Morning hustlers :) Welcome to my Motif Investing review.

So one of my goals for this blog in 2015 and going forward is to try out a lot more financial products out there and then report back to y’all if I find they’re kosher. I tend to stay within my nice comfy bubble of companies and services I love, but the problem with that of course is I never learn anything new. And worse, miss out on some pretty cool $hit out there!

In fact, two of the last three companies I tried out I’m now obsessed with:

- Republic Wireless (the cheap cell plans we now have!)

- Digit (the new way we’re saving!)

That would have really sucked to overlook those. And who knows how many others I haven’t tried yet??

So going forward I’m going to try and be a better financial blogger and keep y’all abreast of things, while upping my own game in the process. And this is why I said “yes” to do a Motif review and participate in a little blogger competition going on sponsored by Motif Investing ;)

The “Grow Your Dough” Throwdown

If any of you know Jeff Rose (GoodFinancialCents.com), he arranges these awesome movements where he gets a lot of bloggers to write about a particular financial topic. Sometimes it’s around debt, other times it’s life insurance, and this time around it’s investing.

Or more specifically, to show how easy & cheap it can be to invest.

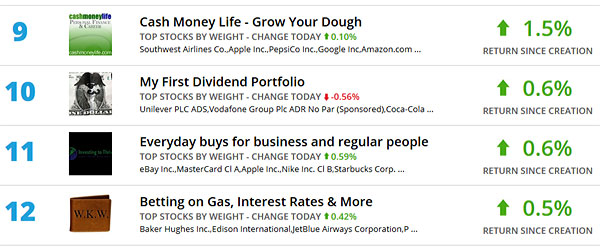

So 20 of us personal finance bloggers are having a nice little competition to see how far we can grow $500 in the stock market :) Most of them are getting all strategic and trying to find the killer performers to win by year’s end (PT Money won last year w/ a 33% increase!), but instead I decided to use it as an opportunity to learn more about dividend investing… And will probably lose in the process, haha.

But I ain’t no fool! I invest for the long haul, bitches… No short term gaming for me ;)

Why Dividend Investing?

I read a lot of early retirement blogs, and while there are a ton of ways to gain financial freedom (real estate, investing, entrepreneurship), it seems most of these guys favor the dividend investing route. Which is owning stocks of companies who give their shareholders some extra money every few months (dividends) to share in the profits. I accidentally, I mean on purpose, already get dividends by investing all my money into Vanguard’s VTSAX index fund, but I want to learn more and see if it’s something I should be pursuing more.

I also haven’t had a brokerage account since I dabbled in day trading back in my idiotic youth, so this gave me an opportunity to finally open one back up and start diversifying my investments. 100% of everything I own right now is in retirement accounts (SEP Ira and ROTH Ira), so this will be my first taxable account to start managing again.

I’m scared and excited at the same time :)

I HATE the thought of dealing with taxes on all this stuff and messing with the simplicity of my system, but again I know I need to wise up on this stuff or else all my millions will be tied in retirement funds I can’t touch until I’m old and gray!! And how are you supposed to retire early on that?? (Yes there are ways to convert stuff strategically over time, but that’s for a whole other day. And for someone much more intelligent like Mad Fientist to enlighten us on ;))

What Is Motif Investing?

![]() Because with Motif you can invest up to 30 stocks at one time and only pay a single transaction fee: $9.95. Which means we can all create our OWN “funds” based on our strategy super cheaply and easily. These funds are called “motifs,” and then anyone else with a Motif account can check them out and learn or invest in them too. It’s all rather cool and unique.

Because with Motif you can invest up to 30 stocks at one time and only pay a single transaction fee: $9.95. Which means we can all create our OWN “funds” based on our strategy super cheaply and easily. These funds are called “motifs,” and then anyone else with a Motif account can check them out and learn or invest in them too. It’s all rather cool and unique.

To put this in perspective, I wanted to invest my $500 for this “competition” into 10 individual dividend stocks. So instead of paying $9.95 x 10 = $100 and losing 20% of my funds off the bat (!!!), I was able to do it for only $9.95. And then I named it “My First Dividend Portfolio” in case others are interested in it too (you can make these public or private btw – you don’t have to share anything).

So, in a nutshell Motif Investing allows you to invest in a bunch of stocks or funds all at once, and you don’t have to pay a handful of fees to do it. It’s simple and easy, and there’s only a $250 minimum to open up an account, and there are no maintenance or inactivity fees at all. The Motif team also shares their own strategic “motifs” as well, for those looking to go a certain route (like a group of stocks/funds by industry, target date, Vanguard indexing!, or even dividend-focused. Even though I didn’t listen to them and did my own, haha…) They’ve been around for a while it looks like as well.

You can learn more here if interested: MotifInvesting.com (that link will give you up to $150* if you end up signing up btw – a nice start to your account!)

What Dividend Stocks Am I Investing In?

I’m glad you asked :) Since I haven’t the first clue where to start, I decided to ping my good friend Jason over at DividendMantra.com to help mantra me ;) Here’s what I emailed him:

If you were starting your dividend portfolio from scratch, where would you put $500?

I’m playing in this “investing challenge” with a group of other bloggers, and while they’re all trying to strategize to have the most $$ by the end of the year, I’m gonna use this as an opportunity to start my first taxable brokerage account instead to be the groundwork for early retirement :) And I really like your dividend approach!

