extra money you don’t end up needing too if you end up overly impressing yourself :)

According to this scale I am shooting for Fat FIRE, not much over the cut off for regular FIRE. I know with having young kids there are plenty of expenses coming in the next 20 years, and I also don’t have any interest in Lean FIRE for the long term, so my number is on the higher side.

fatFIRE for me. We’ve got the fatFI down, working on the RE part. A year from now, I think we’ll be there.

Cheers!

-PoF

Oh yeahhh? So party time at next FinCon then?? :)

You always hear that the “one more year” syndrome is pretty hard to overcome, but seems our community here is getting better at it with people pulling the trigger left and right… Hope you’re indeed next, my friend!

Adam (Minafi) also had a great post on FIRO. It’s Retirement Optional and that to me sounds more pleasant. To keep me sanity I need a few projects and hobbies to aim for or I’ll start feeling like an animal in captivity.

We’re going for fat because my husband and I are paranoid and I heard kids double risks =) if it was just me without hubby I would def do Barista FI. I freaking think it’s brilliant =) I want to be a Walmart greeter and say hi to people all day long! What a cute job!

FIRO!! I like that!!

Fat FIRE for me. But I’d like to keep the required expenses in the Lean category and use the remainder for fun.

Fat Fire for me too. Not that I plan to live a life of luxury life but it will be nice to have that cushion if we need it and we can use some of what we don’t need for family. We’re also concerned about the ever rising health care costs which can take us from Fat Fire to Lean Fire pretty quickly.

Yeah, that’s the biggest question mark in retirement for sure… And yet another reason I love me some Barista FIRE :)

My current plan in similar to yours, regular FIRE, but probably with a part time job to make a few bucks and keep busy. I personally call this semi-retired since i don’t really think a person is fully retired if they’re still working at all. But I’m trying to keep my options open. I’m taking a slower approach to FIRE than many. I’m 20 years from my regular FIRE vision, but could pull the plug a few years early and go Lean FIRE, or keep working a few more years and go Fat FIRE. I can’t predict what I’ll feel like doing in 15-25 years. It will depend a lot on how much I enjoy my job at the time. And a lot on how the stock market does during that time period as well!

It’s good you’re staying flexible and taking it day by day like that. A lot can happen in 20 years for sure!

Fat fire is great, but I don’t think that i’ll be interested. I have never lived the luxury life, so I don’t really need one when I am retired. I am just shooting for the $80K – $100k income range and that’s good enough for me.

I am a few years away from regulars FIRE, but I am already keeping an eye on the “one more year syndrome.” Hopefully, I can pull the trigger.

I hope so too :) It’s a good problem to have, but still a problem. Especially since we don’t know how long we have left on this great earth of ours!

Wooo, thanks for the callout J$! This was a really fun one to make.

I’m shooting for the high end of FIRE/low end of Fat Fire myself. There’s something comforting and having $100,000 as a ceiling on spending (so $2.5m) – especially when our current spending is closer to $75k). Seeing how many people see their spending rise as their age does make me nervous – but then again the data on spending is almost all based on people who continue working and earning more. Be interesting to see numbers from the current batch of early retirees in another decade.

Totally! Although might want to compare non-hustlers out there than us hustler crowd who will always be earning (and probably more!) in “retirement” haha…

Really really good article over there, and of course you know I’m a fan of your other stuff too.

Currently living Fat Fire and three months into the RE. Did some traveling around the country to learn how to start spending the money that we have saved.

Paying Cobra health insurance now at $1600/mo. The Barista FIRE will be investigated in 2019 after my planned six month corporate detox period.

Ooooh fascinating!!! You blogging about your experience with all this?? Very smart to do that detox… And to learn how to spend your money for that matter, something most of us here aren’t that used to, haha…

While I could do lean FIRE right now, I really enjoy my job, so I guess I would be that FIRO that is mentioned in a comment above.

I agree with Nate on his definition of FIRE. I think we’ll end up with lean fire due to circumstance and not choice.

We’ve got a FIRE goal in 2030, when the house is paid off (144 more payments!). Our pull-the-trigger date is pegged more to that than to anything else. The market could return only 1.5% over the next dozen years and we’d still crack the two comma club, assuming we can keep putting away at least what we’ve been investing for the last couple of years.

