I got a really interesting/confusing email the other day that initially through me for a loop. It was from my friend B. and went something like this:

“Hey Jay! Do you still do money coaching? I need some help getting my finances in order and thought maybe you get me back on track. Lemme know.”

Nothing too out of the blue, right? Plenty of people need help with their money or else blogs and coaching and, well, the entire financial industry wouldn’t be around. So at first glance everything’s normal here…

But here’s the kicker – the person who emailed me? He’s a PERSONAL FINANCE BLOGGER!! Someone who’s helped hundreds, and probably thousands, of people throughout his blog lifetime just like me. And who’s always given great, if not excellent, advice.

So why would my friend need ME to help him out? When he knows money just as well as I do? Well, after the shock wore off and I flat out asked him. And his answer was one I’m sure is familiar to all of us:

“I’m in one of those funks… I’ve got so much $hit going on in my life right now that I just can’t keep up. I literally need someone to look at my money, assess it, and then just tell me what to do with it. I need a plan.”

Wow, yup – understood! I was the same with investing. Took me forever to finally do something about my money scattered everywhere, until one day I literally asked a blogger friend what he’d do in my shoes, and then I did exactly that. Humans are notorious for dwelling on things forever and not taking action, so sometimes we just need an outside (trustworthy!) source to knock us straight and get us going again :) And for B., that was me.

So that’s takeaway #1 here: It doesn’t matter who you are, or what you do – everyone needs help with money. Some just hide it to themselves while other, smarter people (like B.) do something about it when they realize they’re stuck. So don’t ever think you’re alone in this money game – we’re all trying to figure it out!

Takeaway #2 is that we’re all in different phases with this stuff. And sometimes we repeat some of them when life gets in our way too. I’ve said this plenty of times on this blog before, but I can’t stress it enough. We have to do our best not to compare our situations with others because everyone’s in a different stage with money right now. Perhaps your peers in high school or college, or even 1st “real” job out of college are on a similar level, but even so we all have different goals and dreams, and some of us take longer for the $$ bulb to go off than others.

Hell, it took me 27 years to finally stop and pay attention to this stuff! So I’ve only been fiscally savvy for a good 7. That’s not a lot in the grand scheme of things. And throughout those 7 years I’ve gone from breaking even with money, to doing great, to freakin’ rolling in it, to breaking even again, and now to losing a little every month (though, more consciously than when I didn’t know what I was doing before).

Regardless of the stage you’re in right now, just remember it’s all temporary. Things will get better later, just as things may get worse. But if you’re eyes are open the whole time you’ll get through everything just fine :)

So what did we put together for my friend, B.?

Well, we hopped on the phone for 40 mins, talked about everything he wanted to accomplish over the next few years, and then formulated a plan specifically to that. And it was the plan, itself, that he needed most out of everything. It’s hard to reach your goals when you don’t have the schematics to get there, am I right Jack Bauer?

Here’s what B. wanted to accomplish, in order of priority:

- Pay off all his debt ($20,000)

- Build back up an emergency fund ($4,000)

- Start saving for a house

- Contribute to retirement again at some point

And then here’s some things about B. that’s helpful to know before reading the plan:

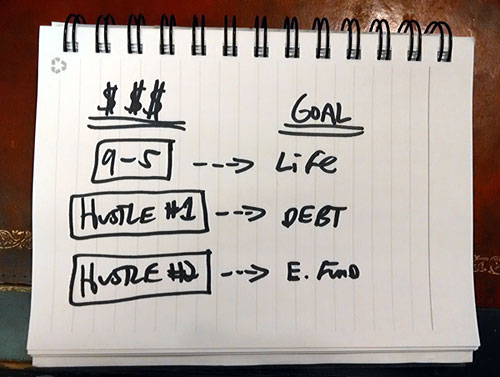

- B. has a 9-5 job that covers all his living expenses

- B. has a side hustle that brings in some decent money (personal finance blog)

- B. has another side hustle that brings in some money, but not as much as the blog

- B. is a “chunker” – someone who gets more motivated paying things off/saving in chunks of money vs tiddlywink amounts here and there

- B. will spend anything that’s “extra” in his accounts and usually not have anything to show for it

- B. is GREAT with money once he’s on a mission

(It’s also important to note that he recently went through some pretty big life changes… It doesn’t excuse a lot of the actions here, but it’s still something to keep in mind. We try to get the whole back story with coaching so we know if it’s a lifelong problem we’re dealing with or more of a one-off, but from knowing B. it seems to be more of a recent issue. So we leave it alone, do our best not to judge, and then get to work on setting things straight again.)

