[Today’s post is by a new blogger on the scene, AbandonedCubicle.com, who’s currently planning an early retirement by his mid-forties. He doesn’t have everything neatly planned out for his life “after the cube” yet, but he’s definitely had to learn a few things to get here. And today he shares some of these things, along with the hefty price tag he paid to acquire them ;) Enjoy!]

You’ve probably lost a huge sum of money before and not even known it. I know I have. It’s not a fun lesson to learn, and unfortunately you don’t catch it until a lot of the damage has been done.

In my case, it came in the form of opportunity cost. The things that you spend money on today that will end up costing you a lot more in the future. Even up to a million dollars more!

We live in a society that’s constantly marketing to us everywhere we turn, and our friends and neighbors only seem to raise the bar for us. We were once fine driving our old clunky cars, and then our pal Joe drives by in a shiny new Lexus and all of a sudden we feel the need to upgrade! And so it goes with all other areas of life as well…

Over the past 20 years, and up until recently, I was that guy keeping an eye on what Joe was driving. And what new appliances were rolling into his house, how many channels he was getting off that dish satellite on his roof, etc etc. I was on financial “autopilot” – happy to be putting in a measly 10% into my 401(k), figuring, like everyone else, I’d be working until 62 or older.

Perhaps the saddest case of my consumer epic fails occurred fifteen years ago when I went out and bought a $1,000 Tag Hauer watch after getting a nice raise at my multi-national company. It sure was pretty! I thought I was James Bond, or at least the IT geek version of James Bond!

The not-so-funny part was getting laid off just a few weeks later. I don’t think that ever happened to James Bond, did it? There were times when he handed over his famous license to kill after some silly misunderstandings, but me? I just handed over my server recovery cheat sheets and passwords (then rolled away in my vintage Lotus Esprit, of course…)

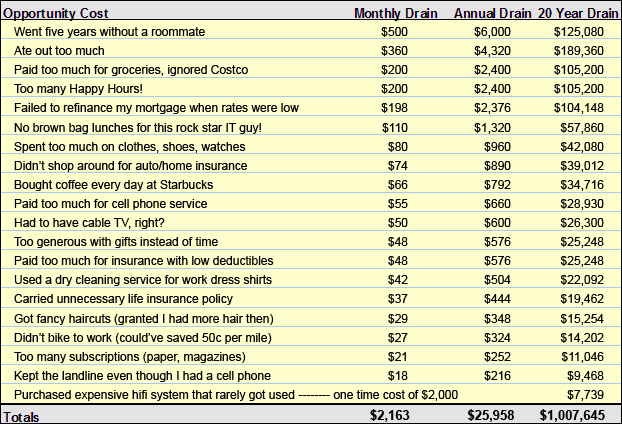

As for the rest of the lost million? Here it is, folks, in all its gory detail… The briefcase of cash thrown into Niagara Falls (to avoid capture by the Russians) which comprised of the following:

(The 20 Year Drain column totals assume that I’d instead put that money into

a low-cost S&P500 index fund, yielding 7% annual returns)

D’oh! That $1 million would have easily paved the way towards retirement in my early thirties, a full decade sooner than currently planned. With hindsight, though, comes a little bit of wisdom and an opportunity for redemption… And had I at least not stopped and evaluated when I did, I’d have gotten into my fifties, or even sixties, until I realized the path I was on!

Fortunately I stumbled upon Mr. Money Mustache’s blog in the middle of a particularly rough stretch of work (some project from hell if I recall) and I completely devoured it. Then felt pretty bruised and beaten from the righteous financial left-hooks.

Had I really been that careless with my finances? I thought I was doing everything by the book?

Turns out I was doing everything by the book, only the book according to Madison Avenue. That mustachioed wonder provided a turning point for me, and in entered the Frugal James Bond…

Much smarter than before (and having sold that silly Tag Hauer on eBay!), I’ve since taken the reverse approach of those first 20 years and as Mike Holmes would say, “Made it Right!”

