[Hey y’all! I found out that one of my favorite podcasters has been tracking ALL of his expenses for over 6 years now, and asked him if he’d give us an inside look at them. You know, cuz we’re nerds like that ;) Apparently he’s never looked at the overall picture before, so we’re the first people to see what’s hiding in the numbers! Enjoy!]

In January 2010, I was wrapping up my last few classes of my MBA at Pepperdine University in beautiful Malibu, CA. One of my first assignments in the new year was simple:

Track all of my income and expenses for one week and write about the experience.

The only rule: to track every single penny in and out of my life, whether it was spending thousands on a car or finding a quarter on the street.

This was right up my alley – as a data-obsessed Excel nerd and Myers-Briggs type ISTP, also known as “The Craftsman,” I quickly built a spreadsheet to help me track it all, complete with pivot tables to summarize the data by date and category (read through to the end to get the Excel template).

Over six and a half years and 7,500 rows later, my spreadsheet is alive and well, still summing up my income and expenses into pretty charts.

While I watch my overall financial health every month and year and break it apart by category during tax season, I’ve never sat down and looked at the key takeaways — that is, until J. Money asked me to.

Today, I’m going to do something I’ve never done: I’m going make my expenses public and share 7 surprises of this experiment:

Surprise #1 — Living with Roommates Didn’t Save Me a Ton

In the last 6 years, I’ve lived in 6 different places in Southern California and in 4 different roommate scenarios. I went from a “Seinfeld” phase (living alone in a 1 bedroom apartment in Santa Monica, CA) to a “New Girl” or “Golden Girls” phase when I had 3 roommates at a house in West Hollywood, CA, and everything in between.

Yes, the rent & utilities were significantly cheaper in the latter ($13,500 vs. $17,700 living alone), but living with roommates brings in additional expenses:

- Cleaning was difficult, so we got a housekeeper (-$650/year)

- My groceries went up because not everything gets split perfectly and food & supplies might “go missing” (-$250/year)

- Restaurant expenses increased because I was around more friends and acquaintances and was pressured to go out with them (-$750/year)

- I spent a lot more on “gifts” (-$500/year)

Adding those factors in, I was still saving $2,000/year on rent, but that only equates to $166/month, which I probably could’ve negotiated when I lived alone, or found a comparable apartment for that much less. Also, I wasn’t sharing a kitchen, family room space, and parking—instead, when I was living alone, I used every square inch of my apartment and lived on my own terms.

If you’re deciding to live with roommates, these are things to consider. Is it worth it to save $100-200 on rent to deal with the complexities of having one or more roommates? For many people, like me, that extra cost makes sense… or maybe you’re an extrovert and simply love having people around.

Surprise #2 — Having a Significant Other Has Been Expensive For Me

How does your relationship status affect your finances? Here’s how it affected mine.

When I was single, I spent somewhere around $1,000/year on gifts, but once I was in a relationship this more than tripled! It didn’t mean I was spending a lot more on my girlfriend, necessarily, but when you’re a couple, you get invited to all sorts of engagement parties, weddings, birthdays, baby showers, and more, and you’ll likely be chipping in for the gifts as well. Add in gifts for your significant other and his or her family, and it’s easy to see that you’ll be spending much more than normal.

But that’s not all. While your groceries and restaurant expenses could stay the same if everything is split evenly, you’ll likely attend more events as a couple, so it’s safe to assume that expenses will go up in multiple ways.

For me, the gifts category was the most noticeable: I spent a whopping $3,600 in gifts in 2015 compared to $765 in 2010. While a good portion of the gifts went to family, I dove in to the line level and found that this was indeed mostly due to the change in relationship status.

Surprise #3 — Cat Ownership Isn’t as Expensive as I Thought

This clearly depends on your parenting preferences, but luckily, I’ve done it both ways:

In 2014, I was very relaxed with my cat—maybe 1 vet appointment, she was fed dry kibble, and she didn’t need a litter box because she went outside. She was also old enough that she didn’t need toys and distractions. Cat-related expenses were very minimal.