The Plan For B.’s Money…

Okay, so here’s the plan we set up for him… Loosely based on the Gigs For Goals concept we’ve blogged about before on assigning specific income streams to specific bills or goals you have.

Goal #1. Kill all debt

Since my friend has a main 9-5 which covers all his normal living expenses, he’s in the fortunate position where all side hustles are “extra.” And since we know he’s loosey goosey with his extra money, the first thing we needed to do was to assign each and every last dollar purpose. So we decide all income from his main hustle (pf blog) will be the gasoline to help light this debt bitch right on up and incinerated once and for all. He’ll be creating a new savings account to funnel all blog money to going forward (and aptly labeling it “Kill Debt!” to further stay motivated), and then at the end of every month he’ll apply the total balance directly against all debts. Nice and easy without any need to think about it again. (Outside of ordering which debts to pay first with the plan)

Why this will work: A) my friend doesn’t need any of this money to live off, b) it’s separated out (and labeled) from all other money keeping everything organized, c) the monthly chunks play towards my friend’s “chunker-ism” and d) it gives all this extra money a purpose so it’s not blown on nonsense. It’s all about structure when you’re trying to get your $hit together

Goal #2. Building back up the emergency fund

Similar to what we’re doing with his debt, we’ll do the same with his second goal here: channel all money from hustle #2 right towards one dedicated spot: cash savings. And again, since my friend has a 9-5 that covers all his normal expenses, we don’t have to worry about him going into further debt, at least in theory. So the e-fund doesn’t have to be top priority, where it might in situations of those living paycheck to paycheck. B. reckons he could have this fund built back up to the $4,000 level (from $0.00 right now) within 8-10 months. At which point we change the direction of hustle #2’s cash flow towards the next important goal on the list. Which, at this point, is the saving for a new house.

Why this will work: For the same reasons as goal #1 will – gives extra money a purpose and diverts into one spot specially allocated to receive it. And as we all know, if you don’t touch your savings the only way for it to go is UP. And up it will, each and every month so long as hustle #2 is in full effect (which he assures me it will). And the beauty of this goal is that it’s temporary.

Goal #3. Start saving for a house

Although this was item #3 on the priority list, once I found out about his employer’s 401(k) benefits, we quickly decided to move this to goal #4 on the list which will take over from the #2 goal above once the e-fund is complete. A 6-8 delay for now, but one we both agreed was smart since the opportunity here to jump start retirement again is incredibly good (as you’ll soon see).

Why this will work: Even though we’re not putting money towards this goal right now, there’s a plan for it in the not far off future, and in the meantime will give B. that much more motivation to make sure that e-fund gets filled. Unless he comes up with side hustle #3 and doesn’t want to wait ;)

Goal #4. Contribute to retirement again

This was the biggest shock of them all to me, and one I’m SUPER glad we caught. My good friend B. – which you’ll remember is a personal finance blogger! – was currently contributing a whopping 0% into his 401(k) retirement account. And what makes it worse/best now? His employer matches up to 6% of his income! Which means he invests 6% of his salary, and THEY invest an additional 6% of his salary – for free. Wow. You could have a 12% savings rate just by putting in 6% of your paycheck every two weeks. And that’s before it grows in the markets year after year too – pretty amazing stuff.

So, of course, this week he’ll be marching into HR and jacking up that % from 0 straight to 6. Will he notice the difference? Maybe. But nothing you couldn’t get used to too quickly. And since my friend admittedly blows any extra money, this will prevent him from having that much extra in the end. Worst case he can lower it later or throw less $$ towards debt if he wants to, but that all requires “work” and we all know once things are set in place we tend to get lazy and leave it be ;) So it’s smart to use that to your advantage especially in these cases.

Why this will work: The investments are automatic, it helps lesson any “extra” money to spend, and it in effect doubles his retirement income without lifting a finger. Putting 12% into retirement will be fine for a while so he can forget about it and know he’s doing well. Once his other goals are complete he can consider plopping in more as he’s still relatively young.