Eliminating, or reducing, those opportunity costs is now the priority. Throw in some improved income from the day job, the marvelous wife’s business, and a few rental houses – and the Financial Spreadsheet of Doom from above starts to look a lot better.

The bottom line comes down to this: it’s never too late to adjust your spending habits and make changes that will guide you to a rewarding retirement.

The changes we had to make were not hard choices. That’s the sweetest part of all! We discovered that these expenses were in large part adding complications to our lives, and the simplifying of our budget led to better alternatives that not only saved us money, but quality time as well. It brought our focus back to what matters the most.

As for James Bond, well, I think he’d still be a pretty cool cat even with a Casio wristwatch (complete with hidden laser, of course.)

*******

Cubert AC blogs over at AbandonedCubicle.com, and lives in beautiful, but weather-wild, Minnesota, along with his wife and two kids. He writes about his personal journey leaving behind his corporate gig, and you can find him on Twitter @cubertAC.

EDITOR’S NOTE: Pretty frightening amounts to add up, eh? How much of that one million have YOU thrown away in the past 20 years? I can shamefully answer to at least $600,000 myself…

Get blog posts automatically emailed to you!

This reminds me of that great book “Your Money or Your Life” by Joe Dominguez and Vicki Robin. If you’ve never read it I highly recommend checking it out. Although the investing advice is a bit dated (investing in nothing but government bonds is not as comfortable a retirement as it used to be), the activities they have to evaluate how much money you’ve taken in over your lifetime, and how to evaluate spending on a shiny object against how much “life energy” you’ve given up to get it, are both eye opening. Good luck on your journey!

Great suggestion, Liz. I have read the book and agree 100% with the authors’ views on life energy / opportunity cost. It’s not the most engaging book, but one I’d also suggest for those on the path to early retirement.

True that it’s not the most engaging book – it can be quite dry at parts. I usually skim over them now :)

I’ve had that book sitting on my bookshelf for like a decade now haha… for some reason I love looking at it but have yet to read more than a few pages at a time. I guess cuz I already know what’s going to be in it from all the reviews and people talking about?

Yeah, it’s kind of like reading a novel where a friend’s already told you the ending, right? When you have time I’d definitely recommend at least skimming it. It’s a good framework for thinking about your spending choices in the context of how much time it takes to earn that money. Plus Joe Dominguez was able to retire from Wall Street after only a few years of work, making him one of the original FIRE evangelists.

Haha… in that case :)

Good post, Cubert. It’s never too late to learn about FI – there are plenty of good ideas in various blog posts in our FIRE community. Tag Hauer? Wow, I love their commercials but my financial left brain will kick my right brain’s ass (or curvy crevices?) if I even think of buying one.

Hey TFR! Avoid the Tag!!! Even if you did have 1,000 bucks to blow, the model I had purchased stopped keeping accurate time within two years. Q would not have been pleased…

Great article! I’m sure I’ve flushed a good deal more than $1 million down the proverbial toilet at this point, but at least now I’m on the right track.

Financial autopilot is a killer!

It’s crazy to think in terms like “a million dollars”, isn’t it? Even crazier to consider folks who blow through multiples of that and can’t or won’t adjust course.

I’ve done a lot of stupid. The wonderful thing is that we can learn from stupid and do a heck of a lot better as we rise from it all. Biggest doses of stupid tax for me was the biga** SUV in our late 20s because I had to show how successful we were, the wild spending on shoes (move over Mrs. Marcos) and too much fancy pants wining and dining. I’m happy to say we’ve done a major reversal and it’s amazing how quickly the $$$ accumulates now, even without factoring in compounding!

Well put, FTP. One thing that’s helped us is to try to recover some of that lost opportunity. You’ll never get back the purchase-price of the SUV or the gas money spent, but selling that thing used, and maybe starting a bike commuting habit will put you farther ahead in the race to retirement. I did manage to sell that silly watch on e-Bay for $350 – even with a five minute per day lag.