Cat bills in 2014: $312

Compare that with the very next year, when I took a more proactive approach: I fed her high-quality, raw cat food and had a couple of her broken teeth extracted by the vet’s recommendation.

Cat bills in 2015: $1,375

That’s a $1,000 difference, but even in the more expensive case, $115/month, or less than $4 a day, to give my cat the best and have a furry friend around was worth it for me.

Surprise #4 — “Gold” or “Platinum” Health Insurance Hasn’t Been Worth It

Being self-employed is expensive. It feels much worse than receiving a paycheck from a company because I have to pay quarterly taxes on my income, which is about a third of my earnings. On top of that, I have to pay for my own health insurance.

As a hypochondriac, I opted for the “Gold” plan, thinking that it would be better long-term. But just 3 years after quitting my steady job, I’m worth $8,800 less due to monthly health insurance costs, and to add insult to injury, I’ve only used my “awesome” gold plan a couple of times.

Average cost per year: $3,500, or roughly 10% of my total expenses

Surprise #5 — Tax Season is Not Only a Breeze, But Also Fun!

I don’t think you’ll hear this anywhere else… Ignoring quarterly taxes, I enjoy tax season. This is what it consists of:

- Sort my spreadsheet by date and category

- Eliminate the categories that aren’t applicable

- Send it to my accountant

Done. This whole process takes a few minutes and it’s fun to see the year as a whole.

Surprise #6 — Despite the Odds of Winning, Playing the Lottery Makes Sense (to Me)

Everyone has their opinion on this, and mine is somewhere in the middle. I only play the lottery if the expected return is greater than the cost of the ticket.

Basic math shows that your odds of winning the lottery, or at least matching all the numbers, are horrific. But basic math also shows that when the lottery reaches certain thresholds, your expected return is actually really good when you take into account the smaller prizes. On top of that, the law of utility makes a great case: even if you played $1 on the lottery twice a week, you’d only be spending around $100/year.

Is that going to ruin your finances? Probably not if you’re reading this article. However, if you won, would it affect your life? Most definitely… and that’s why I play. The lottery also gives back to schools which I like.

As for the numbers, I’ve spent less than $400 in 6 years on the lottery and won back 10%. Is $1 a week worth a chance to win $100,000,000 or even $1,000,000,000? For me it is.

Surprise #7 — The Juicy Details Aren’t Really That Juicy

The numbers are fun and tracking finances to this level of detail makes tax season enjoyable, but to me, the biggest impact of this experiment has been my attitude.

Just one week of tracking every penny in and out of my life was enlightening, but maybe not in the way you’d expect. I thought I’d find insights about the actual data and where I could save money, and while that was somewhat true, the bigger lesson was one of awareness.

Every time I spent any amount of money, I was thinking about my new spreadsheet: the fact I’d have to spend time updating my table for this trivial purchase, what it would mean to my balance, and if this expense was actually “worth it.” This simple homework assignment threw me out of “auto-consumption” mode and made me question every purchase I made. It’s like a meditative practice for minimalists.

After 6 years of doing this, that awareness is stronger than ever. I know what I can afford. I know what it’ll mean if I make a large purchase or if I take on a new monthly expense. It’s easy to see how this will impact my bottom line and my future finances.

My Challenge For You (And The Downloadable Template!)

This jolt of mindfulness and awareness is the reason I ask listeners of my podcast to go through this challenge. Track every penny in and out of your life – just for a week. Try it. There’s no harm.

If you struggle and fail, no worries; but if you succeed and you can keep doing it for a month, a year, or more, your awareness will continue to improve and you’ll know exactly what you spend & make and more importantly, what you can afford to spend or make.

Does it make sense to move? Can I afford to quit my job to start a business?

These questions are easy to answer when all the numbers are nicely summed up by category. Best of all, it only takes a couple of minutes a day to log your receipts if you stick with it.