That’s the whole plan in a nutshell :) As you can see, he’s not in that bad of a situation all in all. Having more income than you need every month is a pretty fortunate position to be in, and of course gives you much more options than the reverse. It’ll take a few years for B. to get back on top again, but I have no doubt he’ll be able to do so if he sticks to the plan… (and we didn’t even go over any of his expenses on this first round – there could be room to speed things up there too!)

Here’s the takeaways from everything:

- Everyone goes through phases with money, even professionals

- It’s important we give all our dollars a purpose (try Gigs For Goals if you haven’t before!)

- It’s important we KNOW what our goals and dreams are so we can plan for them!

- It’s good to know how we work emotionally, as well as logically with money

- It’s important to admit when we have a problem (and to then ask for help)

- Side hustles can be game changers!!

Was I surprised that a fellow money blogger needed help with his money? Hell yeah I was. But do I now have mad respect for this guy for reaching out? You can bet your sweet home fries I do… It’s one thing to get yourself into a sucky situation like that, but a whole other to then spill your guts to someone you know. Especially a fellow financial blogger.

So I’m glad he gave me a ring, and I’m doubly glad he then allowed me to share this with y’all. I hope it gives you guys some good ideas, and at the least an appreciation of whatever your own situation is. We’re all in different stages with our money, but our end goals are always the same: Hit financial freedom sooner than later.

So keep pushing forward! You’re one step closer just being on a finance blog! :)

-J to the Hizzy

——–

[Photo cred: Barta IV]

Get blog posts automatically emailed to you!

Good post – and great spot about the pension fund! I always tell people you are turning away free money if you don’t max out your employers contribution to your pension.

Nice plan.

Its always good to discuss your own personal situation with other like minded people and experts. Often someone who comes in fresh will see something that you have missed or something that you have become overly focused on.

Sounds like great advice. Always good to bounce your ideas or get an opinion of another to make sure you own plan is solid.

Good catch on the 401K! Must take advantage of free money! This is one of the reasons why I like talking/reading/writing about personal finance so much–there’s always more to learn. I think it’s easy to get into ruts with how we spend/save and it’s incredible helpful to have an outside perspective.

Thanks for the timely article. Pretty cool that your friend realized he needed help and put ego aside and asked for your input. You should feel honored that he put trust in you. I have been in your position with RE…sometimes my advice is heeded….other times…not so much. IMHO it’s always good to get a “fresh set of eyes” on a situation. I might just be needing a set myself…

Yeah, I certainly have clients that don’t listen to my advice but it’s all good… the point is really to have an accountability partner and bounce ideas around until you find one you think works and then take action on. I also find people need to hear certain things a few time before it sinking in :)

This post really highlights the fact that you have to be careful who you’re taking advice from and who you’re getting help from (esp. in the blog world). Obviously, you share your earnings / net worth, so you’re someone who I would feel good about learning more from and possibly getting advice from. Everyone certainly needs help and it’s so great to have people to support you and guide you along the way. That said, I would be really struggling to write about finance if I didn’t take control of my own personal finances. It would be like going to a hair stylist who had really bad hair – I just wouldn’t do it! I’m reminded of T. Harv Eker’s book, “Secrets of the Millionaire Mind”, where he says to someone who wants to help him with his finances “send me your income reports first”. The point is – if you’re going to help me with money, I expect you to have your finances together. I’m glad you’re able to help in this situation – I can’t imagine a better feeling! I’m looking forward to that.

Haha yeah – it’s a good thing to consider for sure :) Although as long as the advice is actually *sound* (ie not false info or just stupid) then at least it can still be trusted… Of course it helps to respect/trust the person giving it too. Think about all those doctors who are super overweight and/or chain smoke – they probably give great advice even if they don’t practice it themselves. It’s an interesting one to think about. And in a perfect world yes – you typically want to take advice from those walking the walk :)

I was thinking the same thing, Natalie! =)

I certainly find value in the writings of the experts who have a long history of success with money, but I also find great value in the writings of those who have struggled and are turning things around – because that’s where I’m at. It’s comforting, for those of us who have made mistakes, to know that we’re not alone and to know that’s there is hope for change. I respect B. for reaching out for help, and I find myself wanting to know more about his story and wishing him the best in getting it all figured out.