Been there, done that, bought the T-shirt. I commuted to work for over 5 years by foot/bike sans SUV once we gave our head a shake. Now, my commute is from the bedroom/kitchen to the home office though I still often travel to the the grocery store, coffee shop and library on foot. :)

Great post Cubert. Reminds me to stay focus on my financial goal. A million dollars is a lot in my country’s currency and I probably just doing the very thing down the path to loose the money if I’m not careful. Thank you.

Thanks, Dani! I thought I was being “careful”, but there’s an even better approach, to be “strategic”: use knowledge about compounding of dollars over many years and apply that knowledge with a scalpel to your budget. How sexy is that?!?! ;)

It’s amazing how those opportunity costs add up quick! Good to hear you have now made it right and are on the fast track to FI. Thanks for the post, Cubert, I look forward to checking out your blog!

It is amazing! I am by no means a role-model for super frugality, but the thing is, you don’t have to be super frugal to achieve early retirement. That’s the message I hope to get out on abandonedcubicle.com

Great post and I’m heading over to check out your blog too! I did pretty well in my youth but I’m sure I could have a few hundred thousand dollars more on my net worth now that I look at your chart. Another post to bookmark for my kids now that they are in college!

The trick for them is *getting them to care enough* to pay attention. Maybe send them a 6 pack and a list of blogs to check out haha… (Or tell them they don’t have to work a “real job” after college if they get their money on lock ;))

I sure hope I figure this out (getting them to care enough) before our two little ones venture off on their own. From what I’ve observed, they’ll care enough if their parents care enough. But man, so much pressure from peers and marketing to “keep up”!

Hurray for paradigm shifts! Aren’t we all glad that we have the ability to go through financial repentance and turn things around once we realize the true price of stuff? While we can’t go back and change the past we have full control of the future and now is the time to start making the most of that.

A-men to that, Bro! A lot of it is stuff we never had access to growing up (or dare I say, in the 70s???): Cable TV, cell phone data service, Netflix, fancy-casual restaurants, Starbucks, etc. etc. We’ve sort of embedded these added costs as “necessities”. It was easier “back in the day” to save, when you didn’t have as many luxuries to spend on in the first place.

Wow this post has really made it clear to me how lucky I was to get started on my FI path so early. I have no doubt I would have trod down the exact same path had I also not stumbled across MMM. Good for you on being willing to change! Good luck on the rest of your FI journey!

You’re gonna smash all of our net worths by the time you get to our age :)

Thanks, Gwen! Keep at it — and remember to have fun along the way.

Thankfully we were only blowing money without thought for a few years, but i bet we still wasted a few hundred thousand without including interest gains over time.

Whoop! Another MN blogger!

Right on, man. The way I see it, I could have easily lost a lot more than a million with some other extravagances thrown into the mix (e.g., not having a roommate at all the first several years after college, buying a way fancier car than a Saturn coup, and not saving anything in the 401K.) I suppose that’s why I’m inclined to write about this without kicking myself too hard in the arse. :)

Cheers to the MN blogging community!

Right on, “today is the first day of the rest of your life”. We too started out not so frugal and since have learned from those and numerous other financial mistakes. Chances are even at 35 I’ll still make other financial mistakes, though not this one. I think your process of mapping their long term impact out in a spreadsheet as a reminder is likely pretty effective at avoiding a repeat.

Spreadsheets and math are amazing tools. Just gotta know how to use them.

I’d hate to see how much I’ve thrown away over the years! Quite frankly I still could do quite a bit better than I am doing now. Will be checking out the blog!

Thanks, Mr. Defined! I agree with that thought. I still look at our “budget” and wonder where we could do better. We sure put a lot into dining out and vacations (even with this year’s haul of 250,000 bonus points.)