Then, who knows? Our taxable income would likely qualify us for significant health care subsidies, or one of us could grab a part-time job within walking distance for health benefits, or my wife (who makes $20k more than I do) could decide to keep working part-time at her career because her employer treats her right. Four-day weekends every week for her, while living solely off of her lowered salary as our investments compound… that sounds pretty good to me. Point is we’ll have the flexibility to decide. And to us that’s what FIRE is all about.

Damn straight.

Really fun stuff! I’ve completely changed my thoughts on this in the last year. Since I’m pretty much all set to retire anytime, work isn’t work anymore. It’s an opportunity to help others every single day without worrying about the ramifications of what I do or say. Just enjoying the ride:-)

Nice!!!! That’s the life right there! :)

Trying to FatFIRE by myself in case something bad happens, but could probably just live off of leanFIRE amounts for myself pretty well even in NYC!

I’d like to work at a chill startup when I become FI haha. You lower pay but get equity, so if the startup blows up (which it frequently does) I won’t feel super stressed that I absolutely need to make it work.

Oh yeah, it’s super exciting too! I’ve worked for two start-ups before and they first exploded for the good, and then exploded for the bad, haha… But was a helluva ride in all cases!

Wish this was more popular 18 years ago when I left my corporate job. Told everyone I was retiring. At that point, had only achieved Lean FIRE. Never intended not to work, but wanted more choices. I have done the Barista FIRE, because I needed health insurance more than the money. Now, in the stages of Regular FIRE. Enjoying having my own business, volunteering, and having free time to pursue hobbies and being in the moment.

Congrats! You were cool before you even knew you were cool ;)

I am a Lean FIRE :)

I live with very little and I work 2 hours per day doing things that I love. I teach dance (salsa and Tango) and I do freelance photography from time to time.

Doing nothing would be very difficult.

Haha… always love it when you chime in – you make it look so easy :)

Fat FIRE’d 100 days ago, and loving that new 35′ 5th wheel! Not ever having to worry about money again = True Freedom!

Oooh FAT FIRE! Didn’t know that was the option you went with.

Well done, Mr. 401k Millionaire ;)

Anyone who says less than “Fat Fire” has a poverty mindset. The purpose of wealth is to give it away and leave a legacy. If you want to retire on $60,000-80,000/yr, your dreams are too small.

What if you just don’t want to work an extra 10-20 years to reach it? You can still volunteer and leave a legacy without gobs of money :)

I disagree. You can be happy while spending only $20k/year. You can be miserable while spending $1 million per year. (Think about all the rich folks who end their own lives on purpose or by accident by doing something stupid for the next high).

I’d say it’s easier to be and stay wealthy if you can learn to be happy and satisfied with less money.

I’m aiming for Fat FIRE.

Or well, our baseline expenses should be consistently under $40k with potential spikes for voluntary splurge vacations, but I don’t plan to actually retire until I have millions stashed away. I like my job too much. :)

I disagree that lean vs fatFIRE is a specific number range. In my definition, leanFIRE just covers basic living expenses, and fatFIRE covers that and all the fun stuff. Depending on where you end up living, $40k a year could be fatFIRE ;)

True true… so in your take there’s no regular FIRE then?

I guess we fall into either the “regular FIRE” or Fat FIRE category. We’re right at the $2.5m mark with our investable assets, and then if you add home equity we’re at the Fat FIRE level.

Personally, I’d like to derive a lifestyle that’s very similar to the U.S. median income … around $60k a year.

I’m aiming for regular fire. The fat meaty part of the curve. :)

I’d rather be on the upper end so we can cut back as needed.

Yeap, $60k/year is a good goal to shoot for. That’s comfortable almost anywhere in the US.

It’s FIRO for me, too, I think. Coming late to the party post divorce, still trying to get priorities straight, etc. Too much up in the air right now, but I know I want to be FI. If I wind up going for FIRE, it will likely be lean (unless there is an unexpected windfall, then who knows?). I also like Barista FIRE, then I can do something fun or work PT somewhere that feeds my soul.

Welcome to the party! :)

Barista FIRE for me! Get enough to cover the basics, then I would just do Postmates, Wag, and charge up Bird scooters to make do. If you only need to make 10k or 20k a year, imagine all of the fun stuff you can do!

What are Bird scooters? Haha…

Bird Scooters are those hop-on-hop-off scooters you can rent in some cities to get around! There’s also Lime Scooter that’s the same thing. You down load an app, scan the scooter to rent it for 1 minute to whenever. But, they run out of “juice” and get broken. That’s when @financialpanther comes in with his side hustle to re-juice the scooters!

