Trying to build wealth without tracking your net worth is like not checking the road map because you’re too busy driving. How do you know if you’re headed in the right direction?

My wife and I check our net worth monthly, and it takes a measly 5 minutes to calculate. It’s just a simple tally of all the assets we own, minus all of the debts and liabilities we have. Each month we try to increase our assets while paying down our debts.

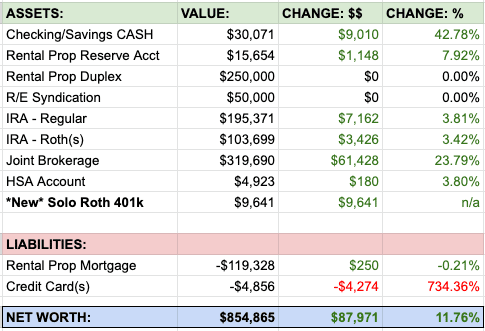

Here is our net worth report from Jan 1 2022 (minus a few private partnerships tracked separately). We share these reports on the blog each month to show how different assets grow and change over time, as well as spark conversations about money and investing – something we all need to talk about more IRL!

Jan 1, 2022 Net Worth: $854,865

MASSIVE increase this month – mostly due to the sale of another partnership rental property that closed in December! 3 down, 1 more to sell!

The sale from this property gave us about $67k in cash, and the other $20k of growth this month came from stock market gains. 😎 In total, our NW grew $87,971 since last month’s report.

December Happenings…

Here are the irregular money moves we made last month:

- As mentioned, we sold a partnership rental property and cashed out with $67k. This wasn’t part of our original tracking, so we’re adding it now because the funds will be put into our brokerage accounts. 🏡 → 📈

- Wifey received a teacher appreciation gift of $435! THANK YOU to all the parents out there who gave their school and teachers a Christmas bonus. Teaching is sometimes a thankless job, so little gifts and appreciation goes a looooong way. Thank you. 🥰

- My employer had some additional contract work for me, so I earned an extra $750 in side income from December hustling. 👨🏻💻

- We signed up for the new Capital One Venture X credit card! This cost us $395 for the annual fee (but in a few months, we hope to reap ~$1200 in bonus travel credits!). 💳

- Gifts and presents set us back about $400 in December, money well spent! 🎁

- We also traveled to Boston for Christmas. Flights were paid for with points, and we stayed with family while there … so it only cost us about $300 for Ubers and groceries/booze! 🎄🍗🥂

(I love wrapping presents and choosing fun wrapping paper!)

Detailed Account Breakdowns

Cash Accounts (+$9,010): We’ve been beefing up our cash reserves but only because we plan to invest $12k into our Roth IRAs at the beginning of 2022. Our ideal cash balance is about $5-10k, as we want as much money invested and working for us as possible.

Rental Property + Reserve Account (+$1,148): All was quiet at the duplex last month (just the way we like it!) with no irregular maintenance or issues. Here is how the rental duplex made us money last month…

$1,975 — Incoming rent from units

(-$138) — Property management fees

(-$28) — Pest control regular service

(-$661) — Mortgage principal + interest

$1,148 — Total rental gain this month

Real Estate Syndication (no change): We’ve owned this building for 3 full quarters and are beating projections on all fronts. Our next quarterly investor distribution is set to come in January and is likely to be $800 – $1,000. Based on our $50k equity, this is a 7-8% annualized return.

IRA – Regular: (+$7,162): The stock market had an awesome run in December, and we finished with just over a ~3.5% increase. This IRA is invested in a total stock market index fund.

IRA – Roths: (+$3,426): Same as above, all our Roth money is invested in a total stock market index fund. This month we’ll be funding both our Roth accounts for 2022 with the maximum contributions ($6k +$6k) which will be reflected in next month’s report!

Joint Brokerage Account: (+$61,428): After the sale of our rental property, we moved $53k into this after-tax brokerage account. The additional growth came from rising stock prices. It’s kind of scary buying stocks in large quantities at all-time market highs… But I’m still convinced that lump sum investing is better than dollar cost averaging when you’re sitting on a large pile of cash and have a long investment time horizon.

*NEW* Solo Roth 401(k): (+$9,641): A couple months ago I opened a Solo 401k with TD Ameritrade, as well as a Roth 401k account. Since I have no work benefits currently (I’m paid as a contractor) I can host my own retirement plan. I decided to go with *Roth* 401k contributions instead of regular 401k because I can roll these directly into my Roth IRA later. This gives me a lot of flexibility with early withdrawals and such before I reach full retirement age. More to come on all this… I’m hoping to max out this Solo Roth 401k with 2022 contributions – this year’s max I believe is $20,500!

HSA: $4,743 (+$180): Since my wife and I don’t have HDHP health plans currently, we aren’t able to contribute to this HSA account. The $180 gain this month was from market growth only.

