Up until today, it was 1 year and 10 months for me.

But then I logged into USAA as I usually do most mornings (a habit any true $$ nerd would enjoy), and I was met out of the blue with this:

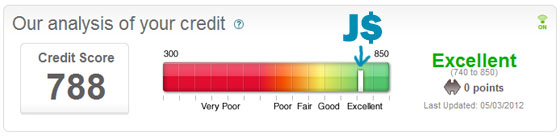

Woah!!! A free credit score just for me??? Is mine really 821?? Who? What? Where? When?

(If you’re wondering – yes, we do have a balance on our c/c because we throw all our expenses on it to rack up cash back rewards as well as to make budgeting much easier. Which of course we pay off in full every month. You’ll also notice a $25,000 credit line too even though we’d never use it in a million years. That’s to jack up our debt-to-credit ratio to help pump up that score more! Which looks like is working! :) But only smart to do if you trust yourself enough not to max it all out.)

So I Googled… and came across this from The Washington Post dated Jan 13th of this year:

Ahead of its competitors, Discover rolled out free FICO scores on the monthly statements of millions of its card members… But there is nothing like peer pressure.

This week, President Obama, in a speech at the Federal Trade Commission about privacy and how to better protect consumers from identity theft, gave a shout-out to several lenders — JPMorgan Chase, Bank of America, USAA, the State Employees’ Credit Union, Ally Financial — for deciding to also offer free credit scores to their customers.

The article went on to say,

“USAA said it will fully implement its free credit score program to credit card holders by March and will provide the Experian VantageScore.”

And it is March now, isn’t it? Woo! I tip my hat to you, USAA. Not that it really surprises me much considering I’m obsessed with ya’ll and have over 10 accounts with you, but still – classy move no less.

Who cares about USAA though – what does this mean for you?

Well, that hopefully you can easily get YOUR credit score for free too just by logging on to your bank or credit card account too. See if you can find it! :) If you can’t, or you use an institution outside of that list above, odds are you’ll probably start seeing it soon as everyone tries staying competitive…

How else to get your free credit score

Other places you can grab your free credit score is at Credit Sesame, Credit Karma or Quizzle. Though the only one I’ve used personally up until this point is Credit Sesame. Which gave me the following score those 22 months ago:

And the time I pulled it before that it was 791. Which I only know because I was in a heated battle with my wife to see who would win :) (Can you guess who came out victorious?)

And the time I pulled it before that it was 791. Which I only know because I was in a heated battle with my wife to see who would win :) (Can you guess who came out victorious?)

Now all these places spit out different types of scores (there’s like a billion of them), but the point is to get a good measure of where you stand on the range so you can then start working on improving it. Similar to tracking your net worth or early retirement scenario. We’ll all track it a bit differently, but if we stick to one it’ll be easier to compare how we’re doing. And it’s not the end of the world to mix them up from time to time either just to see what the differences are…

FYI – the score Credit Sesame gives you is an Experian one and the score USAA just gave me is the Experian VantageScore – which is different in that it combines the scores of all 3 main credit bureaus (Equifax, Experian, and TransUnion). And then of course there’s the grandaddy of them all – the FICO Score. Again, tons of scores out there but the point is to know where you generally stand and see if you can continue improving upon it.

UPDATE: I totally forgot I ran my score last year too – oops. Which I paid for through Experian while in there running my credit report (apparently I’m not loyal to anyone ;)). Here’s what that one showed:

So why do you want a good credit score?

Three reasons:

- The higher your score the less $$$ you pay when you take out a loan

- The higher your score the less interest rate you pay on your credit card(s)

- The higher your score the more attractive you’ll be when dating ;) (TRUTH: there’s a dating site based on credit scores!!)

Why you might not care about your credit score:

- You never plan to take on debt again

There’s a whole gaggle of people who actually don’t believe in credit scores and go about their lives without them. They rent apartments, buy cars, and say they even purchase homes without a credit score. I used to call shenanigans on that, and then it turned out an old blogging bud of mine (Brad Chaffee – if anyone remembers him? From Enemy of Debt?) was such a person. And claimed he had a credit score of zero, which I really laughed at and didn’t believe (turns out that’s kinda sorta true too, but also not).

