What up $$$ lovers!

I thought we’d do something different today where we tackle a subject that everyone’s talking about, but one that yours truly SUCKS at: Travel hacking.

I.E. signing up to all kinds of credit card offers and reaping hundreds thousands of dollars/reward points to travel the world like you’re Jay Z on a budget ;) I.E. something I don’t dare mess with myself because it hurts my brain and seems like a lot of work, even though I know it isn’t and should quit being a pansy! Haha…

What can I say though, I’m a sucker for minimalism. I literally just have one credit card for all personal use that gives me so-so rewards (the USAA World MasterCard where our household expenses go and is paid off monthly), and then only one card for my business stuff too (Blue from American Express). Nice and easy… Just not “look at me I’m traveling the world for free cuz I’m so clever!” type of nice ;)

So this post is dedicated to those who want THAT type of nice, and to learn how the card hacking game goes to grab your rewards in the most efficient way possible.

And to do that, I bring on my good friend, and blogger, Brad Barrett of RichmondSavers.com. Who’s not only racked up over a million points of his own for his family (yes – a million!), but who’s also helping normal people like you and me learn how to do it ourselves through his Rewards Coaching program. Something that he offers for free, and is customized to your own particular situation.

I asked him a bunch of questions on this stuff to better understand the rewards game, so hopefully you find this as helpful as I did. At the end I’ll include a sign-up link if you want to jump in and get personal help from him yourself. Enjoy!

Q&A With Travel Hacker (and Coach) Brad Barrett

J$: You’ve been featured on NBC, CBS, and even The New York Times for your travel hacking skills. What got you started with all this stuff?

My wife and I always used our credit cards for all our purchases and we of course paid them off in full every month; we were tired of just getting the normal 1% rewards and figured there had to be a better way.

About four years ago I came across a post by J.D. Roth on Get Rich Slowly about this amazing 100,000 mile offer on a British Airways credit card. It sounded too good to be true, so it set alarm bells off, but I trusted J.D. and his site and we decided to dip our toes in.

We were able to turn that one credit card bonus into eleven round-trip flights between Richmond, VA and New York City (we’re from Long Island) that we would have paid nearly $5,000 in cash. That’s $5,000 of free travel from one single credit card!

After that I was hooked and did a ton of research and kept opening cards; we’re up well over 1,000,000 total points/miles earned and there’s no end in sight.

J$: What was one of the best trips you and your family have taken pretty much for free?

Without a doubt it was our big three-generation family trip to Walt Disney World in Florida. My wife and I earned enough rewards points to take our two daughters to Disney and stay in the on-site luxury Disney Swan hotel, plus get airfare to Orlando and WDW park tickets all for just a few hundred dollars out of pocket. We easily saved $3,000-$4,000 just for the four of us.

My parents and Laura’s parents also followed the same rewards points plan I mapped out, so they could come with us on the trip for nearly free! It was a really special thing for our girls to have the whole family there and travel rewards points really made that happen.

I did a lot of research to put together the whole trip and I have it mapped out on my site with step-by-step instructions to a free Disney trip.

J$: One of my favorite things about your service is that you’re a total one-on-one type trainer over both email and the phone. Can you share some of the things you go over with your clients to better help them maximize their rewards?

Thanks J$, I appreciate the kind words! I love working with people one-on-one, and I think they get so much value out of interacting with a real person who has done this before and can explain it to them in terms that make sense.

I’m just a regular family guy, not some globetrotting hotshot who flies around the world in first-class every week, and I think people can relate to me and to our family.

This is an intimidating subject – I mean seriously, we’re talking about opening credit cards which goes against everything people have “learned’ over the years, finding the right card bonuses, earning enough points for the actual trip and then figuring out all the rules on how to book the award flights and nights! That is not easy and it provides a lot of reassurance for people to have me there to bounce questions off of, or jump on the phone with to discuss.

The biggest thing I preach is flexibility.

If you can be flexible with dates specifically, you can really save many thousands of dollars on your travel. If, however, you try to shoehorn your rewards points into your regular travel life, or think that this is the perfect solution to get free flights to that wedding in St. Kitts you have to attend on July 4th weekend (my go-to silly example for how not to make this work), then you’ll probably be frustrated.

Flexibility extends to travel destinations, airports to fly out of, being willing to take flights that have a connection, etc. If you can add a little flexibility in, and have some time to plan your points strategy, then you will absolutely love this travel rewards concept!