So, if you were starting all over again knowing what you know now, where would you put your first $500?

And here’s what he sent back:

Hey, bud. Thanks for writing and considering me!

I won’t make any claims as to short-term performance. I’m a long-term investor, so I’m investing for the next 20-40 years with most of these stocks. But I’m more than happy to participate and see where things go.

The stock I’m picking might not outperform other picks over the next 12 months. I have no idea about that. But if I were starting all over again and had to pick just one stock today, it would be Johnson & Johnson (JNJ). It’s my largest investment and I’m confident with its long-term prospects. It’s just an incredibly well-run company. The valuation is a bit on the high side right now, which is partly why I’m unsure of how it’ll perform over the short term. But I can’t imagine being unhappy with this investment looking back on it 20 years from now.

So that’s the stock I would recommend for someone just starting out. Provides above-average yield, and has traditionally beaten the market over long periods. Plus, its volatility is low and will provide downside protection in case the market starts correcting aggressively.

If you’re looking for me to pick a stock that I think will outperform others over the next 12 months, which, again, is not something I typically aim to do, I would pick Philip Morris International (PM). Great yield, the valuation appears fair, and there’s a lot of upside potential, in my view.

So I don’t know if that’s the one you want to enter in the contest, but invest in JNJ. Or you’re more than welcome to use JNJ since maybe some readers might balk at PM since it’s a tobacco company. But I would pick PM right now if someone were challenging me to a contest for performance over the next 12 months.

Either way those would be my picks for their respective purposes. :)

It’ll be interesting to see how it turns out!

I’m certainly not a guru or anything, but I think I’m doing well so far. I’m probably going to earn $7,000+ next year in dividends, which, at 33 years old next May, puts me on pace for financial independence by 40 (where I want to earn $1,500 per month in passive income). So things are moving along.

What a thoughtful (and helpful) response right? That guy lives and breathes this stuff and is just incredibly nice. You can file it under favorite blog #2 if you’d like, right below Budgets Are Sexy ;)

Anyways, if you’ve been paying attention, you’ll know I invested in 10 stocks instead of only 1 or 2. Now why is that when Jason only sent me the two? Well going back to the initial purpose of playing along and trying out new things, I wanted to better test out this Motif Investing and see what it’s like to pick up a handful of stocks and create a portfolio.

So in the end I *did* listen to Jason – both of those stocks are in my new portfolio! – but I took it a step farther and invested in TEN of his largest holdings of dividend picks as listed in his portfolio he shares with the world. Now I can track and learn more :) And I have no shame in copying…

My First Dividend Portfolio!

Here’s what this “First Dividend Portfolio” of mine now looks like:

Here are the 10 dividend stocks I invested in:

- Unilever (UL)

- Coca-Cola Co (KO)

- Philip Morris International (PM)

- BHP Billiton (BBL)

- Kinder Morgan (KMI)

- Wells Fargo (WFC)

- AFLAC (AFL)

- Vodafone Group (VOD)

- General Electric (GE)

- Johnson & Johnson (JNJ)

Interestingly enough I have been invested in these guys before, just without realizing they were dividend-worthy (can you tell I’m not an investing expert? :)). We’ll see how it plays out over the years, but currently we’re in 10th place. Even though, again, it doesn’t matter in the end…

(Click here to see the whole dashboard in real time)

(Click here to see the whole dashboard in real time)

The Purpose of All This…

To recap, the purpose of this little competition (at least for me) is as follows:

- To share, and test out, a cool new company out there

- To learn more about dividend investing!

- To start my first taxable brokerage account

- To have fun :)

I won’t be straying away from my indexing anytime soon (or, ever), but sometimes it’s fun to change things up and let loose a little. Especially if we’re talking smaller amounts of money compared to a nest egg (I’d never invest my $400,000+ into random stocks, whether my friends recommend them or not, haha…). And so far I’m liking the options Motif gives me. In fact, you can even invest in index or Vanguard funds through them if you wanted to!

What do you guys think? Are any of you currently using Motif? What do you think about my first dividend portfolio? :)

We’ll see how far we go down this dividend path, but right now I’m excited for the chance to learn… I’ve been talking about starting a separate brokerage account for months now and we finally have one!

UPDATE #1: Check out the comment down below by “DP” about the official terms of the $150 bonus. Looks like there are some variables that come into play.

UPDATE #2: Motif Investing now allows you to buy single stocks too @ $4.95/transaction. Which is nice, cuz it gives you the ability to house more of your investments with them if it’s something you want.

UPDATE #3: I’ve since pulled my $$$ and went back to indexing 100%… Was a fun experiment/game while it lasted though :)

UPDATE #4: Starting on May 15th, 2017, Motif will begin charging $10 semi-annually on inactive accounts with a balance of less than $10,000.

——-

PS: Just like all the companies I review and use on this site, I’ll get compensated if you sign up through any of the links in this post. Only unlike most others, you can get up to $150* yourself to start playing with ;) So a win all around if it’s something you end up signing up to. (And just like all other reviews too, please ONLY sign up if it’s something you’re comfortable with!)

Get blog posts automatically emailed to you!

Woo! JNJ is on my list of prospective buys, but not until the price comes down a bit more & I already own KO. I’ve been sharing my dividend purchases lately but nothing as exciting as a challenge :) just aiming to make more than $5/year in dividend income!