Hopefully he’ll share it with all of us in the future so we can learn and be inspired! :)

I love your point that pretty much everyone needs help with money at some point. I know I have and, let’s face it, none of us are perfect and life or situations can really take us off track at times. Kudos to your friend for recognizing it and good on you for catching some of the things like the match. I LOVE the plan to match up different gigs for different goals. We do something similar and it really helps keep us motivated and on track because we know whatever that is it’s getting us one step closer to reaching that goal.

I applaud B for reaching out to you and I have seen enough to never assume someone’s financial situation. Like you said, even the best of us go through phases and need a kick in the butt. I have a few clients who have come up on their one year mark and in the back of my mind, I assumed they would not sign on for another year, because they are doing well. Every one has re-upped for more time because they have realized the value of someone keeping them on point.

Asking for help is not a sign of weakness but a sign of strength. That’s great that he reached out to you for help and I wish him the best of luck! BTW can you help with people earning more if they are freelancing? I was working with someone but they were’t sure how to help me because I was great with my expenses but not so great with my income. But what do you do when you are busting your butt to change that? :)

Interesting one! Is it more of a problem getting clients, or getting paid more $$$? Cuz there are tons of ways to try nabbing more clients, but not sure about how to get more $$ depending on what it is… I know with freelance writing it’s all about emailing and networking your ass off to land the deals. And then slowly increasing the $$ and swapping out the old crappier gigs for new ones over time until you hit the perfect ratio w/ clients to $$. And then of course the more open you are to taking on side hustles that are different the more chances of making more $$ too. So it all depends on what you’re willing to do and/or want to do that determines amount of $$ to make :) Happy to try and help one day if you want to give it a shot.

I’m still trying to focus more on video editing that writing, so it would be both more clients & paying more. For instance I had a great lead on a client that was close to where I live and I think had a good budget AND really did need people. But man I tried every which way after they initially emailed me saying they loved my work to land the deal. Calling, emailing, suggesting days/times to meet. I feel like there has been so much of that over the last couple of months. So how are other people landing gigs and I’m always in limbo land. Anyway, that kind of stuff. I could probably pick up a million little $3–$40 writing assignment, but they take out so much of your time then it’s hard to focus on what I call the “big rocks,” bigger jobs that pay more so not every once of your free time it just trying to make a buck or two. Know what I mean? :)

Oh and affiliate coaching. I’d like to know how to better utilize using affiliates for more passive income. No one seems to coach specifically for that.

I think in instances like that w/ that guy he already went with someone else on his project (or decided to table the project) and that’s why none of your reaching out is helping. When someone wants something – or someone – they’re usually pretty quick to get things going…

As for the bigger rocks, I hear ya – that’s def. ideal! I guess the only problem with that is not working on anything while waiting for those big ones to deal. So I feel like it’s a combination until you’re desired enough to only be landing the big boys… But honestly I don’t know jack about the video editing world ;) Just with business/freelancing in general.

As for affiliate stuff, yeah, it’s def. a GREAT way to make some $$ if done right (and if you have a large audience or a super targeted one). I find there’s a balance bloggers have to strike on that stuff as you can tell pretty fast which blogs are just trying to make $$$ without much care of their audience, and those who actually do care… Not that one is completely wrong vs another, just comes down to goals and vision for our sites. So I’m a big fan of affiliates for products/services you already love and use which are much more organic than, say, hawking some credit card just for sign up $$ that you could care less about. Unless you’re only it for the money (which I know you’re not cuz I know you :)).

Anyways, just don’t stop pushing and hustling over there. All this stuff takes time, and many times more than we’d like!

Knowing when to ask for help is a sign of a true expert!

I don’t consider myself an expert, but I feel the same way sometimes–it would be nice having another pair of eyes to look things over and help make decisions instead of trying to do it all myself with all the other crazy things I have going on. There are certain things that are just second nature by now, but there is plenty that I still need to learn. A fresh pair of eyes is almost always a good thing.

No matter how much of an expert you are, looking at your own situations can get tricky and complicated- whether it’s money, fitness, love, whatever. Having the outside, objective perspective is so helpful if you’re willing to be open to it.

I also have mad respect for B putting his financial health first and reaching out for help. Just because we are PF bloggers doesn’t mean that we have all the answers. Sometimes we do need outside help to find ways to get us to our goals sooner and with greater focus. It’s good that you helped him to redirect the extra income to specific goals and definitely a good catch on the 401(k) situation!

I’ve also been kicking around the idea of working with a financial coach or financial planner to incrementally improve our results, take action on things that I’ve procrastinated on forever (e.g. – a will), and generally just learn more. It’s good to hear I’m not alone!