J$: What are some of the cool places your clients have been?

All over the world! That’s the amazing part about travel rewards points – those “dream vacations” can become a reality with the right planning and a little bit of flexibility.

I’ve helped people take multiple-country honeymoons in Europe, a professor on sabbatical visit Europe and Africa on one award booking, trips to Hawaii, Asia, Bermuda, the Caribbean and pretty much everywhere else you can think of. Recently I helped two groups take 6+ month trips around the world!

It is the most satisfying feeling in the world to help people save thousands of dollars on their travel that would have otherwise been deducted from their bank accounts. After being a CPA in the corporate world for all my adult life, I can’t tell you how much psychological value I get out helping people in this way – it is truly amazing.

J$: I’m a guy who likes things as simple as can be, so the idea of having dozens of cards all over the place makes my brain hurt. How do you go about organizing everything?

I crave simplicity in everything in life, so I’m right there with you. I take the lowest-stress approach to this I possibly can, and it just works for us. A lot of people who get into travel hacking would laugh at how conservative we are and how many points we’re leaving on the table, but again, we’re making this work for our regular family and that’s good enough for me.

We go one card at a time and just concentrate on that one single card. I’ll open an account in my name and add Laura as an authorized user. We’ll spend on that account until we hit the minimum spending requirement and then we’ll take those cards out of our wallet.

Then Laura opens a card in her name and adds me as an authorized user. We keep going back and forth like that so we’re constantly working on a new bonus. We’re able to earn about 500,000 miles per year like this, which I value at about $10,000, so even though this is “simple” it is still quite lucrative.

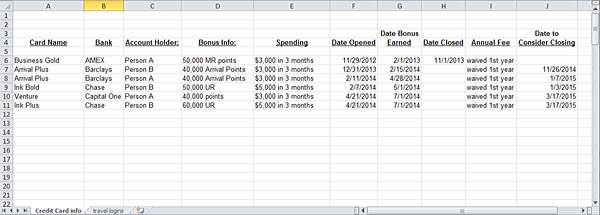

To organize I just have a simple Excel spreadsheet where I keep my card information (just dates I opened, closed, etc.) and our rewards account logins. There are probably more elegant ways to do this, but this is simple and it works for us.

J$: What happens if you screw up?

The biggest way you could screw up is financially, since we are talking credit cards. I’m a CPA and you’re J$, so I can safely speak for both of us here: Please do not get into this if you aren’t responsible with your credit cards. That means paying on time and in full every month and not spending more than you would have if you were using cash/check/debit.

In terms of the cards and travel, I’m not sure you can screw it up too badly; missing out on a credit card bonus would be one way, so only open a card if you are 100% sure you can hit the ‘minimum spending requirement’ on the card. I’d hate to see you open a card and not earn the bonus.

Even if you forgot about a card account you had open and you got a bill for a large ~$100 annual fee, you could always call up to close the account and have them waive the fee, so even that wouldn’t be a big “screw up.”

I think it just pays to be organized and consistent with your new cards. I do see people who just forget to open new cards and then have to scramble at the last moment to put together their trip. That can be frustrating, as you never want to scramble getting points all the while hoping those award seats are still available!

J$: What about credit scores? Doesn’t it jack them up?

Just like anything with your financial life, you need to assess your own unique situation and determine if this strategy makes sense for you. You need an excellent credit score to get approved for these premium travel rewards credit cards (almost always over 700).

My wife and I have consistently opened credit cards over the past 4 years and at last check my score was up 2 points over where I started and Laura’s was up 12 points. The lowest mine ever temporarily dropped was 25 points.

For our lives this was irrelevant since we weren’t making major purchases on credit, but clearly for some people (looking to get a mortgage, buy a (gasp) expensive car with credit, rebuilding credit, etc.) every point counts.

[Editor’s Note: Probably a good idea to track your credit score if you end up going down this path just to keep an eye on things…]

J$: If you could only sign up to one credit card for the rest of the year, which would it be?

My go-to credit card is the Chase Sapphire Preferred, and I think that’s the perfect starting card for just about anyone getting into this strategy.

The Chase Ultimate Rewards points can be used a variety of different ways (even for straight up cash deposited into your bank account if you were so inclined, but that’s the “worst” option), and can be transferred to 11 different partner airlines and hotels like United, Hyatt, Southwest and British Airways, for huge redemption values.