Anyways, whether you care for them or not, it’s probably in your best interest to at least *know* where you stand and make sure nothing wonky is going on without your knowledge.

Which is where (free) credit reports come in…

Not to be confused with credit *scores*, your credit report gives you information about your credit history. And can be dozens and dozens of pages long depending on how active and old you are (and also available to employers FYI – which is another reason you want to know what’s on there). The last time I pulled mine it was 28 pages long! Which of course is much different than your score which is 3 NUMBERS long ;)

So where can you get your credit report for free? AnnualCreditReport.com. The only (non-shady) place that’s literally mandated by federal law to provide such a report to you every single year, free of charge. In fact, as soon as I post this I’ll be running mine again as well since it’s been a year (I tend to stick with Experian’s report in there though you get access to all 3 bureaus’ reporting).

Your challenge for today!

So your challenge for today is to run both your credit score and your credit report if you haven’t done so in a while. To get your free score log onto your own financial institution to see if you can get it there now, and if not hit up Credit Sesame or any of those others out there or just pay for it after running your report which comes next.

Then 5 seconds later grab your report from AnnualCreditReport.com and staple everything together so you can review later in the week. The second part of your homework assignment ;) I’m not gonna lie and say it’ll be quick, or fun for that matter, but it’s definitely a smart move to make. And much more productive than seeing what your “friends” are doing on Facebook!!

Once you have ’em, tell me what your score is! And see if you beat my current 821 :) Or if you’d rather not, try out some of these made-up but equally awesome calculations instead:

This should keep you occupied for the rest of the work day :)

———

Photo by andymag

Get blog posts automatically emailed to you!

I’m one of those people that have been getting my free credit score for some time through Discover Card. It’s a really nice feature – I’m in the 800’s bro!

Nice! Good on Discover for leading the pack here.

That’s a pretty sweet score you’ve got there, J! We typically check ours but once a year, however, now that you’ve assigned it as homework I’ll have to investigate so as not to feel like a $$$ slacker… ;)

Peer pressure!!!

something i’ve seen recommended is to get your credit REPORT from annualcreditreport.com once every 4 months from each of the 3 bureaus — march, july, november for example. This way you get to see the information more often, less likely to forget, and also catch any errors and correct them since credit scores can take some time to change.

I think if you were Mr. Perfect that would be a smart thing to do, yes :)

Nice I’m in the high 700s. Weaknesses are short credit history. Churning cards for miles has actually helped a lot though by increasing my available credit.

I don’t know who you c/c churners do it – makes my head hurt! :)

Nice! I’m in the same boat.. Average card history is around 2 1/2 years, so churning through wouldn’t necessarily help – though the miles are so beautiful. I keep utilization around a nice 9%. #humblebrag

I got my credit score for the first time back in the Fall, and it was about 740, I think. Not too bad for someone with the debt load I’ve had over the past few years, and the new credit I had opened to move stuff around. I think by this Fall, when I check again, it should be even higher.

yeah, that’s great!!

I checked my score 1 hour before opening the email asking. I’m trying to better my score in order to buy a house so I check it every Monday morning and I have challenged myself to continue to work towards a higher score and better looking report from now on out. It’s a game I like playing since I enjoy math and number problems.

That’s a GREAT idea!! And you’ll have to swap it out with a new fun $$ habit once you buy that house to keep up financial sexiness :)

I’m in the mid-700s. Pretty short credit history plus a lot of churning.

Still pretty good!

PS you win, but I’ve gained almost 100 points in the past 3 months as an average. Now I’m just working on the other pieces of my financial framework for house buying preparation while trying to raise my score and put myself in a better position to buy s house for my family.

Hi, J – thanks for the great tip! I have Barclays Bank and they also give you your credit score. I don’t recall getting notice that they were going to put it out there but you got me wondering so I checked. WooHoo! 825+

Brilliant!

I have checked my recently. I wanted to see where it was at post debt pay off. It was over 800. Also checked in on credit report to make sure all was in order and it was.

Nice! It’s a bitch when things are wrong on that report…

I too get my free score through Discover. It’s great to have it on the statement and not have to shell out the $30 when I need to check it before making a big purchase. Right now I am in the low-800’s and it varies by 5-10 points a month.

Damn good place to be in, sir.