And I need to bone up on the tax implications further down the road too. So far I’ve only bought and haven’t sold anything so I’ll have time to figure that out unless you beat me to it and explain it all first! (Nudge nudge, go right ahead, save me a little trouble! Hehe)

Haha… I’ll be asking my accountant about it here soon, that’s for sure :)

If you’re in the lowest two tax brackets (your TAXABLE income is below $37,450 for 2015) you won’t pay a dime (or a penny even!) in taxes on dividend income or capital gains (when you sell a stock for more than you bought it for).

Congrats on your first dividend portfolio J Money ( I will call you D Money from now on :-) )

I agree with DMantra that if you took dividend growth investing more seriously, you could end up building your own diversified “index portfolio”, that can consist of 30 – 40 or more companies purchased over time. You can then sit back, hold for as long as dividend is not cut, relax, monitor your holdings, and enjoy that rising stream of dividend income. Since most of the dividend investors I am in contact with rarely sell, their portfolio costs are super low, and their turnover makes index funds look like day traders. A good starter list of companies is the dividend champions list, which includes companies that have increased dividends every year for at least 25 years in a row. Some like Procter & Gamble have raised dividends each year for over half a century!

And if you are married, earning less than say $73K you won’t pay a dime in dividend taxes to the federal government.

Best Regards,

Dividend Growth Investor

Ooooh that’s interesting to note in both areas! The Champion List (awesome name for that, haha) and the $73k. We’ll actually hit around $75k for 2014 actually. It’ll take a lot more convincing to get me away from my index fund, but I’m liking all this new information coming my way :)

…What if you were at $75K ‘Earned Income’ but then after Deductions and such you are at the ‘taxable income rate’ of $72K? IE you got a refund….

The $75k in my case is after deductions and what not. But good thing to consider for sure!

Looks good! Thanks for this info. I think this would be one good addition if you’re looking for diversification in investments.

JNJ has been been a trooper for me for the past 2 years. I’ll have to take a sharp look at Motif. This is the week I usually do my re-balancing with my dividend stocks in Fidelity, and only paying $10 for all the trades I’m about to do sounds pretty enticing.

I hear Fidelity is pretty good too – my parents use them and are always raving about them.

Motif is a really cool concept. I like how they and firms like Betterment are shaking up the investing world and making it a better place. Now, I just wish someone would come into the real estate world and blow up that system for the better as well!

That would be interesting!! At lest we can now all see homes for sale/rent/etc on our cell phones and computers, that wasn’t the case a handful of years ago :)

Zillow.com? Trulia.com?

I swear every time I venture over here I learn something new. Talk about a learning curve. I have never heard about Motif, but it really sounds like a good set it up and watch it grow investment, which I am drawn too. I’m gonna add this to my notes of possibilities of future investments when I get this debt off my back. Thanks for the info.

Well good! I learn something every time I blog here as well, haha… you guys are always leaving tips and tricks in the comments :)

I get it that Motif is potentially a good resource reduce the cost of investing. But the premise of seeking dividends in a taxable account is something I struggle with frequently. Unless you need the money or are seeking to generate enough dividend income to FIRE, I don’t know why someone would voluntarily give the government more money in taxes. I suppose I can see a situation where one would use the dividend to then fund a retirement account. Again, however, this is a case where they would otherwise be unable to fund it without the dividends.

I’m still wrapping my own head around it after only investing in retirement funds my entire life for the most part. The problem with all that, of course, is if you don’t want to wait until you’re in your 60s to actually retire. With investing in taxable accounts you can pull from them at any time or -in a perfect world – just pull the dividends to life off of! You’ll still have to pay taxes on all earnings of course, but with most income you do anyways so not sure it’s that much of a difference. And if you were playing the “pay no taxes game” like most early retirees do (they only pull $ up to a certain threshold to live off of – usually $20-$30k), then it never becomes an issue. You only need to figure out how to live off so little, haha…

The great thing about dividend income, is that the taxes on it are A LOT lower than your regular employee income tax. And if you can live off of relatively little money as J mentioned, then you could potentially pay no taxes on your dividend income.

Solid approach J! I went the boring old Vanguard Total Stock Market ETF route last year and ended up in the middle of the pack – which was just fine with me since it basically returned what the market did. I really like the concept behind Motif and LOVE that they allow you to get started for as little as $250. So often I’m told that someone can’t afford to invest and at $250 it really helps lower the barrier of entry for those wanting to get started.

I agree :) With both the Vanguard route and low investing limit!

Morning,

I had a question regarding what Jason wrote, “It’s my largest investment and I’m confident with its long-term prospects. It’s just an incredibly well-run company.” How well do you or should you know the companies you invest in. Maybe you aren’t the one to ask this but I am curious as to how far back in the company’s history you must go in order to get a solid background in to how they run their business.

Great question for sure, and I’m def. not the right person to ask :) I invest after talking to people who I *know* spend the time researching this stuff and whom I trust – mainly finance bloggers. And nowadays I mainly just stick with index funds which covers ALL companies, so it’s an even different ballgame.

It would be interesting to see how much time is spent looking over an investment or company by one of my friends here though. I’ll see if I can get Jason to share some light on this one :)

Strandedrocks,

J$ asked me to comment back to you, so I’ll do my best to answer your question.