While I only give away my spreadsheet template to listeners of my podcast, I’ve made it available to Budgets Are Sexy readers today. Grab the spreadsheet here, complete with macros (Excel automation) that I hand-coded myself, and watch the video tutorial here.

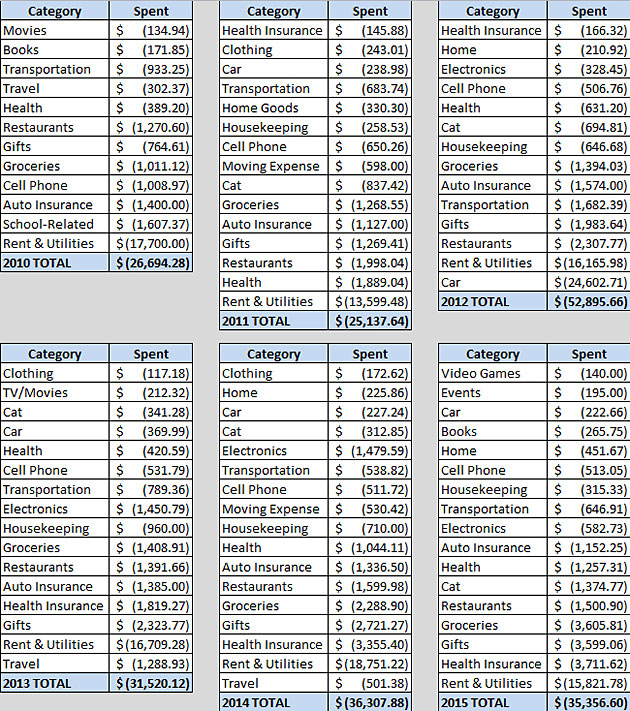

Snapshot of All My Numbers

Let’s face it… this is probably why you’re still reading this article. You want to see my actual numbers and compare it to your own numbers, whether they’re in your head, on Mint (or YNAB or EveryDollar), or in a spreadsheet.

Well, alright, but all I ask is that you don’t judge me. I’m open to advice and constructive criticism, but let’s keep this positive. I’m not putting all this financial information up just to be torn down. :)

Feel free to look over my numbers and share your ideas for improvement, your own experience tracking your income & expenses, and any other relevant commentary. I’ll be here, stalking the comments.

By the way, I’ve taken out yearly expenses that were less than $100 (like the lottery expense or my incredibly cheap haircuts) and more rarely, stuff that I didn’t think would add value to this conversation (like accountant fees, driver’s license renewal, etc.), just to keep this as clean and relevant as possible.

Now that that’s out of the way, enjoy this window into my personal life!

*******

Justin Malik is a serial entrepreneur who launched a podcast as a social experiment to help come to terms with performance-based social anxiety. In his podcast, Optimal Living Daily, he reads to you from the best blogs he can find, covering personal finance, personal development, minimalism, and more (with author permission of course). Bloggers read on his show, and his spin-off podcast, Optimal Finance Daily, include J. Money himself of BudgetsAreSexy.com, IWillTeachYouToBeRich.com, MrMoneyMustache.com, TheMinimalists.com, Sivers.org, MarcAndAngel.com, and many more. Learn more at OLDPodcast.com.

Get blog posts automatically emailed to you!

Tracking every penny for six years is seriously impressive, Justin! Your comment about health insurance is reassuring. I’m embarking on the self-employed, buying my own insurance path at the end of the month. My tendency is to choose the higher tier, but that probably doesn’t make the most financial sense in the long run.

Yep, unless you have a pre-existing condition, I don’t think this makes a lot of sense. If you’re healthy, the money you save not going to the doctor now will pay for some “extra” costs that might come up later. Thanks for the comment!

Nicely done Justin. I’m a fan of excel. It’s my primary tool I use to keep track of my finances. Looking forward to giving your spreadsheet a look. Amazing once you get organized with a bit of data how mindful you can become.