One credit card gives us our score on the statement. 848! WooHoo!

Wow, I think 850 is the highest the range goes! This is the highest score I’ve ever heard of someone having!

Yeah for real!!! Way to go!! (And for your c/c company to print it off like that too!)

Awesome score J$, both my wife and I are usually hovering around the 790-810 mark ourselves and we get our 3 reports throughout the year to stay on top of those. I need to stay on top of it myself as I’ve had stuff from my Dad show up on my report several times over the past few years. That said, where did you see your score on the USAA site? I looked for mine, and looked on my credit card section of the site and didn’t see it.

You’re the 2nd person to ask me about that :( I found it when I logged into my c/c section there on the right side column. Maybe they’re staggering the roll out? Or they picked mine in hopes I’d see and then blog about it??? Haha… (if ONLY I was that important! ;)).

If it’s not there again when you go back, I’d check every week and I’m sure it’ll appear at some point. It’s really cool!!

I’m beginning to think you ARE that important! ;-)

I’ve checked my USAA account every day since this post and I’m still waiting for my score to show up. Interesting…

That’s awesome. I love Credit Karma, but had no idea Ally offered free credit scores too. I just logged on and haven’t managed to find it yet (not the best navigation system, Ally), but I’m excited to compete them when I do.

Ha! I remember when my post last year drove you to check your score and I was shocked that you didn’t check it more regularly. I love that credit card companies are now offering credit scores to their clients as a courtesy for having a relationship with them. The companies have our information anyway, so it seems natural that they should share. I am curious, though, how this practice is going to impact sites like Credit Karma or Credit Sesame.

Apparently I only check it when I want to know if I’m sexy ;)

Nice! I just checked my credit score the other day and it went up a lot! Yay! But I haven’t done my credit report yet. Just trying to get through freelance taxes right now!

Running your report can be your reward afterwards – hah!

I get free credit scores on Mint, too. They give you a pretty good report to tell you why your score is high or low, too. 807 today! I was dinged by not having a lot of open accounts and for the average age being young. My oldest account hasn’t been used in a decade, or so. I kept it just for helping the credit score.

Oh nice! Great to know about Mint!

You beat me by 7 points!! Not too shabby! Thanks for the challenge. My husband and I were just discussing our credit scores the other day but never got around the checking them! The funny thing is that we were discussing this because a friend of ours is hoping to get her score back to zero! What a weird concept, but she had some pretty sound reasoning.

Haha… I don’t think it’s possible to actually have “0” but you can have a really LOW score or no score at all (if you have no credit history and such). But always fascinating to hear peoples’ perspectives on this for sure :)

Ha! yes! I meant she wanted to have zero credit history/no credit score at all. Its crazy! Not my thing, but awesome that she is so dedicated!

I checked my credit score for the first time just last week. I finally decided to start caring. The Dave Ramsey route (which I’ve been doing, more or less) can work but it’s definitely comes with its set of inconveniences.

The first time ever?? Really??? Next you’re going to tell me you just found out what a budget is? ;)

Checking my credit score is one of those things I know I should do annually but I always seem to “forget” to do it. I better look into this.

My credit sesame score shows about 760, but when I got my FICO score pulled by a lender the other day is was only like 730, that’s a pretty big difference! I know the credit sesame score is different from the one lender’s use, but I thought it would be closer than that!

Sounds about right from what I hear… I think if it was 40-50 difference something would be awry? Prob good to Google though :)

High 700s here. Had been over 800 but have racked up some debt in recent months doing home repairs.

Those are the worst :(

I haven’t logged into USAA in so long, but yep there it is!

I check Credit Karma every once in a while and mint updates every few months. The honest truth is that they all say something different, which is why we check annualcreditreport.com once a year and kind of go off of that.

Once we got our 30 year mortgage (2.58%), our credit score became way less important to us. Thanks for the heads up on USAA, excellent article as usual.

Damn – your mortgage rate is HALF ours!