First, even those buying equity index funds means you’re investing in individual companies, but just doing so in a wide swath at a time. So buying a Vanguard S&P 500 index fund means you’re directly investing in Johnson & Johnson anyway (along with 499 other companies), and that’s making a quality call in some manner. Except you’re just trying to spread the risk out by hoping all 500 companies are high in quality. I don’t make a call for 500 companies at a time, but rather one at a time. You can make an argument either way for that.

As far as determining quality, this is generally done by looking at a company’s fundamentals and qualitative aspects/advantages.

You can read more here:

http://www.dividendmantra.com/2014/01/how-i-analyze-and-value-stocks/

But you’re basically looking at the rate at which a company can grow, its balance sheet, its profitability, and any competitive advantages it might have. That’s the short answer.

It’s just like determining the quality of anything else in life. Determining the quality of a basketball player might involve looking at their PPG, MPG, RPG, leadership, number of championship rings, and injury proneness. You’re basically looking at quantitative data involving hard numbers and you’re also looking at intangible qualities.

My portfolio now has over 50 companies in it. And it’ll probably have much more before I’m all done. So I’m basically building my own index fund, more or less, but I’ll only own the companies I want and I’ll avoid the companies I don’t want to own. And once I’m done accumulating assets and living off of the dividend income, the underlying value should grow while I also largely avoid management fees.

I hope that helps!

Best regards.

I remember doing a challenge like this in high school, but with fake money. It’s interesting that they encouraged children to chase short term yields.

I’ve never heard of Motif, but I’ll check them out since I plan to move all our investments soon.

Yeah, I don’t get that at all?? We did the same thing in school and everyone was just trying to figure out how to game the system and earn a ton fast. I guess it’s better than not learning about the markets at all – and I’m sure I’m forgetting all the lessons they taught us too (I guess all we care about growing up is making money fast??? Haha…) – but I do always wonder if this is good or bad in the end. Would be harder to track over the long term too in a 3-5 month class period :)

I remember doing that in high school too. I think this happened during my senior year which was 1999-2000 so it was a very unusual market with the dot-com bubble top in March.

IIRC, the way our class was set up it was pretty easy to game because we were able to use hindsight bias to trade (Hmm, the price of XYZ was pretty low last Tuesday, I think I bought shares then!!).

I’m entirely unfamiliar with dividend investing so this is super helpful.

I do wonder what the advice would be though if someone were to want a more “socially conscious” portfolio. I would feel very torn buying into Philip Morris or Coca Cola.

You should write an article on ethical investing.

Great topic indeed :) And what’s even more interesting is that people are investing in most of these companies without even realizing it! Hardly anyone looks at all the stocks a mutual fund holds, and if you’re index investing – which of course most of us finance lovers do – we’re all owning tiny slivers of ALL companies out there… But you know there are funds and indexes/companies that focus on just that. In fact, Motif would be a perfect place to check out too since it’s all based on customized portfolios and trends!

On this topic: I am not dumping the stocks I already have but in the last year I’ve decided to consciously research and invest in companies that are most ethically sound, going forward. Not just meeting some minimum standard but those that are considered leaders.

I have plenty of time to be outraged by crappy companies, I’d like to now support those companies that perform well as businesses but also specifically as ethical businesses.

We are huge dividend investors and have only one stock that doesn’t pay them. In fact, we own several of the same companies on your list. We don’t do index funds because along with having all the winners in a sector, you also get the losers. With our latest purchase, our dividend/interest income now exceeds our pension income which is pretty sweet.

That’s bad ass! Way to go Kathy :)

And it’s true – we do have to hold the losers as well as the winners with indexing, but overall I’m OK with that since I never try to “beat the market.” I’m perfectly content getting average returns, haha… Which made it a little difficult for me to now create an account to hand-pick stocks in :) But I’m trying to get a little uncomfortable to learn!

To be honest, I’ve lost a bit of respect for you to see that you’re invested in Phillip Morris. Cigarette companies are pathetic.

Sorry to hear, man. I’d recommend to all those who don’t want to invest in similar companies to double check their own portfolios and make sure they’re not holding any of them without realizing. A lot of mutual funds and indexes who hold hundreds and thousands of stocks typically do. Fortunately there’s also companies/portfolios/etc that focus on more socially conscious investing to help make it easier for people :)

…meanwhile check your own holdings and make sure you aren’t investing other “sin” products (e.g., alcohol, pornography, and etc.) via mutual funds.

If you hold any mutual fund, I’m willing to bet large sums of money that there’s some “sin” stock in there.

We remain firmly in the index fund investing camp. Primarily out of laziness – with two full time jobs and two young children, we prefer to set as many things on auto pilot as possible. BUT I’ve been really contemplating ‘playing’ the market with a little bit of our money, just to see how we could do. This idea for Motif Investing sounds like an awesome way to test the waters. Thanks for sharing. And I can’t wait to see how you fare in the competition. Good luck!!

I’m right along with you, Mrs. Maroon :) It pains me a little to go outside of index investing myself, but it’s time to learn and I’m limiting myself to only a tiny % of my overall investments. So in the grand scheme of things it won’t matter much, whether it explodes for the good or the bad, haha…

That’s a solid idea. I love seeing companies drive prices down on investments. I have not yet used their product. The only place that seems to really be less expensive is Loyal3 and their selection is much more limited.