Really interesting about the roommates and the relationship expenses. I think that many people just assume “instant savings” when they think of situations like this but when you actually do out the numbers as you have, they may find out that their expenses are crazy! The power of a spreadsheet or having some kind of budget to track expenses (and then looking at them of course!) And don’t make assumptions cause…(we all know how that ends!)

Good for you for tracking your expenses so closely. I’ve been doing that myself for over 10 years. Like you said, the awareness it brings is pretty incredible because the data is real and concrete… You can’t hide from it. But what’s also pretty neat is seeing how things change or evolve over the years. Good post, thanks for sharing!

Yup! The numbers never lie :)

I definitely agree with #7 on this list. Next week will mark the 6 year anniversary of my tracking every expense that we have made (I started just after getting married). And the level of accountability that it provides is by far the biggest difference that I’ve seen it make in our spending. It helps hold us accountable to ourselves and each other to know that any purchase, no matter how small, is going to be entered in and always be there. Purchasing decisions are no longer just a one transaction experience with us and I often see myself turning down purchases simply because I don’t want to have to enter it into the spreadsheet and have it as a stain on my record.

And thanks for sharing the numbers, I’m impressed at how little variance you’ve had from year to year. We have seen a huge variance in our numbers over the same amount of time as we’ve gone from newly wed college students to homeownership with 2 kids. Ours ranges from $10,327 in 2012 up to just over $42,000 in 2015.

Thanks for sharing.

Fascinating!! You need to share all of your #’s now as an “Anniversary” present to your spreadsheet :) And if it makes you feel better, our expenses have blossomed from engagement to married with two kids too – ugh. I think I need to get back to tracking it all manually myself, to be honest – it’s been a while.

Wowzers! That is some crazy variance. Yeah, my situation, despite moving 6 times, hasn’t changed that significantly.

I agree that tracking is great for awareness. And that premium health insurance isn’t worth it for people who don’t get sick/go the doctor often. We’ve calculated that “worst case” health scenarios usually pan out about the same financially across the different plan options. We even had our second child on a high deductible HSA plan.

Great post and thanks for sharing the spreadsheet!!

I love the level of detail you have here. I follow a similar approach with my own excel file so I’m curious to see how our two approaches compare!

+1 for cat ownership! I was never a cat person until I started dating my girlfriend. Relative to dogs (also love dogs), they’re extremely low maintenance and don’t require much of anything, at all! Amazon boxes tend to be a toy of choice, or my shoe laces…

Haha YES to Amazon boxes!

I review our expenses on a monthly basis, more as a quick review to watch trends and see if we hit our goal.

Can especially relate the gift buying trend you noticed. Between baby showers and weddings alone we have spent over a grand just on gifts this year!

Wow, that show’s incredible discipline that you’ve been able to track every penny for so many years manually! I have about eight years of similar data that I’ve been keeping, but it’s in Quicken and downloaded every month from my financial institutions. I don’t really keep track of any cash expenditures less than $100 or so.

I like how you went digging through the data for insights, it’s not much use unless you look through it to see what you can figure out!

Thanks again for sharing!

Your turn to divulge :)

What you’re doing makes more sense… I think because I started tracking every penny, it became an obsession. But since I left out expenses lower than $100 in this post, it just shows that those expenses don’t really matter that much. Sure they add up over years, but when looking at the big picture, it’s pretty insignificant. Thanks for sharing!

Pretty cool….What I find interesting is the “dramatic” increased cost of health insurance AND yet cell phone costs over the years stayed relatively “flat”. I wonder what made health insurance go from $166 in 2012 to $3700 in 2015?

Employed to self-employed?

What J$ said… that’s when I went self-employed. I was never very grateful for health insurance through my workplace until I became self-employed!

As for the cell phone, I’m on a family plan and that hasn’t changed much over the years.

This is so cool! My husband and I can only go back two years, but I love scrolling through the archives. My husband has actual hobbies…KIDDING! I really think the takeaways are huge here. I will not be showing him this post, though, as I do not think we’re home enough to be pet owners. He’s currently shifted his sights from dog to cat, and this certainly would fuel the fire. Neat insights!