That’s so cool! I think when we talked to you last my score was in the 500s, and now it is slowly but surely CLIMBING. We’ll have to get with you again to explain all the fun that’s happened recently :D

Holler anytime, my friend :)

I probably should be embarrassed to say that the last time I checked it was when I purchased a house six years ago. It was 810 at the time. I should check it just to make sure there’s no fraud and such. Other than that, because I always pay off debt in full (except mortgage) I tend not to worry about it. Now that I’m married, though, I guess we should see how we’re impacting each other. Another thing to add to the list. :)

Would be interesting to see what it is now for sure :)

We’re in the upper 700s but nowhere near your score. That’s maybe the highest I’ve ever seen. Well done!

I tend to check my credit scores every few weeks because I get emails from Credit Karma, Credit Sesame and Quizzle that an “updated score” is available. I check that mainly to ensure that nothing weird is happening.

I also check my credit report ever 4 months or so, once for each credit agency every year spaced out.

Funny, in checking my credit scores this morning we’re just over 800. They reports tell me my scores aren’t better because I don’t have enough open credit accounts -only our mortgage and 1 credit card. Don’t think I’ll be opening more cards just to improve my already 800+ score though. :)

Agreed :)

Also – you’re hardcore w/ all that checking! Haha…

I only know my score from what mint.com tells me. 791 was the latest. I gotta crack the 800s!

My credit score wavered a bit last year. It started around 700, then dipped a little over the summer when we bought a used vehicle and got a loan, then went back up a little as we began paying on the loan, then dipped again as we bought a house (closed in December!! Woohoo!!). Anyway, now it is back up over 700, so we are happy about that. Hopefully continuing to make our normal payments will help it keep going up and up. It may dip again if we decide to get a credit card to use on vacation. We have money saved up for our trip, but don’t want to take that much cash or swip our debit cards all over the country, so we might get a credit card (we currently don’t use credit cards) to use for that. So, who knows, that might ding us and bring us back down a little, but I’m not super worried.

Also, my credit history isn’t very old, so that doesn’t help my score any :(

I’m impressed you’ve been tracking it over the past year though – such a great habit to get into!!

I didn’t know I could get my score from USAA. I get it monthly from another bank. So I signed in to USAA and got mine!

814

Not quite as good, but very happy with it.

Look at that! Nice little treat to look forward to logging on in the future, isn’t it?

I wish they offered it for free in Canada, we’re not so lucky. We have to pay. Mine has dropped to 657 but I suspect its because I changed my name and extra inquiries were made against my profile. It’s interesting to know that even at that score my credit ranks higher than 21% of the Canadian population. At least they’ve all fixed my home address now.

Interesting about the name change… I wonder how big of an effect that has?

My husband’s credit score is dropping like a rock since he has no open credit at all (he used to have a home depot card, but he cancelled it due to the data breach and hasn’t reopened anything). Mine is remarkably stable (and high) considering I have low limit card that only gets used for rental cars.

I’m not worried about our scores right now since my husband and I have taken on the zero debt stance, but if we ever need to rent a house or apartment in the future, we will pick up credit card churning as a hobby 6 months prior to trying to search. Even with our zero debt stance, we both check our credit scores twice per year because I would hate to be the schmuck who has a 300 credit score because of $.02 in outstanding medical bills or phone bills that go unpaid and somehow mar your credit.

Hah – yeah. Sometimes it’s little stupid things that can screw us in the end. Good for you guys for staying on top of it!

Are high credit scores the status symbol for finance bloggers? Last time I checked it was definitely over 800, but now I want to re-check and get that exact number!

Haha… it is now! :)

788 at credit.com . I can’t use Credit Sesame, because the site says I signed up and have to know the password or something. But I like credit.com and think it is Experian they use.

We found out our credit score when we refinanced last year. They were in the mid-700s, which I was happy with. My husband’s was a little higher because we put most stuff in my name, and I occasionally forget a bill.

That’s when we found out that our old apartment complex put us into collections (without notifying us) for repairs after we moved out. Yet another reason to check your score regularly.

Ouch!

We have to put stuff in my wife’s name all the time cuz she didn’t have much credit history when we first met. But then she likes to rub it in when her scores is better than mine :) Which is fair. I obviously do the same!

I personally use credit karma that gives you scores from two companies. It also gives you a summary of all your accounts and their standing. Anytime there is new activity you get an alert.

Just checked and my credit score is at 769 for both.

Cheers!

Woah buddy, that there score is rhiteous! LOL. My Experian score was 776 at the start of the year per my citi credit card. Experian’s usually my lowest score but I’ll check them all and reports some time this year.