Ahhhh yes – got it now! Those things look fun! :)

Probably somewhere between regular FIRE and barista FIRE. But we want to be flexible. :)

105 days left until regular FIRE for me… and it can’t come fast enough!

Now let’s get some of the Fat FIRE guys to hook us up with some drinks at FinCon! ;-)

— Jim

OH WOW!!!! So close!!!!! First beer is on me at FinCon! (But only the free ones ;))

This is a tough one for us. At 35 and having battled a whole young adulthood of poorly paying jobs and inadequate $ knowledge, we feel very late to the game. Thus, so often it seems like Lean Fire is our only option if we truly want to retire semi-early by 50! But really, there are so many options. I could see us VRBOing our tiny house long into the future for a nice Barista supplemental income as well. So many unknowns at the beginning of the journey!

Just keep the snowball rolling… You’ll be surprised how much momentum it gets once it starts building! My husband and I have grown our retirement accounts 156% in the last four years! The first $100K is the hardest. We started later than you and hope to retire when I’m 50 and my husband is 55.

I second that!! And while your money is growing so will your brain :) My mindset is 100% different than it was 10 years ago, and I’m sure it’ll only continue to shed more light on what truly makes me happy as well! Excited for you to start this journey!

I love looking at all the options! Another one that I like is coast FI. I think having so many different variations takes the pressure of one particular goal out of the equation. I am still shooting for fat fire but also barista :)

I’m Blogger Fire bwahaha!!

That was literally the last goal I had with this blog, haha… Accomplished it 8 years ago and haven’t replaced it with a newer goal yet :) I hope you make it over here with us!!

I think it will be “Morbidly Obese” (rather than “Fat” ) for us. We’re over $6.0 million in net worth but wife still plans to work to 65 because she likes what she does. We already have more dough than we need. I’d like to pack most of what I do in, but wife wouldn’t be happy if I were retired and she wasn’t. There’s something about the “RE” (retire early) that just won’t be happening for us I guess. At least I’m not working that hard right now. And I am ALWAYS going to lend money which is the best business in the world (next to insurance).

Hot damn man! And you’re still on $$$$ blogs too – love it! Haha…

Hoping for high end of regular FIRE/low end of fat FIRE – will likely depend on how the market does for the next 20 years! Right now, FIRO sounds like a good option to me since I like my job and can’t imagine not working. (Knowing I have enough F you money and could retire when I want to and not when I have to sounds like a great situation to be in.). Plus, I’m also calculating my FIRE number conservatively – targeting a number that after projected taxes would still leave me 25 years worth of projected expenses covered, plus extra for traveling.

Regular FIRE for us.

Living in Europe, healthcare costs are not a major concern so no need to go baristaFIRE.

If anything, we’ll go BeachFIRE. We may go broke, but at least we’ll have a great tan.

Seems like most of the world has figured out how to care for their humans unlike us :(

I guess I’m fat FIRE. My goal is a house paid off plus $10k per month in after tax dollars. I plan to enjoy my retirement and want to make sure I have enough for something to go wrong, update my house, pay any medical bills, travel, etc.

I think some of the lean FIRE people are one day going to want more and will need to go back to work.

I like the paid off house goal since that would be one less (major) thing to worry about. I’m probably going to have to go back to owning too once it’s time to settle down as I can’t imagine paying rent for the rest of my life although I sure am enjoying the peace right now, haha… haven’t had to pay or worry about the condition of our house in years :)

I started my fatFIRE Feb of 2017 when I retired from my medical practice. I’m a year and a half into it now. We have been travelling the world and are only home about 50% of the year. I was worried I would miss my job, but I have not. I have a new mission now, teaching doctors about personal finance, through books, blogging and speaking so it keeps me busy. I think it is important to have something to do when you FIRE, especially if you worked as a busy professional. If you get bored, then your retirement will lose its luster.

Dr. Cory S. Fawcett

Prescription for Financial Success

Good for you man! Love to hear you’re enjoying it AND paying it forward.

The physician/money niche here has exploded in recent years so you’re definitely in good company. Here’s a list of a handful of others in the space as well if you’re looking to connect and throw a party together or something :)

https://directory.rockstarfinance.com/personal-finance-blogs?search=doctor

I’m aiming for fat, but I end up where I end up. Al I can do is be responsible with the things I can control and overtime hopefully that means I hit any of these. Life constantly happens and everything can not be accounted for, that’s just the reality of it.