A lot of beginners like the flexibility of the Barclaycard Arrival Plus and the Capital One Venture as well, but my favorite is the Chase Sapphire Preferred for sure.

J$: Lastly, what’s sexier – budgeting or credit cards? ;)

Anyone who has ever seen people flock to J$ at the FinCon financial bloggers conference will know that the answer has to be budgets!! Haha.

In all seriousness, I think responsible credit card usage to earn these massive signup bonuses has a place in your financial life. If you can earn 1-2 trips per year just for being smart about where you direct your normal spending, then that’s about as powerful a financial tool as I can imagine.

**************

If you want to learn more, or to tap Brad to get your own travel hacking plan started, you can sign up here: Brad’s Rewards Coaching

He definitely knows the ins and outs of this stuff, and again his services are completely free (he earns commissions by the credit card issuers if you end up signing up to any while planning your trips – which is how he’s able to do this for free for people).

It’s not for everyone – as evidence of me not going down this rabbit hole yet myself (though I am now signed up to his emails to learn) – but if you’re interested in this stuff, Brad’s a great person to start with. I’ve met him a couple of times in real life and I can vouch he’s a genuinely good guy or else there’s no way I’d be featuring him here ;) He’s got a $hit ton of testimonials too – even from financial bloggers using him, hah!

Anyways, hope this sheds more light on the travel hacking game. As Brad mentioned above, this is NOT for anyone who sucks with cards and can’t use them responsibly. If that’s you and you’re getting tempted here, just shut this page down now and move on… Not worth the risk for a free trip or two – your finances have to come first!

—————

PS: Big thanks again to Brad for partnering up with me on this one. It’s only taken me approximately 3 years to do a Q&A on travel hacking, and now we finally have one! Haha…

Get blog posts automatically emailed to you!

I also found my credit score going up once I started travel hacking. It’s a win-win-win if you do it right. I do one at a time too, it’s too much for me to track otherwise.

I’m with you. I move from 1 card to the next. Multiple is confusing.

you guys are hustlers!

I haven’t gotten a new card in approximately 5 years – hah.

Amazing, right Stefanie? Big wins all around for sure, as long as you just keep track of everything.

A lot of people can manage the whole multiple cards at once thing, but it isn’t for me (and seemingly not for you guys either). You can get a ton of value out of even doing it in this measured manner.

And come on J$, we’ll get you started at some point! :)

We got a lot of free flights from our first credit card after getting married. Now that we have little ones flying isn’t quite as fun. But this approach sounds more involved, and lucrative, then whatever we used to do. Great info as it’d be nice to afford flying as a family when they’re older. I keep hearing about the Chase Sapphire Preferred card. Must be a winner.

I haven’t dared flying yet with my two little boys – scares the bejesus out of me! haha…

We have two little girls (see pic above!) and this sure makes traveling a whole lot more affordable!

Southwest Airlines is a solid one to focus on when you have a family as they don’t have any gimmicky award limitations — you can easily book tickets with points on just about any of their flights.

The CSP is a really great card, and it is the backbone of any cohesive travel rewards strategy. Other cards like the Cap One Venture can be great “quick wins” though, so I don’t discount those.

Lots of card options depending on your travel plans and what airport you’re near :)

I too had tired head when I started thinking of juggling all of the cards we’d cycle through in a year.

But once you have a system – a simple one like Brad’s is perfect (we used a google docs ss + google calendar reminders – setting them up at inception with each card takes 1 minute), the system really takes over.

I think this is most definitely a Challenge-worthy activity – let’s see J$ get out of his comfort zone a little!

hah!

if anyone can get me to try it it’s Brad, so I haven’t given up on myself yet :)

Let’s see him do that indeed!! haha :)

Seriously though, I always tell people you have to do what’s comfortable for you and your life. There is not one way to succeed with this, and I certainly never try to talk people into anything. You can get value from one card and you can certainly get a lot of value from multiple cards over a period of time.

Sounds like you have a nice system!

Just connected with Brad. He has some great information and he’s from my neck of the wood. Small World. Disney pun intended. :)

That is pretty magic-al :)

Small world indeed :)

I sent you back a personalize video this morning! A Disney trip should be great…

Great post! I had never even heard of travel hacking prior to becoming a blogger in late 2013, but we are now on our third rewards card. So far we’ve been able to reap some pretty sweet rewards from it, but I know we could probably do better if we got more organized and developed a system like Brad and his wife have! We might do that in a few years, for now having an infant has put a bit of a damper on some of our travel :-). Thanks for sharing these tips!