Haha.. yeah, if you’re pretty relaxed about the cat, it can be relatively inexpensive, but you never know when a big expense might creep up with those crazy felines!

Wow! What a great assignment from your teacher. :). Awareness is definitely the key here. I have been tracking my assets since 2012 and only started tracking expenses in 2015. What a difference this year has made now that I have something to compare it to! Ive challenged myself to spend less on groceries (bye bye WholeFoods! ) and I try to reduce my energy consumption each month. What a wake up call!

Thanks for sharing!

Groceries are our silent killer too – esp after having kids!

Lots of good realisations in there Justin and I think a lot of people could identify with what you found. I agree completely that cats aren’t that expensive and totally worth the small expense and cuteness. Plus they’ll track down any mice/rats if you have them (and bring you a nice treat).

Nice job tracking all your income and expenses so thoroughly!

Tristan

Funny you bring that up. My cat, pictured in the post, used to do exactly that. The only problem is that she would catch baby mice ALIVE and bring them into my room, often setting them on my bed… this was not appreciated! :)

Being in a relationship means spending more and eating more! Worth it for love, though!

Let me start by saying I gasped for a second at #2, thought you were about to dig yourself a deep hole on that one for a second. But you didn’t take it the direction I thought it was going to go.

Health insurance is a rip off. Let me start by saying as a self employed person I also feel your pain. My silver level HSA is over $1000 a month for family. If it weren’t for the triple advantage HSAs provided I would opt for a health share ministry plan which is something like $400 ish a month for a family. My wife also likes to rush to the doctor’s office for every minor thing, which is another reason I haven’t done it yet. That and the HSA Its basically an extra retirement account for me which I don’t want to give up.

For real… We just stopped spending $950/mo ourselves now that my wife got a gov’t job. So crazy.

Yes, my girlfriend’s jaw dropped when she read #2, but I tried to put out that fire by explaining that it wasn’t exactly what it sounds like.

Thanks for sharing that health insurance info, too.

Very interesting – thanks for sharing! I used to track everything in Excel, but I actually have found it easier to use Personal Capital. I like that I get to see my entire financial picture in one place. And I completely agree with you on the mindfulness/awareness piece, which is why I try to check PC daily.

I love cats and wouldn’t change a thing, but they can get a lot more pricey when they reach the geriatric stage. Before we said goodbye to one this winter, we had easily spent $5,000 on surgery, biopsies, medications, prescription food, and general vet care, in his later years. My fingers are crossed that yours stays healthy and happy for many more years!

I want so badly to love Personal Capital like everyone else but for some reason they insist on doubling up my automatic transactions and so it looks like I spend at least 1/3 more than I do each month. I’m about to go back to tracking manually via Excel just so I have honest numbers…

Has anyone found a resolution for this issue? I can’t be the only one (and I know I’m not based on their community support forums) but even though I’ve reported it and it has been moved up the ticket system, they don’t seem to be in any hurry to fix it…

That’s so annoying :( It hasn’t happened to me, but I’m more of a spreadsheet tracker anyways so I don’t pay attention to it as much. I wonder if it’s tied to a specific bank or two?

Now that is a very interesting thought I had not considered. It is a smaller bank. And that is very possible that it has to do with how this bank handles transfers. I shall do more investigating. But that makes it even more likely that I shall have to go back to my spreadsheets since I’m not going to change banks over this!

I’ve never tried Personal Capital, but I’m so obsessed with my spreadsheet & Excel that I probably won’t move over anytime soon.

Yes, cats can get super expensive later. I actually wrote this post after my cat already passed away… I just didn’t feel like mentioning it in the post. But thank you for the good wishes and nice comment. :)

I love your spreadsheet! Having roommates you don’t like will decrease your costs since you are not trying to hang out with them, but also decreases your quality of living since you have so much time with people you don’t like. I absolutely spend more on gifts and restaurants in this relationship, too.

I use Quicken and have for 20 years. I’m planning on doing a similar sort through to this but don’t expect many surprises as I look at the trends rather frequently.