You should! I’d imagine that just one session with a Financial Planner could probably help a lot – even to just get questions answered and generally pointed in the right direction. And being a blogger online you have access to many who also do this type of stuff as a “real” job :) Not me though, haha… I stay far far away from will helping and the likes. I have trouble with ours as well!

Hey J$,

Long-time reader, first time poster. This article really got my thinking and kinda-ticked off to be honest

Really…how can you buddy be a finance blogger and “expert” as you call him/her if they are an avid money-spender, was completely clueless about there 401k match, and in $20,000 of debt???

I admire you because at least you “practice what you preach.” How can “we” as the public take advice from someone who has no idea how to budget and prioritize his/her finances. Think we need a little more information to find out what kinda of debt the $20,000 was. Was it credit card debt (if so, then WE really need to not consider this person an expert), student loan, medical, etc?

I understand we can all get into trouble sometimes but I think we need to really think about who are the so-called experts. My money plan for your friend would:

A) Re-budget and prioritize (where is the money going..ie. going out with friends, extra starbucks machiattos, golf on the weekend with the buddies)

B) Through in all extra-income at debt (Agree)

C) Build up emergency fund (is $4000 really enough, sounds like if they lost there job they would really be in trouble. What are there monthly expenses vs monthly income (Agree)

D) Would re-start with their monthly match (would up their contribution so it reaches the maximum limit for next year (2015) of $18,000 so they are used to having that money come out of their paycheck.

E) I would certainly have this person think about whether or not home-ownership is in the cards. I would recommend that anything extra go into the “down-payment” account. I think $20% down payment should be the goal but I know that sometimes is unreasonable depending on the total cost of home, but honestly, I don’t think it would make a lot of sense without 20% down because of the PMI (which we all know really stinks).

Thanks for sharing J$ I hope this person plans to share they’re money “issues” with their reader-base for full transparency! I think we need to know what kind of expert we’re really talking to!

I may be off base, but I know that many PF bloggers get into the bloggin’ thang in order to motivate themselves. It would be like a chronically overweight person becoming a personal trainer at a gym. They need to live in it in order to keep on track.

Perhaps this guy is one of those bloggers. Sometimes you can get off base little by little and then all of the sudden you realize you need even more help.

I too hope that he shares his struggles with his readers. It’s very difficult to admit failure but the strength you receive from a community if you are willing to share your trials is amazing.

Sincerely;

Mrs. Wondrously Weird

Blogger of finance because I was born with a weird frugal bone so I also sometimes don’t understand those who don’t naturally get it but also born with several sweet teeth so I totally get the overweight deal.

How’s that for a title. : P

I thought the same thing as I started going through the article, as well. I get the “do as I say, not as I do” standpoint, but I guess that this article really illustrates why the transparency that you provide your bloggers is so important. Even though I don’t agree with all of your decisions, you provide, not only the numbers, but your reasoning behind your decisions. There is not a strict “right versus wrong” with a lot of decisions…but this other “expert” was making HUGE mistakes. Not taking advantage of the 401k match is Finance 101. Tony brings up good points…but I still go for the match before debt because the return is likely greater. A 100% return on the match (plus potential market return) is better than the ~15-25% loss on debt (assuming horrible APR’s). I also assume risk on the emergency fund. I can’t stomach losing interest on a pile of money, so my emergency fund is my Roth IRA contributions. In a true emergency, I take money out of there. That way, “new tires” doesn’t become an emergency…it gets narrowed down to “health and job loss issues.” My cash reserves are usually two months of expenses with an eye on big upcoming purchases.

In fairness to Mrs. WW, I think that we can assume that we have “Personal Finance Bloggers” and “Personal Finance Bloggers that are experts.” I just think it’s important that the bloggers are clear on which one they are beyond the typical disclaimers that are included for legal purposes.

Great comments guys!!! Love seeing these!!