I know how hard it is to add an extra anything into your life when you have an infant, so I totally hear you!

Even though we haven’t traveled as much as we would have liked over the past few years when our kids were young, we’ve been stockpiling these points and can now finally really put them to good use!

We have big trips coming up tentatively to Europe and South America the next few years! Really glad we kept earning those points

I wish I had gotten more into traveling hacking before we had a little one. Now traveling is a little more difficult. Though you make a good point about stockpiling points for the future. I’m hoping the points won’t be devalued in the future or limitations/restrictions added with more and more people taking advantage of it.

Great breakdown of hacking! I’ve worked with Brad a little bit and he has been great to work with. When I first started travel hacking my concern was losing track of the cards we’ve worked on – the Excel spreadsheet/calendar reminder approach solved all that. It can get really simple to track after that.

Damn, he’s working with everyone in the PF world! Haha… Rock star.

Thanks for the kind words John — I appreciate it!

You’ve been doing amazingly well for yourself with the travel rewards stuff :)

Awesome article! I have been wanting to start looking into travel reward cards but I need to actually sit and research it. This was the kick in the pants I needed! It does make me a little nervous to start because we will be applying for a new mortgage in the next few years and i don’t want to jeopardize anything, however, if we can save money on travel and bank that money it would mean a bigger down payment (we travel a lot so our kids can see their grandparents). Choices, choices!

I’d ask Brad all these questions and see what route he would take :) Even if you don’t go through with anything it would still be good to get the feedback from an expert in the field! And doesn’t cost a penny (the best part)

I’d be happy to chat about it Elise, so definitely reach out!

Depending on your timing with the mortgage, this might not make sense to you now, but let’s discuss…

Thanks! Let me figure out exactly what I want to know (the jumble of nonesensical images of vacations and dollar signs in my head aren’t helping right now!), and I will definitely reach out.

Very cool stuff. We generally just go with the cash back, but I’m sure my wife wouldn’t mind us doing a vacation instead. Maybe that’ll be the plan next year!

The cold hard cash is tough to pass up, believe me, I understand!

Most of the value is from these large signup bonuses on the travel cards; the cash back cards don’t often have the bonuses, so you’re stuck with the normal 1-2% “rewards.”

If you were going to travel, then this would be something worth looking into from an overall financial perspective…

Not impressed… too much risk. There’s no such thing as a free lunch. Credit card companies offer these rewards for a reason: just like a rebate, people are rarely able to make them work for them. I find this one big endorsement of debt. You can travel hack without having to risk so much of your financial life: We scored an AMAZING cruise of two weeks across the Atlantic for only a few hundred bucks total – it should have cost us $3000. But we were flexible with dates, and when the cruise line needed to fill those last few cabins, we were on board… literally! Hah!

What’s do you see as the risk? If you already use a credit card, your simply moving your natural level of spending from one card to the next.

RE: Endorsement of debt. I would say to the average person out there not paying attention to their $$$, that yes – this would be a stupid move to make. Which is why we mention it a number of times in this article to NOT do this in that case :) Fortunately, if you’re on a personal finance blog, you’re looking for new ways to rock $$ and hack the game, so I’d hope that by and large people here know their position or are at least cognizant of the drawbacks. You’ve got to be smart by just reading this blog, right? ;)

Hi Kati,

Thanks for the comment and I’m sorry you interpreted it so negatively. We said multiple times that you should only do this if you are responsible with your credit cards and pay them off on time and in full every month. Case in point:

“The biggest way you could screw up is financially, since we are talking credit cards. I’m a CPA and you’re J$, so I can safely speak for both of us here: Please do not get into this if you aren’t responsible with your credit cards. That means paying on time and in full every month and not spending more than you would have if you were using cash/check/debit.”

This is decidedly not an endorsement of debt in any manner.

Great deal on the cruise by the way! How did you find out about the last minute availability?

If you paid for even those few hundred dollar cruises with a Cap One Venture or Arrival Plus it would have cost $0! :)

I’m on that bandwagon. We’ve flown to San Fran and Brazil (for 2) on a single sign-up. I just hit the points level for the Southwest Companion pass, and probably have another 400,000 points in the bank.