As for the cat not being as expensive as thought, what did he think? $1,400 a year seems expensive especially since cats live long and the last few years is where the major costs are.

Even if you blend the two numbers and say it’s $700 a year, a 15-year cat will cost $10,500 plus any last years treatments which could add a few thousand dollars. I’m not saying that’s expensive or that it’s not a good choice, but did he think a cat was going to cost $30k, so he’s ok with $15k?

Tell me you’re going to share all your totals over the 20 years too?? Would be so fascinating! And take major cajones to divulge as well ;)

Thanks for the comment!

The headline that it’s not as expensive as I thought refers to the “relaxed method.” Whenever I tell people that it was costing me $25 a month the third year I had my cat, they’re shocked, and so was I. Most people think it’s way more expensive than that on a regular/monthly basis and that’s why I wrote about it. I don’t look at it on a span of 15 years because indoor/outdoor cats have an average lifespan of like 5 years, not that I’m a fan of letting them roam the streets.

I definitely get what you’re saying–if you take great care of your indoor cat, then yeah, you’ll fall into a different bucket.

Tracking every penny for that long is pretty darn impressive! Great job! Number 3 and Number 6 resonated with me. I’ve recently read a few articles regarding the cost of pet ownership, and for me, it’s 100% worth the money! And buying a cheap lottery ticket every week? I definitely do that! :)

Thanks for stopping by, Ashli! Hard to not click on your blog with a name like that ;)

This is great! Thanks for sharing your numbers!

For me it’s #7. My spreadsheet creates accountability and awareness. Anytime I make a purchase, in the back of my head I know I’m going to have to report it (even if it’s just to myself). It’s always a game with me to keep my categories as low as I can.

I completely agree that tracking your expenses makes you second guess every purchase. I like to see how low I can keep my expenses, so every purchase I make is like “What is my expense total for the month going to be after I purchase this?” It keeps me from buying stuff I don’t need!

My expenses may have gone up a little when I started dating Mr. Frugal Turtle due to the extra driving to see each other and the meals out. However, since moving in with him, my rent has dropped, I need less gas for driving, and we hardly ever eat out any more. He’s definitely helping me save money!

Sounds like you found a keeper ;)

Now that is commitment! Tracking numbers so closely but be scary but exhilarating at the same time as you see the true cost of your habits. I have only been doing it for 2 months now but it exposed how much money I was spending eating out due to having roommates.

My girlfriend and I live roughly 4 hours away from each other so gas is a killer and whenever we visit each other we always do activities that can rack up money but somethings are worth the cost ;).

That’s awesome that you’ve been tracking all the data this long in your own spreadsheet. I’ve been tracking to the penny for over 10 years now, but in Quicken. I think you’ve found some very interesting takeaways about roommates, significant others and pets. But the most important one is #7. I know when I spend something, not only do I take a moment to enter it into my data, but it will show up again when the wife and I review the monthly budget, and again in the future because we compare against past months and use 12-month rolling averages. If it’s going to be immortalized in the data, it better be worth it!

I want to see your data!!!! New blog post, please! :)

#7 is the big one for me too. We spent a bit too much sometime and we’d see it when we go over our numbers at the end of the month. Usually we spend a bit less next month and it all even out. If we don’t keep track of our spending, we wouldn’t be aware of overspending and it will keep happening.

I only buy a lotto ticket if the prize is over $400M. :)

You’re like my wife. Apparently a few hundred mil just doesn’t do it for her – needs to be at least half a billion for her to get out of bed :)

Wow very impressive. Interesting to see that living with a roommate didn’t save you money. Have been tracking every penny for over 5 years now. It’s great to be able to go back and compare the numbers.

Very insightful about the Gold and Platinum health care not being worth it! I’m spending a fortune on a Platinum health care plan and it hasn’t been worth it. BUT, isn’t not being worth it a GOOD thing since that means we’ve been healthy?