A few things in response to all y’all:

RE: Debt details — yes, I left out the specifics on purpose just so I wouldn’t accidentally “out” this blogger. He’s told me he’ll probably divulge it all later to his audience, but for now he’s still dealing with all his life events and wants to get settled first… which I can respect. It’s hard enough to share problems like this with people, but even harder when you don’t have a grasp on it yet yourself. So for now I’ll have to leave it vague like that…

RE: The *types* of bloggers — yup! All different types. Some are in heaps of $$ trouble and blogging their story while getting out from under it (debt bloggers usually), while others are just pure informational types who share tips and tricks but don’t share their personal details, and then you have the ones who are killing it and divulging everything. All I’ll say for B. is that I know he’s typically great with money and these life events have kinda messed things up a bit… Similar to what I mentioned above in a comment, it’s kinda like one of those things where the information someone tells can still be accurate even if the person isn’t following them himself. So it’s really up to the individual to decide if they should trust their opinions or not… And obviously I’m skewed having already been friends with B. ;)

RE: The “Expert” Term — I kinda hate labeling B. or any other personal finance blogger an “expert” per se, but I couldn’t find another word that best describes it…

“Person who knows a ton about money” was a bit too lengthy ;)

@TONY – Thanks for commenting for the first time – way to add to the convo!

That’s great that you were able to help your friend fix up his money plan! It’s a nice example of the fact that even though you can fall off and get entrenched that it’s possible to get back in the game. Would love to know how he’s doing as the plan progresses.

I admire him for reaching out and letting the world take a shot at his financial weaknesses. I think we get stuck in ruts and need a wake up call sometimes to put into practice what we probably already know.

This doesn’t surprise me at all. Doctors see other doctors for medical help. Lawyers often consult with other lawyers for different angles. Sometimes simply having an outsider look at your situation and give you an unbiased opinion helps to cut through the BS and truthfully show you what you how to get through it.

Nice analysis and plan you guys laid out!

Exactly…. that’s actually similar to what he told me too after we emailed a little back and forth – we all need a trusted set of eyes to review our situation regardless of how well (or not) we’re doing. And even more so from someone in the same field since we typically give ourselves blinders!

You are so right! Everyone needs help from time to time. Glad to know all the “expert” PF bloggers out there are not immune to needing some financial advice at times. Whew!

Yeah, we all need a little help sometime. Life is just so hectic and things slip through the crack. It is difficult to look at your finance with an objective eye.

That’s wonderful that a fellow personal finance blogger reached out and asked for help. it is a great strength to know your weakness and request assistance when needed. And it’s great to have a fresh set of eyes to look at the whole picture and see everything from a different perspective.

Sometimes we’re too close to a problem (or have stared at it too long) to see the solution that’s there. I’m glad he didn’t let his experience get in the way if asking you for help. I can see how it could have been difficult for him to admit he didn’t have all the answers, but none of us do. I like the gigs for goals method!

I tend to get in a rut and just keep doing the same things over and over and consider what I am doing to be the best possible scenario. Sometimes it’s good to have an independent person take a look at things and just ask a few questions or throw out a few ideas.

I have gone to a few financial planners for the initial consultation and lay out the numbers and most say “wow, so what do you need me for?” and I say, well what would you do. I’ve had a few say to just stay the course, a few that want all my money and to sell me a couple of finance products they get commissions on and then a few others that say, “have you thought about this or this.”

If I never talked to anyone or got another opinion I would still be living in ignorant financial bliss thinking that 3% savings and 3% match would somehow be the answer my financial and retirement situation. One meeting for 1 hour changed my financial life forever 6 years ago.

Perfect testimonial for all this! And you’re right – even getting a “stay the course” helps to keep you going and more confident in the plan. Great comment, my man.

Sometimes it just helps to have someone else look at your finances. Just knowing someone else is looking at your dirty laundry makes you want to clean it!

This is just to say +1 for the Jack Bauer schematics reference :)

Haha… Glad you enjoyed that little ditty ;)

It was always annoying though that Jack always needed ’em like in 30 seconds and the other person (usually Chloe) would say “It’s just not possible! I need at least 30 minutes” and then magically – EVERY DAMN TIME – Jack would have them within the 30 seconds he needed ’em by. Too unbelievable! Everything else on the show – believable ;)

Major kudos to B for reaching out to you! Thank goodness you got him back on track with the 401k thing. I’m also a little concerned that $4k might not be enough in an e-fund, depending on his expenses of course. Even though he has a 9 to 5, that does not necessarily insulate him from job loss or layoffs! Glad you could get him back on track.