My word, son! You are killing it!

I just got the Chase Sapphire Preferred and hit my spending target to get the bonus. Have you had luck canceling the annual fee after the first year? Or is the card worth it enough to you to pay it? Thanks.

Great question and this comes down to if YOU think it is worth it to pay the $95 annual fee.

If you’re opening up new credit cards to get the bonuses, then in all likelihood you won’t be using the CSP too much and it would be hard to justify the $95.

If you are just sticking with that one card, then you could see paying the fee as it is a great card.

You can close all cards before paying the annual fee, so no worries about ‘luck’ coming into it :) It’s just a 2 minute phone call

I just got my very first credit card a month ago. It’s a Discover it card. What card should someone with my credit score (710ish) get next for travel hacking?

And sweet featured image, J$. BEAUTIFUL!

You are too much, haha… You go from zero cards in your ENTIRE life to now thinking of getting a handful, haha… You’re an all or nothing type guy, aren’t you? :)

Hey Will,

It is impossible to answer the question in a vacuum without knowing more about your travel goals and what airport you live near. If you want some personalized advice, just sign up for my travel coaching and I’ll record you a video based on your response to my 4 short questions!

The Chase Sapphire Preferred is tough to beat, though I could see a card like the Capital One Venture being useful as it is a simple way to save about $460 on completely flexible travel (after hitting the current bonus requirements).

Brad was kind enough to do a phone consultation with me and Mr. FW earlier this year and we learned a ton! He knows everything there is to know about travel hacking and is such a nice guy! He really helped us figure out how to wisely use or convert the points that we already have as well as strategies for accruing points with other carriers. Glad to read this interview and I hope anyone interested in travel hacking will get in touch with him!

I think he needs to copy this into his testimonials page, haha…

Half the bloggers commenting here have apparently used him! He’s cheating on me! :)

Thanks for the kind words!! Maybe I will copy this into the testimonials page…with your permission of course :)

I really enjoyed speaking with you and Mr. FW and I think you two are going to save a whole lot of money with this strategy!

Brad – Great article and I am digging your website. I am hoping you can clarify one point for me, as I am relatively new to learning about Travel Hacking. If you close the card after one year to avoid a fee for year two, do you need to use the rewards before closing the account? Are you able to transfer them and then close the account? I am mostly interested in the Chase SPC that you are high on, and wanting to use it on some hotel rooms. This is fascinating stuff though, and certainly something I am going to test out. Thanks!

Hey Greg,

Great question! If you sign up for my coaching, I send you a link to my intro webinar where I talk about the 3 different kinds of cards and where the points reside. I think that’ll give you a better overview than I could here, as I don’t want to shortchange your answer.

The CSP card: Those points reside in your Chase account, so if you closed the card before utilizing the points, you WOULD lose them. However, the simple 15-second fix to that is to just TRANSFER them out to one of the 11 hotel/airline partners prior to closing the card.

Those points have so much value because you can transfer them at a moment’s notice to one of those 11 partners, so in a perfect world you can keep them in Chase to preserve that flexibility.

If you have a spouse/domestic partner you can consolidate your CSP points into their account (this works for any of the Chase cards with Ultimate Rewards, but you want to only do it with the premium cards: Chase Ink Plus and Sapphire Preferred) instead of transferring them.

In that sense 2 spouses can keep those points alive in Chase as they open new cards. If the time came where that isn’t plausible then you just take your best guess on where you’ll use them and transfer them there (Hyatt, United, Southwest and British Airways are my 4 favorites). They would then be subject to the expiration policy of that partner, but that should buy you at least another year on the points.

Thanks Brad, that makes great sense. I will look at signing up for the coaching in the near future!

I love reading these stories, but it just seems like too much work for me, juggling all of the cards. I just use a card that gets me decent cash back, then apply that to my balance. The money that would have gone to pay the bill gets moved to my investment account. Simple and easy. Works for me.

I hear you Jon, believe me! I absolutely crave simplicity in my life, which is why I take the easiest and least stressful approach to this concept.

There are people who open 5x the number of cards I do in a year and that works for them. Too much stress for me!

If you travel anyway, then I nearly guarantee you that you’ll come out ahead using this travel rewards strategy as compared to a 1.5%-2% cash back card. The math is just overwhelming!