Breakdown of Liabilities

Rental Property Mortgage: (+$250): I’ve reached out to a mortgage broker to investigate refinance options (again) for our rental duplex. Since we have more than 50% equity in this property we have room to leverage a bit more. Still not convinced it makes sense right now, but it never hurts to explore options! Until then, our tenants are paying down the mortgage balance little by little, month by month.

Credit Card Balances: (+$4,856): We hammered the credit cards this month, but we have the cash to cover all purchases in our checking account. Each month we pay our CCs off in full before any interest hits.

My wife and I have no other consumer debts at this time. 😎

How did your 2021 finish up? Which accounts are you prioritizing this year?

Happy Friday and have a great weekend!

– Joel

Get blog posts automatically emailed to you!

I’m really liking the Capital One Venture X. The points post within days instead of having to wait until statement balance closes. The $300 travel credit and $200 Airbnb credit were easy to use and we got reimbursed within a week. We spent the money faster than projected (but still stayed in budget), so we applied for a second card for me (Dragon Gal got the first one). She referred me and we got an extra 25k bonus points about 10 days later. Only thing I worry about meeting the inital spend on the second card is if we have to cancel travel due to COVID. So trying to be cautious on how I use the card to pay for refundable travel.

I was worried about hitting the spend also… And my backup plan is to pay some property taxes (they charge a fee, but still less than the bonus points we get). You could also try the AMEX Platinum, which has a 6k min spend in 6 months.

My new job offers a Roth 401k, so I’ll be prioritizing that account. It will be nice to have another (potentially larger) pool of money that I can access without tax implications.

Amazing. And I believe when you eventually roll it all over to the Roth IRA, it is all treated as a “contribution” (original contributions + growth). So you can withdraw a larger amount earlier if needed.

Joel, does the Roth Solo 401(k) allow rollovers to your Roth IRA at anytime since it is self directed? Or, what are TD Ameritrade’s rules on this?

Since you are the plan owner, you can set your own rules. I believe by default, they allow 1 in-plan rollover per year. But, I think it’s in your best interest to just keep it all in the Roth 401k and roll it all over in a large chunk later in life. There is zero downside keeping it in the roth 401k vs. IRA, they are essentially the same thing.

Oooh, I want to know more about the self-directed Solo 401K. I only recently found out it’s available for sole proprietors, so I really want to get on that. Looking forward to that post!

Hey Katie! — Here’s the first post I wrote about it [Solo 401k w TD] and it has some stuff in there on why I chose TD instead of the other places… And another good resource was The College Investor which I also reference in the article. Feel free to hit me up via email if you want to chat further or have questions!!

You are killing it! That’s a huge net worth, especially for someone in their thirties. I’m curious, you said your normal target for cash is $5 to $10K. That sounds low for an emergency fund and even lower for an emergency fund plus working capital. I’m guessing you’re substituting something like credit cards with a high limit or a home equity line of credit in case of some major unplanned expense?

Hey Steve! Yep, we have multiple credit cards to cover unplanned expenses and a line of credit against our brokerage account. Planning for emergencies is important, but for the most part I no longer believe in cash emergency funds. (might completely screw myself one day, but that’s how we’re rolling right now)

Congrats Joel! Looking at your NW update just a few months ago, it’s shot up over $100k, which is incredible! I appreciated linking to the post on lump-sum investing is better than DCA for long-term time horizons, a well-needed reminder for those of us scratching our heads at how the market will perform for this year.

Hey Gary! I have no idea how the market will perform this year. But, since my horizon is 10+ years I really only care what the market does over 10+ years. And I’m confident we’ll see growth in the long term :)

Awesome post Joel and congrats on the big NW jump! I’m curious though, why weren’t you carrying the value of the property you sold in your net worth calcs prior to selling it? Did you make more than your appraised value? I carry a pretty agressive Zillow number for my units in my NW so if I sell I might even see a NW decline because I’m probably not accounting for closing costs adequately. I’m also impressed with your low cash position. I’m easing out of cash also having just purchased my $10k in I-Bonds which claim 7.12% return. I also just opened a public.com account and have bought a few individual stocks just for fun. Im prepared to lose all that and still be ok. Im a lot older than you though just turned 50.

Hey Jacob! I wasn’t actually tracking that particular property publicly — but now that it’s sold off I’m starting to track it all in these accounts. I have a couple private partnerships that we are keeping separate from public view.

I know what you mean though about zillow estimates and how you might be overvaluing places. Even my Duplex here I have valued at 250k in this NW report. But if I was to liquidate it after fees and commissions etc, I might have a 20k drop overall. It’s hard to know how to value property within NW reports… I guess as long as you realize transaction costs can set you back, just keep that in mind if you ever have liquidation plans.