I’m glad you found your way out of the madness. It’s funny how a little financial meltdown has led all of us to the same place whether it be MMM, JD Roth, or J Money – all different styles but all the same message. Spend less than you earn and you will set yourself free. $1000 watch wasn’t so bad had you kept the job. Timing sucked!! ;) My 3 rental properties tanking brought me down the rabbit hole of debt but I’ve managed to recover.

Curious – how much did the Tag go for? :)

Ouch! Sorry to see that your rentals brought about a hole of debt. I’d be curious about how that went down. I’m glad you’ve recovered. Might be worth sharing some tips to help others (myself included) avoid serious rental hardships.

I got something like $350 for the slightly off, 13 year old Tag on eBay. Course, eBay takes a commission… One thing to be said about Tags, they hold their value pretty well.

Good luck on your FI journey. 20 years is a long time to spend wandering, but at least now you’re on the right path. Yeap, it’s never too late to start. Young people are so lucky because there are so much material on FIRE on the internet now. 20 years ago, nobody knows about FI.

Ain’t that the truth! Back in my day (Dana Carvey???) we had a few books, like the one J. Money has on his shelf collecting dust, “Your Money or Your Life.” I certainly had moments of inspiration before the blogs really blew up a few years ago. Some of the usual suspects I’d read during the 20 year stretch included “Rich Dad, Poor Dad”, and “Millionaire Next Door”. I had my chances, but not regrets!

As someone who excelled at spending money on stuff, I’m right there with you. I think I crunched the numbers and figured I spent about $11,000 on impulse purchases during my shopping heyday. That’s not planned purchases (of designer bags, designer shoes, etc). So, yeah. I’ve definitely squandered a lot. The money part makes me really sick, but the stuff part might actually make me even more anxious. I’m slowly getting rid of it (all?), and that’s the really painful part. But I try to remind myself that it’s not worth beating myself up over. I can only move forward.

You’re really buying FREEDOM from both mind and clutter at this point. So the cash on top of it is only gravy! :)

Agree with J.’s point as well. We work hard to be clutter free, and it really is gravy when you can sell the “sins of old” for cash on CL or eBay. Donations are great too – a lot of folks in need out there.

I lost my millions in a divorce! Not that we had tons but I have ended up paying for 90% of my children’s needs/wants/education :) I am proud that I was there for them and will continue. I have however changed my saving patterns now that they are on there own and doing well. I have about 14 years until retirement and I have know that it will come quickly. I want to enjoy my 50’s since I am healthy but I am also reading all the blogs about saving & cutting expenses. Thanks for all the information…..

Good for you!!!

Thanks….it is a great feeling coming to terms with financial freedom as a goal!

It’s great you gutted it out for your kids. Keep reading these great blogs, including Budgets Are Sexy. If nothing else, you’ll be inspired to share your own story in your own blog. I’m finding it a wonderful tool to keep myself accountable to the bigger goals we’ve set for our family.

I’m sure my wife and I have squandered at least a half million potential dollars, at least… but while some people get it at age 20 others take till they are 30 or 40. It really is about personal growth, that and now that you have this info what do you do with it? At the very least you need to pass it on to your kids. I’ve tried telling other adults most don’t seem to believe me or don’t think it is doable but every now and then it clicks for someone.

I feel like I was about 31-32 when I really got it (3 years ago). Since then I have made some progress but the one thing that is holding me back is this 600K dollar mortgage. Its tough living near DC, especially if you don’t want to live in a crap area, and especially on one income. I would like to stay here at least until my kids are out of school which will be about 18.5 years. probably closer to 23 when I think about college, Puts me at 55-56, then depending on a few things I may as well work at least part time till 59.5 so as to not tap into my retirement accounts. I’m not really planning on early retirement right now, I would have to seriously downsize to do so or make a significant amount more. I am confident however that retiring or semi-retiring in my 50s is extremely doable.