I actually checked my credit score a month ago for the first time in years and was pleased when both scores I was given from Credit Karma were above 800. Getting a high credit score is not hard to do as long as you opened a card early (I think I got my first one when I was a freshman and college) and never miss a payment. I also used to have a car loan (shame on me) and I’m still paying some small student loans (on time of course!).

Yup! Just like with everything in finance, the earlier you start and let it ride the better it gets across the board :)

I believe my credit score is at 803 right now. Just checked it the other day. Barclay offers free credit scores to its credit card holders, which is great!

Here in Denmark there’s no such thing as credit scores. Your ability to repay a loan is evaluated by an actual human being based on you income, your debt and how trustworthy you seem.

If you stop paying on your debt, creditors will add you to a database of bad debtors and nobody (except for a few business who charge ridiculously high interests) will loan you anything. You can’t even get a phone subscription.

It works pretty well.

Woahhhh love that! Haha… what a novel idea ;)

(No way that would work here cuz all those financial companies WANT people to fail and owe them interest!! It’s all jacked up.)

“Which is were (free) credit reports come in…”

Change the “were” to “where” to make it Super SEXY

okay okay, pipe down – changed ;)

So happy to be a Discover card member! I get to see it every month! I’m in the mid 700’s which isn’t too bad, but hopefully with time and more history, it’ll keep on going up and up!

It’s great for credit card churners that the credit card companies are providing scores for free now. The ones I know of currently are Capital One, Discover, Barclaycard and recently Citi. That’s one thing to keep on top of when applying for new cards. Funny enough, I finally got my score above 800 after a few months of credit card churning.

You guys are better than me on that churning stuff – makes my stomach hurt!

Great score, I believe last time i checked I was in the low 800s, I can’t remember if it has been a year since I checked it for not. Will check again when i get back on the right side of the globe so i can actually print it off. If Canada brings this out i will be a happy guy.

On an unrelated note, I believe this site moved up on the Modest Money Top Financial blog page.

Ooh la la – will have to check, thx!

Got to 721 this month. Not exactly stellar, but much better than it’s been years after living in ignorance and likely the 600 or less range. Now it’s just time and good habits to get to 800.

Helluva jump!

Well I decided to pay the $22.95 or whatever it was to see mine. I am sitting at 820. Mine is an Equifax report, apparently they go to 900? I didn’t know that. Apparently my score is higher than 81% of Canadians. I don’t really know what to do to get it higher other than paying off more of my mortgages as my utilization % in those accounts is 76%. My revolving debt % is 8.

Looked at the whole report and everything looks good to me. I am surprised to see my street bike loan still on there as I paid it off years ago.

All in all, I’m pretty happy.

After I wrote that I wasted another $20 something dollars and printed my Transunion score. Again its out of 900 and it rates me at 812 which is higher than 75% of Canadians. Looks like i have some work to do!

Haha… so you just dropped $40 to get a cple scores? You’re hardcore – love it. Could be a lot worse ways to spend $40 :)

I still have two weeks overseas working and I wanted it NOW. Plus I dont think i get my score for free in the mail, just my report.

Just checked mine and I’m waaaaaaaaaaay above where I was last time I checked (When I brought my car) The military and just being a dumb kid with new MONEY THAT WASN’T ACTUALLY MINE was not kind to me. (All my own fault.. not monitoring my finances) .. since despite advice I refuse to have credit cards or take out loans or buy on credit for anything lower than 5K… I’ll be honest I’ve seen below 550… Now.. close to Mid 700’s But now after seeing Those J Money #’s and reading comments.. I’m thinking At Least High 790 – 805 in the next 3 -4 years

You’re not alone unfortunately – tons of military guys (esp the guys!) are bad with money. and love sports cars for some reason :)

Checked mine last month and it was 816/820, so I’m right behind you. It would be great if the trend to provide credit scores expanded to all the banks and credit cards.

I’ve been seeing the advertising for the credit score on a Discover card for months now and I’ve never bothered checking! Haha I checked right now and I have 800. Got dinged for keeping a balance on my cc’s (pay off in full every month but use for cashback and ease), and for the car loan (paying off slowly since it’s 0%). So oh well!