Okay, that might be my favorite comment so far… We def. tend to wait for the stars to align on stuff before pulling triggers on stuff, huh? I certainly don’t want to be waiting around for *some* day to happen if I can be enjoying my life more now! Excellent insight..

We’re pursuing lean FIRE and trying a different approach (versus what seems to be the norm).

Instead of grinding away at a 9-5 *until* we hit a specific lean FIRE number we’ve decided to travel (travel hack), house sit, work remotely, and live everyday life in combination with pursing lean FIRE.

We’ve been traveling continually since 2016 and have been fortunate enough to visit three continents, 26 countries, and nearly 70 cities all while doing 26 house sits.

For us it’s more about the journey and adventure rather than a specific FIRE number. :-)

Love it!!! And tell me you don’t travel with kids or else I’m going to be even more jealous?! ;)

You’re right, no kids yet. ;-)

*wipes brow*

**But still impressed!**

I always love your articles!

The RE part is a bit tricky, for me. I’m 44 and am at a point where I could LeanFire or even regular Fire (my savings can sustain my current spending with a 4% Safe Withdrawal Rate). I think I would consider 44 to be RE. I still love my job and I am still challenged and motivated to work. I figure I could reach FatFire by 50-52 (some things are out of your hands, like market/investment returns). Is 52 still in the RE range? Our generation didn’t really have the FIRE movement when we were younger. The closest we had was “Freedom 55” lol. You should look it up – I think it’s a Canadian thing where London Life Insurance had a big marketing campaign in the 80’s focusing on retiring comfortably earlier than average.

Hah – nice!

I think if you can retire ANY TIME before your 60s it should be considered early :) But really age is a state of mind, right?? I still feel like I’m 21, only with about a million responsibilities now, haha…

Thanks for posting this! I never knew there was more than one type of “FIRE”. This is some good stuff. My personal goal is to be able to Lean FIRE by 40 and Fat FIRE by 50, but I will probably be in the Barista FIRE category past age 60 since I would get bored after a while and want to do an occupation I enjoy/care about. The different categories really helps further organize what’s best for everyone.

That’s a good idea shooting for different phases like that. I hope we’re all still around over time (both online, and in living!) so we can track how everyone’s doing :)

That’s not what the Trinity study found. The max time period is a 30 year period of retirement in the study and it found different levels of success for different AAs and different time periods. Sorry, but it bugs me that people gloss over v. important details like that. For everyone planning to FIRE, read the study yourself so you truly understand what it said.

There was a really interesting interview with Bill Bengen who first suggested the 4% safe withdrawal rate. I think it’s about 1 year old. There’s tons of good stuff in it but I believe he said “actually, it’s 4.5% SWR” and the 4% SWR has a very high chance of success provided you don’t hit a massive bear market in your first years of retirement.

See Reddit link below. I thought it was really good.

https://www.reddit.com/r/financialindependence/comments/6vazih/im_bill_bengen_and_i_first_proposed_the_4_safe/

Thanks for the info/links guys! I’ve always used it as just a basic rule of thumb to forecast around, but it is true we try to simplify it a lot more here on blogs… Mainly just to get others to be able to quickly do some math and get a good idea too. Even flawed it’s better than the “Everyone needs $2,000,000 (or $5,000,000 or $10,000,000!) in retirement or else they’ll DIE IN FINANCIAL RUIN!” type of advice out there that doesn’t even account for differing lifestyles.

Regular FIRE all the way. Upon learning about this lifestyle, I decided on a number in which to aim for. Since then I have been making progress towards my goal. However, its not to say this number wont change in the future, but knowing how much you need to live the lifestyle you want is whats important in determining which type of FIRE you are seeking. Thanks for the great read, I was unaware of the different types until now.

Nice post :)

I will probably be regular FIRE. But I’m probably on the high expense side of regular FIRE. Being in Switzerland does not help keeping expenses low. But I’m still able to stay below 60’000 dollars each year. We’ll see how that goes!

Fat FIRE balance but I’m quite frugal, so I’d likely be spending at regular FIRE levels.

That’s a good combination :)

I propose the addition of “Dumpster FIRE.” i.e. obtaining food, clothing and shelter from a nearby dumpster.

Like this guy? ;)

https://smartasset.com/mortgage/this-guy-is-living-in-a-dumpster-would-you-trends-in-micro-living

The goal would always be barista FIRE. But i would be fine with just with the high end of regular FIRE ;) Root for you success