I can’t wait to get back out of the DC area… took me a few months back to remember it all, and now I’m ready to leave as soon as the wife says it’s time :) Unfortunately the best jobs for what she wants to do is here, so that is not making it easy, haha…

I feel you, I ask myself at least once every few months why I live here.

I remember you saying she is government. Tell her to keep an eye out for virtual job listings. IDK specifically what she does but many areas do have virtual. but then again her locality pay would be based on where you live. So potentially less money.

Yep, the mortgage is a tough one. I’m betting your property taxes are pretty high as well? From what I know it is hard to find a low-cost pocket in DC with good schools and low crime. Still, there may be creative ways to make it work in your current area: maybe by renting out a room or basement suite to collect some rental income? Easier said than done, but if you could pull it off, it’d probably accelerate your retirement age by 3-5 years or more?

This is a great analysis which everyone would benefit from doing. Nice post. To be honest, I’m a little scared about how much waste my analysis might reveal. . .

You might find it cathartic? I dunno… I did play by the rules and my splurges weren’t obscene. Still quite the eye-opener, and motivator to improve!

This is just a great example of how living normally is so ridiculously expensive! All of the things you did aren’t the type of things that anyone would criticize you for. Sure, you should live on your own. You’re an adult. Sure, you should go to the dry clean your shirts, or pay for haircuts (even if you don’t have a fancy haircut), or drive to work. These are all normal things to do and things that no one would bat an eye at.

The cost of inaction is also something we notice. I’m guilty of the same thing. I didn’t refinance my student loans for over a year, partly because I didn’t know I could and partly because I was just lazy. Biggest barrier to some of these things is just taking that first step.

For real – it’s all normal! And the scarier part is that people seem to be *fine* with it, either out of not knowing there’s a different way, or not willing to make the changes to make it different :( Although I surmise most are pretty stressed out and just not showing it/sharing it to the outside world… they don’t make for good Facbook posts ;)

Great point, FP. They don’t teach us in school to constantly monitor interest rates for opportunities to refinance. We learn the hard way usually, after college (yes, after 17+ years of formal education.)

PS – It’s easier to cut your own hair as you approach your 40s and there’s less of it to cut. My lovely wife/stylist will attest to that!

Hey, no judgment here. My fiance cuts my hair too! Really putting her dental skills to work there.

I can attest after meeting you in person that your (now wife) does a fine job with those haircuts! Course, hard to go wrong with the close crop. ;-)

It’s good to think about the long term consequences of any action, but looking at the cost of anything compounded over 20 years is going to be a big number. That could keep you from doing just about anything.

I think it’s important to evaluate how you spend you money and focus on the priorities. If that daily Starbucks brings you real joy (and you can’t make it on your own), go for it.

I agree with that, Fiscally Free. I think the main thing is hitting big stuff head-on. You know, avoiding spending big money on a big house, a fancy car, a fancy vacations year after year. If you can do that, then the little things like coffee and the daily newspaper are mere dents in the plan (and still, that’s a $45,000 dent after 20 years, which could pay for your kid’s tuition to State U. So there’s always a trade-off to keep in mind. Maybe you hit Starbucks once a week instead of five days a week, and you get your news off the web instead of print?)

Great post! And look how quickly the “little” things add up!

Our biggest loss came from larger expenses in the form of a bad car buying habit. Every 2 years, like clockwork, we’d trade in and finance our next car (or truck). Compounding what we lost would be excruciating, so I haven’t done it. But just looking at the chart tells me we lost more than a mil. :( I’m grateful we figured it out and are on a different path now (and I have to give MMM much of the credit too!).

Thanks, Amanda! Oh yes, that little car habit… I’ve had a few cars under payment plans over the years and it stinks. So nice to have both cars paid off now, and on liability-only insurance. I hope to sell the Fit when I hang up the corporate gig, forcing me to rely more on the Surly (and my feet!) to get around town.

Does your different path involve bike commuting by chance?