I used credit karma too which I love because of the way it breaks down your score and how to improve it.

Great reminder for me to check my credit report:P Thanks J Money!

Now you’ll pay attention to it every time you log onto Discover :)

I actually checked my credit score last month, have had an account with Credit Karma for a while now. I also did pull my free credit report at the beginning of the year and luckily I didn’t see anything strange on it. Credit Karma basically gives you the report now too in addition to the score, but it was nice to double check from the official source. I believe my Barclay card even offers a free credit score now too, they seem to be popping up everywhere. I think my score is finally approaching the high 700s though!

I could use some advice. My husband and I have gone the Dave Ramsey route over the years, which is great because we have no debt beyond our mortgage, have an emergency fund, ect., but we’d like to buy a new house soon and our credit scores are not where I’d like them to be (around 700, give or take 50 points) and I of course want to get the best rates on our next mortgage.

These less-than-stellar scores are because we have no accounts open except for our mortgage, which we refinanced 3 years ago (paying off half of our house debt in the process) and currently has a high balance that will take a long time to decrease because we refinanced into another 30 year in order to keep our payments low so that we can afford to only have one of us working and the other at home with the kids. However, we have the neighbors from hell (they possibly literally torture puppies, they are currently under police investigation for animal cruelty) and it seems no matter what they do they are going to be here forever, so we’d like to move in the next couple of years to a single family home so we have some space from neighbors.

I believe now is the time to build up our score and apply for credit so we can then not apply for anything else for a year or two and allow our credit to build. So far I applied for a Discover card a couple of months ago, which has already improved my FICO score to 750 according to Discover. I then added my husband to the account and increased the credit limit as much as they’ll let me. Is there anything else we can do? Get another credit card? Pay off a chunk of our mortgage? I would love to get us into the 800s by 2016, if possible. Thanks.

Love it! (not the nasty puppy haters, but the credit building ;))

I’m not a credit expert, but I think you’re on the right track. I’d even personally open up 2-3 more, some with stores directly (target card?) and then another main c/c and do the same thing (upping the credit limit) and just making sure to use it every few months and then pay it all off ASAP. That’s helped in my experience.

Maybe others have some ideas too?

I check mine and hubby’s every month…on Credit Sesame and our Capital One accounts.

Mine was up 9 pts and his was up 7pts this month…WOO HOO!

Keep in mind that there are a variety of companies out there producing credit scores. But over 90% of lenders use FICO. The only way to get your FICO score is to pay for it at their myfico website. So all those free credit scores will give you a great ideal of where you are at. Because good credit is good credit. But when you apply for something they won’t be looking at Credit Sesame, Credit Karma, etc.

Definitely good to consider!

I have also gotten mine for free through discover card. It is nice to see it and check it monthly.

Great score! I use the Discover feature. Mine has gone from 771 to 817 in a few months– there was a home purchase during that time. I’ll take it!

I would too!

Though it doesn’t surprise me with you – you’re pretty good with money :)

I am so excited that USAA is offering this. Some of our other products do, but I log on to USAA regularly so this will make it super-easy to keep an eye on things.

I only have an 802 right now, but given that we have purchased a house and refinanced two others in the last 15 months, I think that’s probably OK. We had quite a few inquiries, plus three new HUGE loans, so our loan balances are all near their max. That should improve all by itself, I hope.

I am so glad I saw this post!

And you STILL have an 802?? That’s bad ass! You are killing it :)

Mine was over 800 too! And then I took out a student loan and it literally dropped 20 points in a few weeks. WOW – who knew!? Luckily for me, my score is still good, but I can imagine it will go down over the next few years of school again. Returning to school as an adult is no fun!!! Also, Discover and AMEX both offer the free credit score – so I get to look at it every month. It was more fun when it was higher – ha! :)

Haha, I bet :) Good luck with the school stuff though! Good for you for going back and knocking that out. I know it can get expensive and what not, but I’m a firm believer that it’ll more than make up for it as time goes on. Hope you get through it all smoothly!

Can you update this post with a link to the follow up homework for us new readers?

Every new blog post of mine is pretty much a chance to get homework :) Just sign up to get my blog posts emailed to you and you’ll always be pinged! (And hopefully motivated!)

http://forms.aweber.com/form/24/1196048824.htm