CATS! I tried a cat, but had respiratory issues 3 months later. Had to give it back :(

I’ve stopped counting my pennies and more focused on making more than the government and life can take away every day.

Sam

Yeah – insurance is one of the only things we spend money on that we hope to never use!

This is pretty amazing to see. Thanks for opening up to the online world to show us what you’ve learned and not holding back. The first surprise about roommates was a surprise to me too, but I think you bring up some very good points. Depending on what you value having your own privacy at and not having to share living areas all the time I think it makes sense for people to live on their if they can afford it. I live on my own now after graduating college and I don’t think I’ll go back to having a roommate again. I had never thought of having roommates as a reason someone might spend more on restaurants and entertainment, but it absolutely makes sense.

Again, awesome stuff and thanks for sharing!

Yep, the roommate scenario can get expensive real fast if the roommate becomes unemployed, lets their boyfriend/girlfriend practically move in, or move out in the dead of night without paying rent. Also, having a roommate can sometimes be a hassle. Best scenario is a roommate who works opposite your schedule.

Did all that happen to you?? Yikes.

J Money,

Hilarious on the additional costs from a relationship as it is SPOT ON. Easy example – the lady and I started dating last year, a Florida wedding of her friends got lopped in and next thing you know I’m spending $500 over a weekend. Fun, yes. A cost that I’m used to having? No. Then the weddings cost double, etc.., the going out to eat, trying new things. All are great, don’t get me wrong, but cannot beat the statement of – Yes, money being spent has increased. Nuff said.

But – I’ve tracked everything for around 4-5 years now and love it, love knowing my quick 2 second internal calculation of the impact it will have and being able to make any conclusion on any purchase and knowing exactly how much $ is going in/out and what is left after investing/saving. Keep it going, I sure as hell am.

-Lanny

> Surprise #6

> As for the numbers, I’ve spent less than $400 in 6 years on the lottery and won back 10%.

> Is $1 a week worth a chance to win $100,000,000 or even $1,000,000,000?

Totally agree but you’re selling the “chance” short. Instead should add up the prizes from all those years. Trillions?

Fair enough! :)

Thanks for sharing your numbers, always interesting to see someone else’s snapshot. The roommate conundrum is definitely interesting – I would have guessed a much bigger savings. My gift spending actually went down significantly after getting married – I felt more pressure to spend on friends and family because I didn’t have anyone else to be accountable to. My wife and I also restrict gifts for each other to gifts for the house – an excuse to spend money on something that might be more of a luxury. We bought an espresso machine for one anniversary – it gets used multiple times a day so that was more of an investment!

That’s a great gift idea :)

Interesting article and thinks for sharing the details (I have no idea why we spend so much more than you on food). I’ve been using Quicken “Savings Goals” since 1996 for budgeting (I don’t know if it’s still an option as I haven’t upgraded since 2001). But, I guess I’ve got 20 years worth of data. Interesting exercise trying to pull the data out and look at trends (I’m usually only interested in how much is currently in each category). Unfortunately, some of the data isn’t complete as I have only tracked my “net” income – ie, my health insurance/retirement/etc cost came out before it hit my bank account. I could definitely see a jump in the amount we spent on food in the last couple of years as well any time we had more significant outlays (usually cars)…

20 years is amazing!! Would be so interesting to see what’s hidden in those #’s and how much has changed over the years… I hope you look at it all (and then come back here and tell us :))

Kudos to you for tracking your numbers for so long. I started tracking my money a few years ago, and it has improved my financial situation greatly.

Unfortunately the lottery isn’t the charity ball that everyone thinks it is. :/

https://www.youtube.com/watch?v=9PK-netuhHA

Big fan of your podcast Justin – this is a great habit to employ. I am on year #4 of tracking all my expenses as well. I wish I could get mine as low as yours (head of household, 2 kids, 1 wife, 2 dogs).

Have you ever thought about switching from Excel into something like Quicken? I’ve given it some thought but like the flexibility of using Excel to create graphs, tables, etc on the fly.