Very true. Those groceries are killer too, and shopping bulk is necessary at least once/couple months for my partner and I. I’ve never seen opportunity cost analyzed like this before…. don’t think small purchases add up? They do!

Man, those small purchases sure do add up. Another factor you could throw in is energy opportunity cost. Just take the savings you get from an LED-lit household vs. incandescent. Run those numbers over a 20 year span and you get some pretty nifty returns. Don’t forget to include the couple bucks a month you save by not keeping a silly cable box plugged in 24×7.

I’m sorry but I do NOT consider eating out, living alone, happy hour, and and drying cleaning (etc) as opportunity cost. Those things are worth the money to me.

It really boils down to what you value most, Michelle. Everyone has their own best mix of what works for him or her, and I’m certainly no exception. I admit I enjoyed the couple of years I didn’t have a roommate – a lot less drama and I didn’t have to share the washing machine! I have some amazing memories of happy hours with great friends and I have no regrets about that expense. This exercise is more a reminder that at some point in life, you can *choose* to downshift your major (and minor) expenses or not, and consider leaving behind a cubical job you may not love, or not…

Yikes! This hurts to look at! I feel like I am making or have made nearly all of these mistakes. Time to reign it in and get back on track! Some months I just don’t know where all the money goes, but looking at your spreadsheet, I think I have a pretty good idea…

It’s never too late, Bridget! I’m sure the Financial Gym has a great plan for you.

My recipe? Get friendly with spreadsheets. And start whipping up some plans to recover some dough with sales of “stuff” on CL/eBay, and boosting your income with side hustles (rentals) and A-player job performance. One step at a time.

Great article and reminder little purchases add up. I come from a frugal family, so I think frugality is in my blood. However, I still made some crazy purchases, and now that I think about, could have been funding my brokerage account. You live and learn. Glad I learned early (I’m 26). Now, it’s just reminding myself so I don’t try to keep up with the Joneses (it’s hard).

I’m trying to share with my younger brother as well. He’s 19.

Good luck getting through to little bro – Sharing the spreadsheet might be the wake-up call. “A million bucks from those things???”

Ouch! That really sucks about getting laid off; just adds insult to injury! I agree that living “by the book” is what gets people in the hole to begin with. Our society normalizes debt when it couldn’t be further from normal. “Good enough” just isn’t good enough for most people.

But it’s always possible to turn things around. :) It’s all about cutting every possible expense, paying off debt, and building your net worth for retirement.

Yeah, it really did stink when the lay-off occurred. But ultimately, I turned that situation into a positive by using the next 12 months to finish my MBA full-time. That then led to better career opportunities and pay. So when you say it’s all about cutting expenses and paying off debt, I’d just add that it’s also about maximizing your earning potential (day job, and side hustles) and opportunities as well. Cheers!

Wow!!! I never thought how quickly all that stuff adds up. I’m not sure I want to look at how much money I have wasted over the years. I might throw up in disgust with my old self. Thanks for sharing!!!

Think of it as therapy. Actually, a point I made in response to an earlier comment holds true. Some of the “lost opportunity cost” I wouldn’t trade for anything. There was some fun travel overseas that I didn’t mention in that list, and, some of those happy hours with friends made for great memories. I really think you need to enjoy life as it passes you by. That said, about 90% of the rest of that list is just plain silliness! :)

Absolutely love this post. Right now, my primary financial goal is to find all these costs in our spending to cut back. Once you start tracking expenses it can be mind blowing how much money is being “wasted” on things you don’t really need!

Thanks! I’m glad you love the post. Trust me, it’s hard to find the lighter side (Bond???) when you run these numbers. Definitely track your expenses, but avoid the trap of creating a budget. Counter to common belief, a “budget” is what gives us the green light to spend. Attack every line item expense with a scalpel. Be ruthless! (but don’t be too hard on yourself either!)

The timing of that lay-off was brutal. I’m glad you were able to re-sell that fancy watch.