I might have to check these guys out. Thanks for the review.

Yup, Loyal3 and then I just heard about Robinhood too that apparently charges no transaction fees. All of which is much better than it used to be back in the day!

I used to be interested in dividend investing but I realized it would be too much effort. I’m an index investor which frees up a lot of time for me to do the things I enjoy.

I think I’m going to realize the same thing by the end of this – but forcing myself to try and see what it’s all about :) (Without touching any of my index $$ of course)

Dividends always make me feel warm and fuzzy. There’s something comforting about getting money out of your investments periodically without having to make actual withdrawals. But I always reinvest them! I should figure out if I could live off the dividends I create in my taxable account if I would stop reinvesting them… probably not but I’m sure it would at least pay for housing..

yes! that’s what a lot of those early retirees do, actually – live off their dividends. So you either need a shit ton of money invested in them, haha, OR you need to live off a shit-ton LESS money ;) But ultimately the goal would be to live off investments forever and not have to work another day in your life if you so chose not to. And before you get to that part, you keep re-investing those dividends to help your $$ ball grow larger!

dividends for the win, it’s free money. Think about it, you are the “bank” for these corporations and unless something really bad happens or you sell they will continue paying you money indefinitely. Most of the top dividend companies pay out a yield that is better than any savings account offers.

I like the idea of Motif for beginning investors (same with Loyal3.com) they are a great low entry into the stock market. but once you start getting into thousands and thousands i think it makes more sense to either buy book shares or go with a full service brokerage

I’ll have to take your word for that until I get to that point ;)

I like the Dividend Investing style, the long term appeal is certainly a benefit for those reaching towards FI.

There is an investing theory called Magic Formula Investing (MFI). The readers digest version is you invest in quality companies that are cheap, over time you will beat the averages. This theory is backed by a guy named Joel Greenblatt who is a big time name in investing. You find those companies by ranking stocks by 2 criteria, earnings yield (cheap) and return on capital (quality). There is a website run by a guy, who I believe is an actuary, who gets deep into the weeds of MFI. One thing he seemed to recognize was that companies that ranked high in MFI and also had a decent dividend yield, 2.4% or higher, tended to do really well. Now the majority of the website talks straight MFI but will occasionally mention the dividend angle. If you want to take a look, his website is at http://justadrone.blogspot.com/

Hey, cool thx man – will check it out :)

Motif is definitely a cool way to invest in baskets of ideas. I plan on trying out an account myself in the near future. I hope to get in on that next challenge.

Solid buys, J. The bulk of my investments are in index funds but I find that I oddly enjoy reading about and *attempting* to value companies so I’ve decided to go into some individual stock investing too. I was a bit apprehensive about dividend payers in general as it seems like the focus is so much.. too much.. on the dividend rather than also on the company’s fundamentals, growth prospects, etc. It’s important not to look at just the dividend in a vacuum but also keep in mind other things that may affect the company. But I read Jeremy Siegel’s book “The Future for Investors” and it really put dividend stocks in a new light for me – I highly recommend it if you haven’t read that one already.

I do some real estate investing so I try to go into individual stock investing with a similar mindset… maybe that’s wrong, or maybe that’s brilliant, I don’t really know. Joshua Kennon writes on this a lot as well. I could go into this a lot more in depth but I won’t – but I’ve learned through a recent decision that it’s all about maximizing your money’s utility (another JK theme) and in effect, buying the largest amount of cash flows possible at the lowest price you can. I did this recently with a home purchase but I feel like a similar mindset while examining companies wouldn’t be a bad idea… ie valuing a company based on the earnings/cash they bring in (with the house, it was on potential rent and purchase price). It means I probably won’t get to invest in my tech darlings (well I have some Tesla but that doesn’t count) but that’s ok. Heck I don’t even know if this makes sense but it does to me! I can try to explain further in an e-mail later :)

Haha I love it!! I have no idea if it’s smart or not myself, but I DO know that we all grow our wealth in a handful of different ways. So if this way is working for you really well and most importantly you’re *enjoying* it, then I say keep on keeping on my good friend :) All types of strategies for all types of people, right?

It’s working out today… I’ll get back to you in about 10 years to let you know how it all pans out ;)

Deal ;)

I did something like this in a college class and it was fun, mostly because it was fake money. I was clueless then and sadly still am when it comes to things like this :) I have never heard of Motif and am definitely going to check it out. I can’t wait to read the updates!

I’ve had Motif on my radar to test out and I just might in the next week.

Thanks for a quick prelim review on this site! All of my investments are in my 401K at work, but I’ve recently become more interested in the idea of investing in various funds. I’m so new to the game I’ve barely started, and trying to figure out the right path is overwhelming. The various prices seem right though, and Motif seems like a pretty safe way to dip my toes in without too great a financial risk ($250 versus thousands of $$ to start). The low entry deposit is doable even as I’m trying to aggresively tackle some debt. I’m definitely adding this to my notes as a place to check out, and possibly to the list of things to do with my tax return (#3, after “pay off J.Crew card” and “buy new luggage”)

haha, sounds like a plan :)

do check out index investing as a whole too. it’s usually recommended for those (like me) who don’t know how/care to research funds and stay on top of it all. they perform well over time and requires no work outside of setting it up and forgetting about it. fwiw