Guys, this works. I’ve saved over $15K in flights to/from the US to visit my family over the past 6 years using cc bonuses. :) I’m going on 7 years of just paying fees ($100 or so) for round trip flights from New Zealand to the East Coast of the USA! :) These flights are normally about $2500 – $3K NZD a pop…

I do feel like the rewards are drying up, though. I’ve taken advantage of as many of the bonuses I can by now, and a lot of the cards don’t really let you get the bonus more than once, so I may have to start paying soon. I’m definitely going to sign up for the coaching to see what Brad can do for me! Thanks J$!!

Holy crap – wow. You are working it! Haha…

Let me know if Brad ends up being able to hook you up even more :)

I’m thankful that my favorite vacations are camping trips. Since we have all the gear, they are crazy inexpensive. I’m taking two weekenders, and two 5-day trips this year, among other day hikes, and I don’t even have to budget for it since I’ll buy food either way, gas is getting split, and permit fees are usually free (or a whopping $15 for really popular trails).

There’s campsites all around the world! ;)

Though I still prefer my cash money over “points” any day of the week… If only you got more cash though…

There’s a huge argument to be made for cash, no doubt about it!!

However, if you are someone who travels anyway and that money is coming out of your bank account each year regardless, then it is almost a mathematical certainty that you’ll come out ahead using this travel rewards strategy over the piddly 1-2% cash back a regular credit card gives you.

I’ll get you involved yet J$!!! :)

Just got my second rewards card in the mail a few days ago with a lovely 25,000 Aeroplan miles AND a $70 rebate for going through a referral portal! The fun (only with this kind of readership haha!) part is it forces you to organize your spending more. For example, I actually put off a few planned purchases (I’m a sucker for bike accessories) until I got my new card so that I could put them towards the minimum spend. I’ll likely try to use my miles for a trip next year sometime… only “problem” is I can’t decide where to go!

It is something only we would have fun doing, haha… Congrats on the good problem :)

Good “problem” to have, right!!

I’m a huge fan of Air Canada, as their award availability is excellent! I usually use United miles (Star Alliance partner) to book their flights since I have a ton of United miles and they don’t charge the ‘fuel surcharges’ that Aeroplan puts on their own flights.

I would google “aeroplan avoid fuel surcharge” if you want to learn some great tips.

So far I just have two credit cards, one that gives 5% cash back on gas and another that gives 1.5% cash back on everything else. If the cost of credit cards are going to be baked into the price of everything, might as well get some of that back right? I like the fact that it’s simple and easy to keep track of.

But I like Brad’s idea of the simple spreadsheet to keep track of things – that makes things seem less overwhelming. And I am extremely interested in taking advantage of all these rewards! For now I think I’ll have to sit on the sidelines and watch though as vacation is currently not so flexible and spending too low to hit any sort of bonuses at a good rate :)

I’d always take spending low vs a free trip :)

I love using credit cards, but I’ve always stuck to cash back cards because of the simplicity. It’s not much – but I make around $20 – $50 each month. I’ve since made it a point to dump all cash back into my daughter’s college fund, which I think will add up in the long run.

That being said – this post might make me reevaluate my use of credit cards! Thanks for the info. I might have to give this a shot!

love your blog name :)

Thanks! :) My cheapness went into hyperdrive mode as soon as my daughter was born!

I’m as frugal as they come, so I hear you about the value of the cash back!

If you have little ones and you aren’t traveling now then there’s of course a great case to be made to continue with the cash back. If you know for a fact that you will travel in the somewhat near future, it is always helpful to start stockpiling these miles & points. Let me know if I can help :)

I must admit I have not used a credit card in probably 7 years, but my wife and I are celebrating our 10th year Anniversary and after a quick chat with Brad…I completely changed my and saw the savings!!

I still can not believe it’s just that easy! I have already hit my spending limit and on my way to saving over $500!! Can you believe, this was money that I was going to spend anyways on our trip so why not get paid a little kick back for doing it.

Thanks for this awesome interview J$!

Very cool! Congrats man! Another happy customer, haha…

So glad it worked out for you Eric!

(and I’m glad the new blog is up and running; looking forward to seeing how it progresses)

Wow, great post! I have been really interested in travel hacking lately, but I am leery of trying some of things I have read before. My hesitation has been around potentially messing up our credit scores. We have worked really hard to have excellent credit scores and maintain our credit history. We are responsible with our credit cards now by paying them off every month and I don’t think this would make us less responsible, but the impact of opening and potentially closing a card does concern me. But your post makes me a little more optimistic. We track our scores on Credit Karma and we have already purchased a home, so we don’t anticipate any large purchases on credit any time soon. Definitely some things to consider here.