Thank you for the kind words, Danny! I’ve never tried Quicken… I love Excel too much. From pivot tables to back-end coding with VBA, I can’t imagine a more customizable solution and I don’t have a solid reason to move over. I find it pretty easy to log a couple of receipts every day.

Thanks for listening to the podcast!

We have “expense reports” going back to 1998. Another Quicken user here. Although I do make our annual budget in excel then enter it in Quicken. Lots of potential retirement scenarios created over the years as well. I like the comparative reports that I can tweak with just a couple of clicks. I especially like watching the changes to our account balances and net worth over the years. Things really took off after getting “Dragonboy” through college and law school. It’s nice to know I’m not the only one who comes home every day and updates the books. Thanks for sharing your spreadsheet.

Almost 20 years now – nice! I hope Dragonboy will continue the legacy ;)

Hey Justin,

Thanks for your template! I’ve been using an existing one (a very crude one which I just devised myself) and I want to insert some of the formulas I’ve been using in my old template to yours since it looks better and has more functionality. Basically, I have a set monthly budget per category (for example, $250 for groceries per month). I have a monthly overview of my budget so I can track if I am already going over the budget of a particular category. Now, I am trying to figure out how to insert this feature into your template. Any tips how to? Thanks in advance!

Yikes… I don’t have a simple solution without diving into the spreadsheet and doing it myself, but that’s a good idea for a future upgrade to the sheet!

Cool info!

I’ve been tracking my expenses for years, but it’s mostly automated using Quicken these days. Your expenses seem very reasonable. Great job keeping the spending in check.

I recently analyzed our spending from the last three years (I have records going back much further, but the last three years are the most representative of our current lifestyle) and it was very interesting. You can check that out here: http://www.fiscallyfree.com/2016/05/retirement-planning-step-1-review.html

Oh wow – you def. break it all down there. Never thought to track “cash withdrawals” like that – I always just put it in “miscellaneous” which I know is a no-no in the $$ world ;) Pretty brave of you to share too after seeing you’re spending $100,000+ a year.

Great article. Love seeing the quantitative analysis backing up the post. Glad I’m not the only one who enjoys the guilty pleasure of an occasional lottery ticket! The part about healthcare is something that I think would make a great post in itself. I’m not presently self-employed, but one of my concerns of going that route is dealing with the healthcare situation.

Justin, thanks for sharing… Great insights! I’ve been wanting to try to start tracking but never find the ‘right time’ to start! This was inspiring… I start today!

Have you ever looked up your professor at Pepperdine and told him/her what an influence that assignment has made on your life? Sometimes receiving feedback like that is all it takes to make your day and to know you’ve made an impact! If you haven’t you should think about it! Love your podcasts too! All 3 of them! JB

Excellent idea!! Sometimes we never know how our words/ideas affect others unless they tell us. I’d be so thrilled if a student shared this with me after all those years!

Good job on starting to track this yourself too – such a big step towards awareness :)

I totally thought about reaching out to him, but then I remembered that he gave me a B in his class and I’m still sore about that. hahaha

It’s amazing how at the end of the year some expenses that seem like a lot, at the time, are actually minor in the big picture.

This is really telling, thank you for being the perfectionist you are! It makes me feel comfortable to track a lot of things in my life, and it’s empowering to see what diligence and awareness of finances can do for someone!

How many people need the inspiration to look at cost as you have illustrated? What a stress relief to be fearlessly honest and empower others to get real about these notions built up by years of assumptions and adopted perspectives. Economic turns can be a media fueled fear factory and the extreme consequences of living beyond means and purchasing frivolously can make some feel trapped by unexpected expenses and even avoid proper medical treatment due to cost. What you provide is a route for anyone who feels overwhelmed about money to redirect their energies and see it in a refreshing and explorative way. Your point of view is a valid and extremely relevant one. Thank you for the tools provided; keep em coming- you’re helping people in a much more profound way than you might imagine. Cheers.

Glad you liked it!! It’s encouraging me to pay closer attention too – and I run a blog on personal finance! :)