Seems like a pretty good investment vehicle to have, reduced fees and you can invest in any stock. I like your portfolio J, but I didn’t see any oil stocks man. They are so cheap right now, you could have knocked it out of the park if oil shoots back up. XOM or COP brother get on it. I personally have BP, but that is an international ADR. Talk to you soon.

hah – I don’t dare time the markets anymore, I’ve learned my lesson on that years ago ;)

I’ve seen Motif mentioned on a couple other personal finance blogs lately. Thanks for sharing more about it! It’s on my radar to try out at some point so hopefully I get to it in the near future.t

Great list of dividend paying stocks. Motif sounds similar to Canadian equivalent of ShareOwner. We’re using ShareOwner for my son’s dividend portfolio so all the dividends can DRIP and grow. :)

I know you are! I saw that article and really enjoyed it :)

Here it is for everyone else that wants to check it out:

http://www.tawcan.com/creating-legacy-dividend-portfolio-kids/

I also like Motif, or shall i say i like the idea of MOTIF since i don’t currently use it. The reason i don’t use it is because i invest every month just a few hundred dollars. I don’t want to pay $10 a month in fees. Instead i purchase DRIPS directly through the company. As an example i purchase Disney shares for $200 a month and $100 in Mircosoft and avoid all the fees by going directly through them. it is more places to go to manage all these drips i have especially if i were to have 10 like you. Mint.com helps me keep an eye on all of them though.

Another great idea!! No shame in that at all :) It’s too bad they don’t give you paper stocks any more – those were so cool!

I can’t wait to see how your portfolio performs especially since I have heard that the dividend investing trade has passed it’s prime and many people feel that dividend payers are too rich since money has been going into them the last six years as bonds yields have dropped like a rock. Hopefully you didn’t time your dividend buying like you timed your home buying. :-) PS: You know I still love you, right? :-)

Hah! I never time the market anymore. That house deal BLEW!!!! What a horrible way to learn a lesson, ugh… On the biggest financial purchase of our lives!

I know you wanted something different for your dividend portfolio but did you ever considering just using the Vanguard Dividend Appreciation ETF (https://personal.vanguard.com/us/funds/snapshot?FundId=0920&FundIntExt=INT) or the Vanguard High Dividend Yield ETF (https://personal.vanguard.com/us/funds/snapshot?FundId=0923&FundIntExt=INT#tab=0)?

Either of these options seem to me like they would accomplish exactly what you are trying to do without the hassle of managing/buying individual stocks. Both of these seem to pay out about 2% or more in dividends each year compare to current purchase price.

Dang, no – I didn’t see those. I probably would have made the same call just for testing/learning purposes, but in general yes – I much prefer Vanguard indexing! And that’s bad ass that it combines dividending with it, thx for the heads up!

I’ve often thought of going that route myself, (through Vanguard dividend mutual funds) but I struggle with the decision. The reason being that the dividend yields on the funds tend to be somewhat low, at about 2%. Even some of the motif “funds” offer upwards of 3%. I know it seems like a small difference, but if you’re looking for your dividend income to bring in say, $500-$1000 a month, that one percentage point can make a big difference in how much you need to invest.

Very cool! A few years back I did some dividend investing with some fun money I had. I started with the Dividend Aristocrats list and made my choices from there. I chose five stocks and two of them were JNJ and Coca Cola. I haven’t done more dividend investing since (we’re Vanguard target fund people) but I’ve kept my original investment (about $5k) in those 5 companies and I check in once a year to see how they’re doing. It’s fun!

Dividend Aristocrats sounds like some posh club I’d like to belong to, haha…

Haha. No, Dividend Aristocrats are companies that have raised their dividend every year for the last 25 years or more. They’re not necessarily the highest dividend payers, but they’re the most consistent.

Congratulations on diving back into the market!

I’ve checked out Motif’s website and it looks brilliant! So reasonably priced. Building a “portfolio” or “fund” for only $9.95 is unheard of here in Australia! Hopefully they decide to expand down under.

Unfortunately I don’t think you’ll manage to beat 33% return using a dividend portfolio, but you’re certainly making a great investment decision.

My $10m retirement plan is very focused on building huge passive income through dividend investing.

33%???

I don’t dare try chasing too high returns because I know the opposite will happen fairly often as well ;) I’m totally cool with “good enough” returns year after year.

J$,

Thanks for including me!

It’ll be fun to see how the Motif works out. Obviously, we’re not in this for one-year gains or results, but it’ll be fun to see how it turns out. :)

Appreciate all the kind words as well. Really glad to be considered for this project!

Best regards.

Really glad you were up for it, man! Helped me put this whole thing in perspective more and made it more fun for me. So thanks :) And for replying to my readers’ comment too above, awfully kind of you sir. Nice to have wonderful friends online.

I love Motif and use it for our “play money.” The majority of our investments are with Vanguard in index funds, but I love the idea of investing more specifically in certain sectors. Several mentioned investing according to their personal ethics and they have motifs specializing in everything from socially conscious companies to solar energy, etc. For the political among you, they also have ones for each major political party. It’s a fun way to use extra money though they also have IRA options as well.

Hah! Political?? That’s too funny… Different strokes for different folks I suppose :)

I don’t know why people are so fussy about owning Phillip Morris. It is a solidly managed company and supports the economy they are in. If people are going to talk about Phillip morris being in a terrible business that kill people then they should really look at all the child labour, sweatshops operated by other unethical companies. What about Mcdonalds or Cocacola targeting young child? I thought it is democratic country that we all live in.