I think it’s smart you’re considering all this stuff than just jumping in and going for the free $$$/travel :) Gotta make sure it matches up with your personality/goals/etc first.

I’m maybe like you J–basically unmotivated to get into this travel hacking stuff. My wife, however, lives to hack (what used to be called ‘beating the system’). I will forward this post to her, and watch the sparks fly! :)

I’m sure they’ll fly *in the bedroom* wherever she ends up taking the two of you – ZING!

We’ve done a little bit of travel hacking but would love to get into it a bit more, especially once we start traveling more as Baby T gets older.

Hey J$, great interview and a great “get” in having Brad.

Like you, I’m not temperamentally suited for this, but luckily Mrs. jlcollinsnh is! She has been doing this for a while now and Brad has helped her refine her approach.

Just the other day she said to me, “Oh, BTW, you are flying First Class to Ecuador this fall for the Chautauquas.

Speaking of the Chautauquas, Brad also stepped up and offered to help all the attendees travel hack their way there for FREE. Thanks again, Brad!

He’s a great guy to work with.

Look at that! Awesome worlds colliding all over the place :) I’ll have to come out to one of those things and chill with y’all. It does sound pretty fun.

Brad rules. I had no idea how to get started with travel rewards, and he sent me step-by-step instructions and talked me through it over the phone. As a result, my fiance and I recently went to Japan and Hawaii. Flights were about $450 each–that’s round trip, both destinations. We’ve already started earning points for our next trip, and bonus: my fiance’s credit score has improved quite a bit since adding him as an authorized user. Totally worth it.

Nice!!! And Congrats on the engagement – how exciting! :)

I stumbled on the concept of travel hacking a few years back on my own, before I even knew it was a thing. One of my sons started college a few years back and that’s when I started seeing all of these bonus offers for opening new credit cards. For the past 3 years, I have been opening 2 new cards (one for myself and one for my wife) just before the beginning of each school semester and his tuition bill coming due. I split the tuition payment between the 2 new cards each semester (easily hitting the minimums for each card’s signup bonus), and then paying off the credit card balances out of our state 529 education plan, to which I had been contributing since he was little. Earlier this year, we had a wonderful 2-week 25th anniversary trip to Europe, with 75% the cost covered by all of our bonus points/miles I had accumulated travel hacking over the past 3 years. On average, I would say for every $7000 spent on college costs, I got back $1000 in travel rewards. So, for those parent’s with kids in college or about to start college, travel hacking can be a very lucrative way to get back some of your hard-earned college savings!

Woah! I didn’t even know you could PAY college tuition on a credit card – that’s bad ass! (And also scary for those who aren’t so good w/ credit – hah).

Thanks for sharing, man :)

J$ – I think maybe this needs to be discussed a little bit further. Playing this credit card game is not without its ramifications to your credit bureau score.

Credit bureau scores are broken down into 35% for payment history, 30% for amount owed, 15% length of credit, 10% new credit and 10% types of credit. Playing this credit card game will impact 15% of your score. Here is how – say John Doe has had a credit card with ABC Bank for 10 years and another credit card with First Bank for 2 years. That’s 12 years of trade line history between two cards for an average length of credit of 6 years. Say John Doe starts this credit card game and adds 4 new cards. Now he has 6 credit cards with barely over 12 years credit history for a new average age of 2 years. That will impact a credit bureau score! Also, all those new credit limits and the accompanying credit inquiry will have a 5 point hit on the score. So John just took a 20 point hit on his score for getting these new credit cards in playing this game. Another thing to consider too is if the credit limits of all these new revolving credit cards and the balances of any existing installment loans total greater than 25% of their annual gross income. If something unfortunate happens to this person and they start using these credit limits their Debt To Income Ratio could skyrocket AND their credit score drop just as fast. Maxing out credit limits lowers your score.

I get what people are trying to do with travel hacking but I think it is a dangerous game and like someone said above ‘there’s no such thing as a free lunch’. So says the guy who works for a credit union and looks at a lot of credit bureaus.

I hear ya, brotha… I don’t mind my minimalism ways at all in the c/c world :)