Agreed actually. I always like to ask the person what *they* think would make them the most comfortable, and then try and reach that first. Afterwards (which I haven’t had any clients that long yet) the plan will be to review and see what they *actually* might need at that given point in time… But by asking what they would like to see in there during phase I, I find makes them a lot comfortable and not as scarred off. If I say we’re going for $10k off the bat it’s a hard pill to swallow :)

Reaching out for help really does take some courage sometimes, so good on him for doing it. I feel like whenever I seek help, its often not so much the advice that helps, but the fact that you’ve opened yourself up – it’s like it acts as a trigger to confront the issue, take some action and do something about it.

I’m always super impressed by all the bloggers who share their personal financial situations with the world, but it seems to be such a great way to keep you on track, when you know someone is paying attention, regardless of whether people offer advice.

For sure. Even when I only had like 7 people reading my blog it made me double think my actions in real life knowing I had to report back to them later! Haha… It’s a total win-win :)

I finally caved and let Mr. Mt buy the shiny toy he has wanted the last 8 years. As we were driving home all I could think was, “Crap, now how am I going to explain this on the blog?!” =)

Haha… sounds about right :)

That’s great you didn’t really judge too much, as many PF bloggers might need more help than it seems. Also have you ever heard how stock brokers, are broker, than the clients. They make big incomes, but risk it all, and lose a lot. They don’t save and live paycheck to paycheck. Its a do as I say, and not as I do type of thing with some brokers. Sign them up J. as your new clients. I can be your partner.

Hah – sure, you go recruit and I’ll do the coaching ;)

This exact post is the reason I believe that financial advisors still hold value in today’s world with robo-advisors and passive indexes becoming more popular.

It’s always nice to get another opinion! And sometimes, I think PF bloggers are maybe more messed up when it comes to money than most. That’s why we need to write about it and get all the aggression out. Or maybe I’m just talking about myself….haha.

Haha… I’m sure there’s truth to that! And a perfect way to hold yourself accountable too, as others have mentioned up above :)

That person who emailed you is very truthful to himself, even though he is an expert. I hope everyone is like him who is not afraid to ask help from someone. He really know himself and what he needs.

I applaud him for asking for help. Everyone needs help from time to time. I don’t consider myself an expert and wish I could afford your coaching services! I am putting mostly everything to debt and go back and forth with saving for retirement and investing as well. It’s a tough balance and I’m never sure of what the “right” thing is.

That’s because there is no “right” thing :) Statistically there may be one, but most people don’t live their lives based on numbers as our feelings tend to creep in. So my opinion has always been to just “do what feels right” and then as time changes, and different life events occur, adjust and keep asking yourself “what feels right right now?” You can never go wrong paying off debt or saving/investing as either route grows your net worth.

Nice to hear that even experts need advice sometimes! I think having someone external assess your financial outlook is good as it takes out all the emotional part of planning and decision making..

I think it great when we see the real side of money – that even though you know about it and even write about it, it doesn’t mean you’re perfect with yours. My friends tend to think I’ve got it all figured out because I blog about my net worth, but in reality I’m still struggling to get my sh*t together!

Things are significantly harder to do for yourself than for others. You can look at someone else’s budget without bias or being invested (so to speak) in the expenses. To the person him/herself, there are nuances or emotional ties. So a third-party perspective can be integral.

Does your friends 401(k) have a ‘true up’. Some firms will match your 401(k) based on your payments for the entire year – not just based on what was contributed each paycheck.

Primarily this is for people who max out their legal contribution early in the year (so can’t contribute say for Nov/Dec), they will still get a match for that period.

Seems like your friend could contribute the maximum for the rest of the year (my employee limits it to 50% – up to the legal annual limit) and maximize his match for 2014.

Great point! I did not ask, but you’re right – that could certainly skew things. Probably too hardcore for someone trying to get back on track, but not others who could be reading this. So thanks for sharing it :) Reminds me of when my company would match in that way so I’d turn up the heat to 90% of my paycheck going to my 401(k) until it maxed out and then had the entire year of plumper paychecks :) Which I couldn’t have done without having side $$ coming in (and making it even more motivational was that my employer matched 100% of 100% you put in – which was unheard of!).

It takes major guts to swallow your pride and ask for help…and that goes doubly when it’s an area you’re supposed to be great at. I give this guy a lot of credit for stepping up and taking action.

Knowing and doing are just not the same thing.

Great food for thought.

This was a good read. I think my big takeaway is to figure out exactly what I want to achieve with my side gig and go from there. Thanks for the inspiration.