Regards,

BeSmartRich

Good things to consider, indeed ;)

I recall reading that Motif didn’t have automatic dividend reinvestment. I don’t recall any other limitations, and it does seem like a great way to start dividend investing since I’d want to be in the FIRE camp (someday).

I’d be excited to see what else you find out about using Motif, though.

Interesting, I didn’t catch that actually? That would suck if it just paid it out like that instead of re-investing… I’m gonna have to ask them this, thx for bringing it up!

While I continue to mourn the loss of the Baby Tracker, I have to say that I will be watching this project with interest, I hope it works out for you!

Hah! I have to admit, I do NOT miss tracking that thing whatsoever ;) Was such a bitch! And, also, probably SUPER scary at this point with baby #2, haha… Glad you enjoyed it while it lasted though!

You always bring the Fresh New. This challenge sounds super fun!

I just rejiggered all my retirement fund holdings. Man, was that hard! I also rely on other people’s advice as I still feel like I have no clue what I’m doing, beyond the basics like the standard buy no load, low fee index funds, watch your asset allocation and maximise the tax efficiency, etc. advice. Actually choosing the funds from those that meet the above criteria still feels like a crapshoot to me! Would be fun to play with funds that I’m not relying on to sustain me in my old age.

Now to figure out what the H is that challenge leader doing to get 16% returns…amazing.

I believe the leader in this contest only has one stock in his motif. Not sure how it was picked, but it was certainly picked right.

@Sense – This is why 99.999% of all my money is invested in Vanguard index funds :) You figure it out once and then leave it be and go drink beer or something, haha…

Oh man. I’m staying away from this one. I feel like dividend investing is the current trend, but then again, I don’t have as huge of a NW as you!

Maybe when I’m your age I’ll have as big of a load to sit on, but at least you’re only investing $500.

Did you just say “at my age?” *hangs head low*…

Thanks for the post! I dabble in investing every now and then, and I “lose” too but I think in the end… it’s better than doing nothing, and all the long term benefits will add up even if you don’t win your contest!

How fun and nerve wracking at the same time! I’m invested into mutual funds via Betterment (slow going on returns with the stock market being so volatile) but I don’t think I can handle the stress of individual stocks. How often are you checking your investments? Once a day? Twice a day? More???

So far, never :)

I haven’t looked since putting this post together and I probably won’t outside of whenever I do an update on it, haha… So maybe once every month or two?

I don’t get scared by the market really so doesn’t matter to me…. I just get more curious if anything.

Great round ups, really enjoyed your article. Thanks for sharing about this Creative Way to Invest. It’s really useful and helpful way before you invest.

>I HATE the thought of dealing with taxes on all this stuff and messing with the simplicity of my system, but again I know I need to wise up on this stuff or else all my millions will be tied in retirement funds I can’t touch until I’m old and gray!!

IRS rule 72-T. Learn it; love it. Prosper

I keep hearing about that thing… guess it’s time to man up and read about it, thx :)

There are companies out there that pay dividends monthly also. You should look for those too!!

hah – really?? That’s kinda cool.

Realty Income Corp. is a big one (ticker symbol: O). And they’re pretty reliable.

J Money, it seems like you invested in different companies. I just have some investment in Coca Cola and Unilever. What else can you suggest? I can’t pick one or two among the ten.

I’m the last person to ask, sorry :(

Check out http://DividendMantra.com and see if any stand out to you!

I’m convinced, I’m giving this ago as well. Here Here to the 500$ dividend test.

Really? Awesome!

Let’s compare notes every month :)

I just added their high-yield dividend motif and switched out a few for KO, PG, and JNJ. It was well worth it for me and I like where it’s heading. I do wish I would have waited just one more day as the market dropped 300 the next day after I made the trade. It’s life!

Oh man, you know we can never time it right!!

At least you didn’t buy your house right before it crashed like me – (UGH.)

Good luck with your dividend portfolio!

Is there a prize for the winner, or just bragging rights? :-)

No prize outside of the fun and learning experience :) Though, we should do something like the loser has to buy beers for all of us! Haha… (Or, maybe the winner should in that case?)

Good stuff man! I’m just getting back into dividends myself. If I had to pick one, I’d probably go with JNJ as well… But right now, I’m watching oil with the most interest ;)

I’m watching it too… but only when I fill up my gas tank :)

Direct response from Motif, reference your comment, “You can learn more here if interested: MotifInvesting.com (that link will give you up to $150 if you end up signing up btw – a nice start to your account!)”

Thank you for your recent correspondence regarding our $150 trading promotional offer. I added you to the promotion list so when you meet the full terms you will receive the bonus. The bonus is usually paid out 70 days after your deposit date.

I thought it may be helpful for you to have the terms of this offer so I’ve included them below. Please review and if you have additional questions, feel free to give us a call. We can be reached M-F between the hours of 9am and 6pm ET at 1-855-586-6843 or by email at service@motifinvesting.com.