Thanks! Yes, it was brutal, but in retrospect it couldn’t have happened at a better time. The market really tanked, so I turned my part time MBA into full-time and got it done. Much easier then, when I was single and kid-free. Gotta take advantage of the bad stuff – jujitsu style.

Money flushed down toilet: working with a commissioned investment broker that made me broker.

Money thrown out window: using my HELOC like an ATM machine for vacations and bar tabs

Money set on fire: buying my wife’s engagement ring with student loan dollars (still have the wife so that’s a bonus)

Oh wow – can’t say I’ve heard of that last one before!

Glad you’re still happily married, haha….

Don’t beat yourself up, Andy. Good to recognize the bad and then make the big changes to get back on track. I dropped a big chunk on my wife’s engagement ring, but have zero regrets about that. That’s why it’s not on the list. Hopefully your student loan interest rate is on the low side. If not, check into SoFi. Best!

How about : Paid more for a house then cold really afford resulting in over $3k a month interest only payments. 5 years of that with some refinancing to make it a little better. add $700 a month for taxes and $150 a month for insurance really added up! Getting rid of that place was the single best thing for my net worth.

Very smart, Richard. Refinancing is a great tool, if you know when to use it. Even better that you recognized that a larger house isn’t bringing you joy (but stress instead.) Home downsizing is perhaps the single biggest improvement you can make for improving your long-term financial picture.

Second to house downsizing, dump the knucklehead BMW or F150 and buy a Honda Fit or rely on a bike/mass transit mix. The long term financial gains, improved usability (hatchbacks rule!), and power over image (*no one* is impressed by your car) will yield huge results. Best in your journey!

This is probably the best post I’ve read all week. Opportunity cost is so incredibly sneaky. The most interesting thing to me about the list you put up there is that the top 5 account for more than half of the Money That Could Have Been. To me, that’s an inspiring thought because it means getting a few bigger things right moves the needle in a huge way and might allow for smaller indulgences.

The other interesting way to sort it is by level of discomfort. Too many subscriptions and unnecessary life insurance wouldn’t cause much pain to remove.

When I look at my own opportunity cost list, I’ve done pretty well with biting the bullet on big things, but I have a lot of low-discomfort smaller items that could easily be gotten rid of without having a material impact on my happiness.

Glad you enjoyed, JP! Always like seeing juicy guest posts come by my desk like this :) Especially relating to spreadsheets! Haha…

Thanks, JP! Life is full of choices. Some have long term consequences we don’t recognize until down the road. The beauty of cutting back is that you learn and adapt to a life that’s less focused on things and more focused on people and experiences.

Yeah opportunity costs stinks, and we all are guilty of this. I am eyeing a pair of sneakers that I want to buy soon as well, instead of investing the 100 bucks. I guess we all have the things that we enjoy shelling money for. As long as you invest or save more than that thing you cant live without, you should be headed in the right direction.

There’s def. a fine balance for sure, as you’re liable to drive yourself crazy if you think about the opportunity costs with every expense! I haven’t bought a pair of new shoes in at least 3 years so will also be going that route as you here shortly :)

In all honesty, I’m not sure I would’ve survived being single for many of those years where happy hours and dinners with friends keeps you “plugged in” to the social scene. Opportunity costs sure do stink! The key is to recognize them early on and try to find reasonable substitutes for costly pastimes.

The idea of applying the “gory detail” of the opportunity cost spreadsheet to my own situation has shocked me… I haven’t done it yet and I’m not sure I want to!

I was reading another blog post earlier today about cars and what a cash sinkhole they are (specifically new cars).

It’s so easy to get caught up in the trap of keeping up with the Joneses. My wife often tells me that so-and-so got a new car and that “they must be stinking rich”.

As I always tell her, never judge a book by the cover… people love credit and just because someone has a new fancy car, it doesn’t mean they aren’t on the verge of losing their home!

This is true! Haha…