The cash bonus offer applies to new, approved Motif Investing brokerage accounts opened and funded with at least $2,000. The new funds must be posted to the account within 30 calendar days of account opening, and must remain in the account for 45 calendar days. The total bonus will be based on motif trades made within 45 calendar days of funding, as follows: 1 motif trade will receive $50; 3 motif trades will receive $75; 5 motif trades will receive $150. A motif trade is defined as a completed purchase or sale of a motif for $9.95 commission. Individual stock trades will not be considered as part of this offer. The cash bonus will be credited to the account within 30 calendar days after the end of the 45-calendar-day period.

Commission fees are not reimbursable as part of this offer. This offer is not valid for retirement accounts, such as IRAs, and cannot be combined with any other offers from Motif Investing, and is not transferrable. Limit one account bonus per household. Motif Investing reserves the right to terminate this offer at any time and to refuse or recover any promotion award if, in Motif Investing’s sole opinion, it was obtained under wrongful or fraudulent circumstances, that inaccurate or incomplete information was provided in opening the account, or that any terms of the Account Agreement have been violated. This offer is not applicable to associates or affiliated associates (including contractors, interns and temporary employees) of Motif Investing and their immediate family members. Standard pricing: $9.95 per motif and $4.95 per stock. Other fees may apply.

Best regards,

Matt Bear

Motif Investing, Inc.

Great info – just updated the post to alert new readers that hit the article.

If you are looking to add to the portfolio – I search for undervalued dividend champions every month:

http://www.myjourneytomillions.com/articles/february-2015-dividend-watch-list/

Also, does Motif reinvest dividends for you? That will change your returns.

cool, will check out – thx!

And looks like they don’t! Ugh… Didn’t realize that earlier… you still get the cash in your account which you can then pick up more with of course, but it’s not automatically re-invested :(

Here’s what their FAQ says:

“If the stock in the motif you own pays a stock dividend, we will credit the additional stock shares to that motif. If the dividend is in cash, we will credit the money to your account and it will be reflected in your account balance. We do not offer dividend reinvestment at this time.”

https://www.motifinvesting.com/how-it-works/getting-started-faq

Just took a look at MotifInvesting today… Love it by just looking at it.. signed up.. Thinking this will be a Swing Trading account. I like how they group up stocks then I can pick and choose. Already have a plan to create my own Motifs.. Earnings Winners for 1 – 3 months Swing trades… Already have my Dividends accounts with E-trade…

Nice! Let me know what you think after a few months :)

Hi, I’m new to the investing world and I just recently signed up for motif investing. I’m really new and I am slowly learning how to invest. I found Motif Investing from Mint where I manage my budget. In my Motif account, I made 3 Motifs so far, and only bought one out of the 3 cause I’m scared to drop more money on something I’m not fully familiar with. Right now, I’m just watching the 3 Motifs I made especially the one I personally bought. My question is am I on the path? What else do I need to do?

So hard to answer without knowing you, your goals, your risk levels, age, etc, etc. But do know this – investing in something is better than investing $0.00 in nothing! :) You’ll learn and figure it out if you keep googling and reading blogs. Check out some of the links in my blogroll as many of these bloggers talk about investing and such:

https://budgetsaresexy.com/blogroll

I’d also consider looking into index funds and similar (even target date funds) so you can invest and be less active in it if you’re worried about what you’re doing. Whatever you do just don’t chase the “hot” stocks! You’re in it for the long haul and won’t be touching the $$ for years and years and years (hopefully).

Good luck, and keep researching!

Hey, J. Money, so how did the competition end?

I think I landed around the 13th place of the group. So not that well :) Then again, it’s all a long term thing than short, so wasn’t really planning on outperforming many much. I just xferred out my money last week so I can apply it back to the #1 post – my Vanguard index fund :) Was a fun one to try out though!

Thinking about opening an account with Motif and in doing my research I can across your blog. What would you rate this experience on a scale of 1-10 and is it good for long term investment?

I think if you like researching and buying stocks it’s a great platform. Especially the more creative you are. If you’re a “set it and forget it” type of person, I’d recommend going elsewhere and a different investing strategy altogether.

So hard to give it a rating out of 1-10 just cuz it depends on what you’re looking to do :)

Is it possible to modify the limit price on an open stock order in Motif Investing.

FYI, starting on May 15th, 2017, Motif will begin charging $10 semi-annually on inactive accounts with a balance of less than $10,000.

You’ll probably want to update your article to reflect this.

Good to know – will update, thanks!

(I’ve since pulled my money from them and went back to indexing full-time, so not “in the know” anymore… though it was a fun experiment for a while :))

Hello J. Money-

I’ve been thinking investing in motif platform. However, since you had experience with motif. I just have a couple of questions.

Q1: What is your starting investment?

Q2: How long you had it with Motif?

Q3: What is the Monthly, Yearly ROI?

Thank you in advance.

Have a Magnificent day of living.

Joel

I started with $500 and only tried it for a year – way too early to be able to tell if it was successful or not really, I just eventually wanted to streamline all my accounts into one spot and main strategy so I pulled the money out and added it to my index fund elsewhere. I didn’t even look at the monthly or yearly ROI but I feel like it was still around $500 by the end? I remember it hadn’t moved drastically one way or the other.

(Keep in mind though that it’s all dependent on the stocks you invest in – not the vehicle you use all the way (ie motif or elsewhere). If you pick crap stocks they’re going to be crap no matter where you invest, haha…. Which again is why I went back to index investing – I like having my money across the entire field of stocks and I’m fine with average market gains :))